More excellent work from Westpac’s Elliott Clarke today:

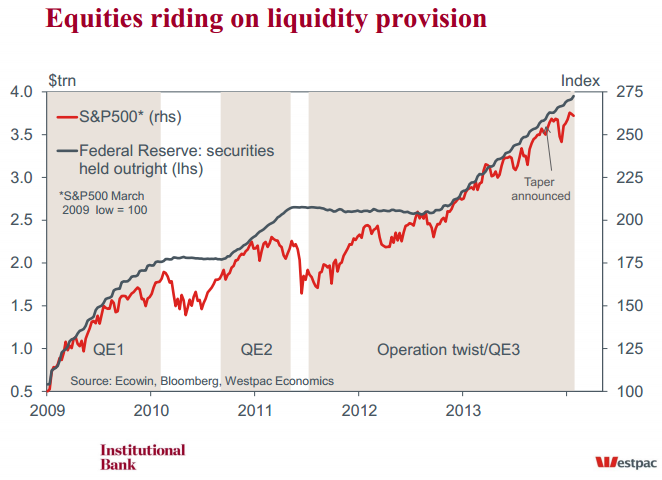

A cursory look at the performance of the US stock market would indicate that the Federal Reserve’s efforts to right the US economy have been a storming success. The rally in US equities through the Operation Twist and QE3 episodes has been dramatic, with the S&P500 gaining over 60% since October 2011 to reach new highs.

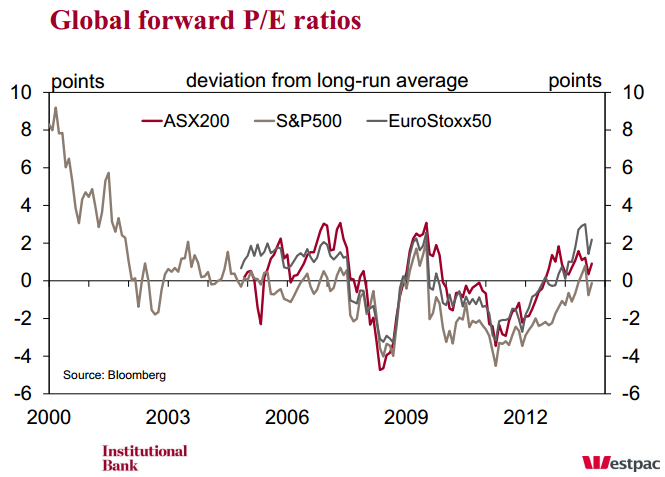

While is it certainly true that the FOMC’s actions over the past two and a bit years has facilitated this recovery by instilling confidence and providing liquidity, it is important to recognise that there has also been a clear ‘fundamentals’ narrative. Simply, equity investors have reacted to the improvement in profits (financials in particular) as well as belief in a new wave of technological progress, spread across established tech firms and new entrants to the sector. In aggregate, P/E ratios based on forward earnings hardly look stretched: the S&P500’s forward P/E is currently around its long-run average, well below the heights seen in 2000.

Still, against this fundamentals-based rally, the US economy has consistently struggled for momentum. As we have continued to highlight: employment growth has only marginally outpaced population growth and real wages growth remains meek, giving little support to household demand; further, demand from corporates and the public sector remains (at best) modest.

So how should we square away this obvious disconnect between financial markets and the real economy? In part it is because of the material external exposure of large US corporates: they may not be producing goods within the US’ borders, but (at least for their non-tax accounting statements) their global profits are repatriated. But, in this recovery there has been a further key influence.

Simply, instead of looking to maximise top-line growth, all eyes have been on the bottom line; and instead of being focused on their productive capacity, firms have remained most keenly interested in their financial structure.

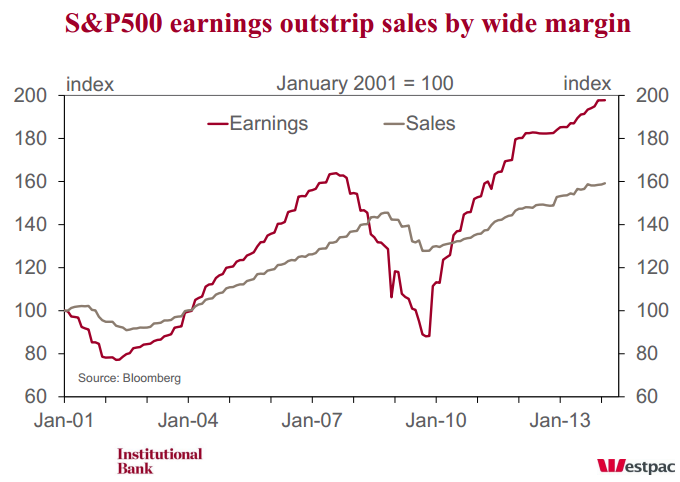

On the first point, comparing S&P500 sales to earnings clearly highlights that large corporates remain focused on the bottom line. Faced with weak domestic demand, large US corporates have actively sought to manage their expenses so as to meet and exceed the market’s expectations. Combined with the unwinding of provisions taken in the GFC, cost management has allowed US corporates to achieve a 124% increase in 12-month trailing earnings off the back of a 25% increase in 12-month trailing sales since October 2009. We note that available data points to this phenomenon being concentrated in the financial sector: since August 2011, earnings and sales have risen by 20% and 12% respectively for the S&P500; sans financials, earnings and sales have both risen by 15%. Arguably, the initial improvement in profits post GFC provided the narrative for the market, while the subsequent liquidity associated with the QE initiatives fostered the confidence.

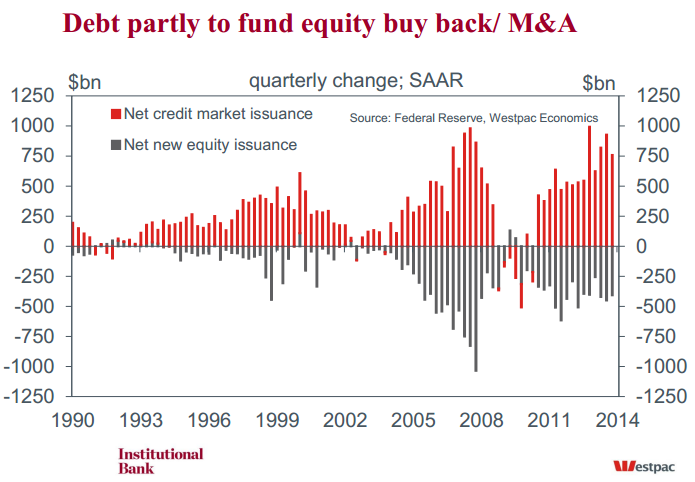

Capital structure management has also provided significant benefits for US corporates over this period. Specifically, the free availability of debt capital to well-rated corporates has allowed for persistent, cost-effective share buyback and dividend programs. This has had a two-fold effect: reducing the number of shares available, all else equal; and also incrementally increasing the total return available to the remaining shareholders. Together with the tight cost management noted above and expectations of a new technological age, capital structure management has then provided the substance for the strong, broad-based US equity market rally.

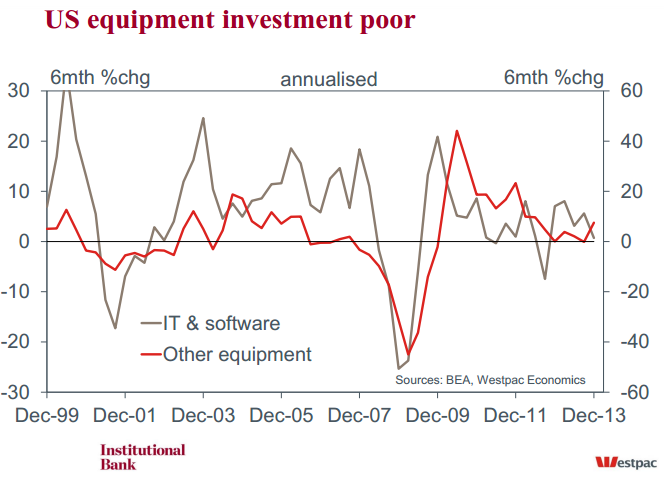

We will leave the obvious benefits for households’ wealth for a subsequent discussion. What we instead focus on for the remainder of this article is the consequence for business investment. Being able to meet, and indeed exceed, investor expectations through management of the bottom line has negated the need to invest in their own productive capacity. This has resulted in a deteriorating underlying trend for business investment, further impacted by the various bouts of fiscal uncertainty.

Needless to say, this is not a viable long-term strategy. One has to argue that there is an inevitable limit to the earnings benefits achieved through cost and capital management, with top-line trends the inevitable determinant of long-term success and stock performance.

All else equal, the absence of persistent investment in productive capacity and efficiency creates a tension between the market’s expectations and firms’ ability to perform. This tension has been magnified by the degree of liquidity provision offered by the Federal Reserve.

The apparent disconnect between financial market performance and real economic activity should concern investors. If the FOMC’s economic forecasts fail to be achieved again in 2014 and, at the same time, liquidity continues to be removed, the sharp improvement seen in household financial wealth may be jeopardised. Stay tuned for more on this topic in coming weeks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.