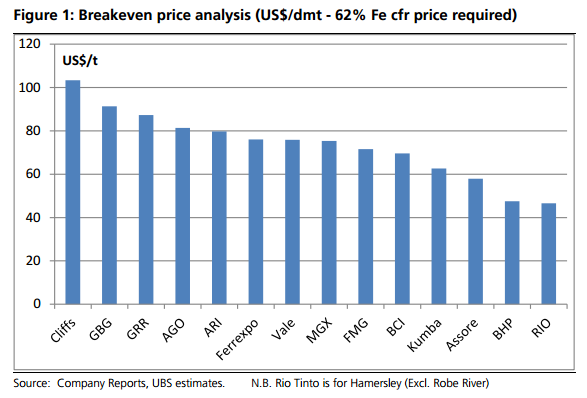

Here’s a chart from UBS to raise a few eyebrows:

Any comments on the notion that FMG is cheaper than Vale are welcome! UBS argues it’s because of the higher shipping costs despite Vale’s C1 costs of $23wmt.

Here’s a chart from UBS to raise a few eyebrows:

Any comments on the notion that FMG is cheaper than Vale are welcome! UBS argues it’s because of the higher shipping costs despite Vale’s C1 costs of $23wmt.