From Business Spectator this morning:

Coking coal prices have slumped to six-year lows, many Australian mines are not making money and the industry is set to close more of the mines that produce the nation’s second most valuable export.

A dramatic fall in quarterly contract prices for the steelmaking raw ingredient has caught industry players by surprise and led coal giant Peabody Energy to declare it is considering the closure of Australian mines it recently indicated were safe.

As boom-time-approved expansions continue to increase supply, the June quarter coking coal contract price has fallen from $US143 a tonne to $US120 a tonne, which is close to typical cash costs for the east coast coking coal industry, according to Credit Suisse analysts.

This means when things such as corporate, financing and sustaining capital are added in, most producers would be losing money.

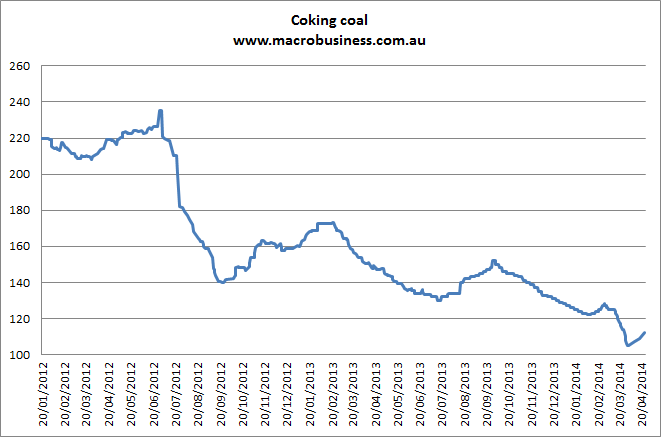

Nobody, least of all the industry, can be “surprised” by this. BREE is forecasting $127.50 average price this year. The spot price crash has been as impressive as it has long and telegraphed the contract crash:

Next quarter is going lower still!

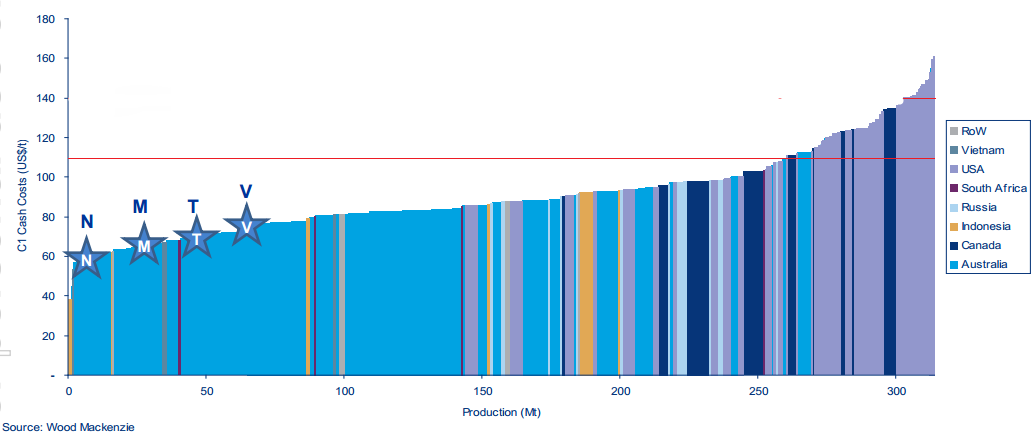

Cash costs are much lower than Credit Suisse reckons, according to Wood Mackenzie, though the point about break even costs is right:

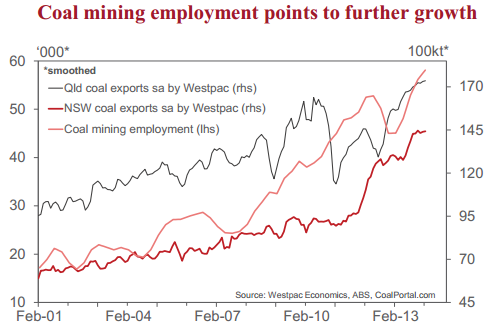

But remember, coal employment is booming on supply expansions. From Westpac:

Australian coking coal mines won’t close unless they’re globally inefficient and then they should shut anyway so what’s the big deal? Miners over-invested and now they must chew through it. Such is the commodity business.