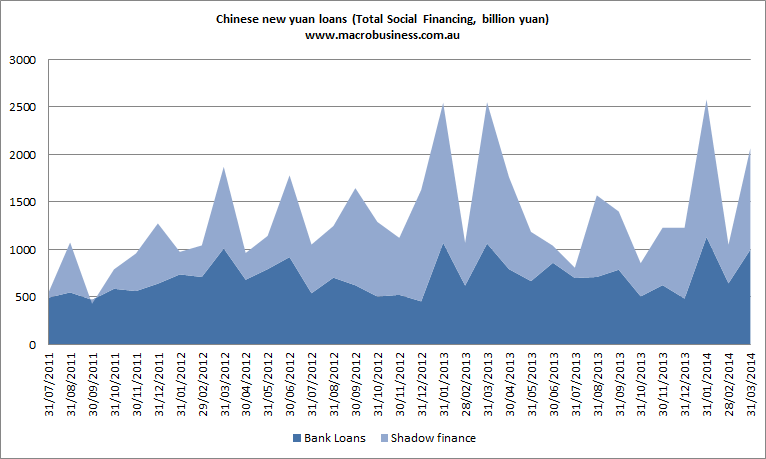

The world’s most important credit data for March is out in China and it is weak. Total social financing came in at 2.07 trillion yuan, well ahead of consensus at 1.85 trillion but still down 19% year on year. Bank loans were an even half at 1.05 trillion:

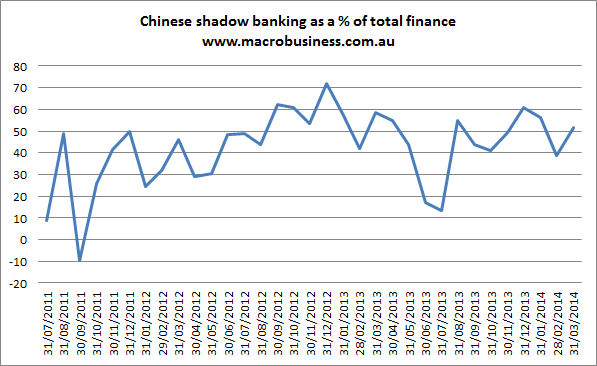

The shadow banking share isn’t shrinking:

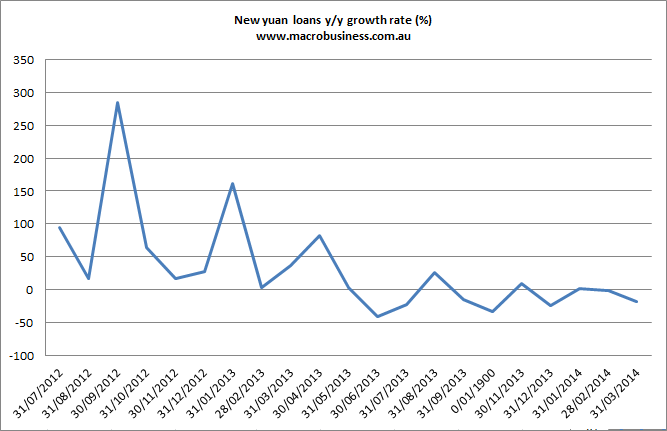

The growth rate for new finance remains deeply negative:

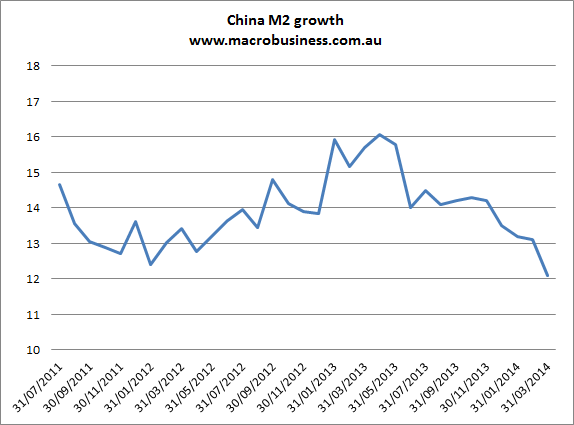

But M2 is now seriously undershooting the 13% target:

This is weak data and an uncomfortable mix to boot. For the first quarter the year over year shrinkage in new yuan loans is 7%. Moreover, the shadow bank component is holding up even as M2 undershoots, placing the PBOC in a quandary. It’s undershooting on money supply but isn’t reining in the relative contribution of shadow credit very fast, if at all.

That probably means steady as she goes with modestly tight policy. Indeed, today it resumed draining liquidity from interbank markets, 79 billion yuan from 14-day repo and 93 billion 28-day repo.

This weak credit and firm hand will weigh on Chinese growth for at least the next six months.