The bullhawks are back. A new flerd but no less ear-piercing. For those that don’t recall or are new. The bullhawk is a creature that believes in the new normal interest rates and property prices can rise together.

According the Paul Bloxham and Stephen Koukoulas the Australian economy is rebalancing, momentum is building in the services economy, net exports will support growth, the capex cliff (when it gets a mention) will be be leaped clean over and interest rate hikes loom large. The Kouk is a new devotee of the bullhawkish school but has quickly assumed its leadership with the most aggressive rate hike forecasts in the market.

To be clear, I have absolutely no issue with the argument that we’ve got a cyclical bounce underway. I’ve been on board with that since the post-election snap-back. Indeed, in any other cycle I’d would have been screaming “go long Australia” a year ago.

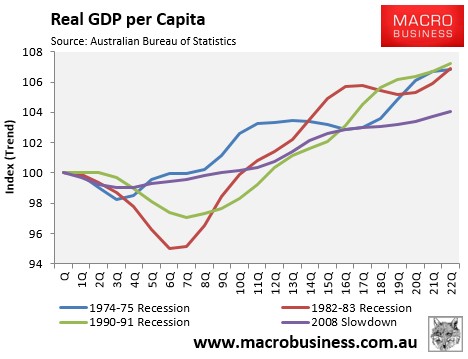

But I remain firmly of the view that this is not a normal cycle. It’s the end of a super-cycle in mining and a structural denouement for Australia. China made that abundantly clear this week with its extraordinarily ambitious reform agenda. And that presents headwinds to our current cyclical upswing that will make momentum difficult to sustain, just as it has for years already, let alone boom. Here is the the per capita growth comparison of this cycle with the last few recoveries:

This cycle is well behind and slipping further. That’s not say that it won’t continue on its trend. Both Leith and I have argued that is the most likely outcome, but it will feel like a recession nonetheless and is high risk.

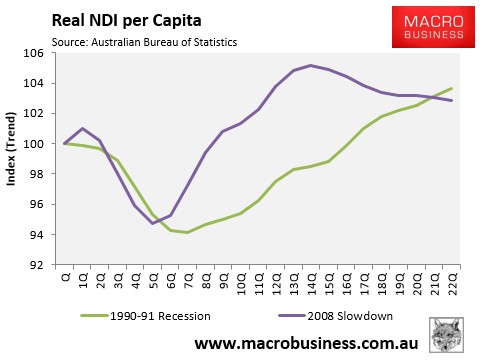

Why? What are these head winds holding us back? They are three and all are structural. The first is the terms of trade are going to keep falling further than officials are forecasting as China faces up to its own rebalancing. That will mean, by definition, falling incomes. Here is the chart from the national accounts that shows very clearly where this is heading:

There will be no new income growth to fund a services sector expansion. Yes, there is an alternative, consumers could run down savings and/or leverage up, but how sustainable is that? A point I will return to.

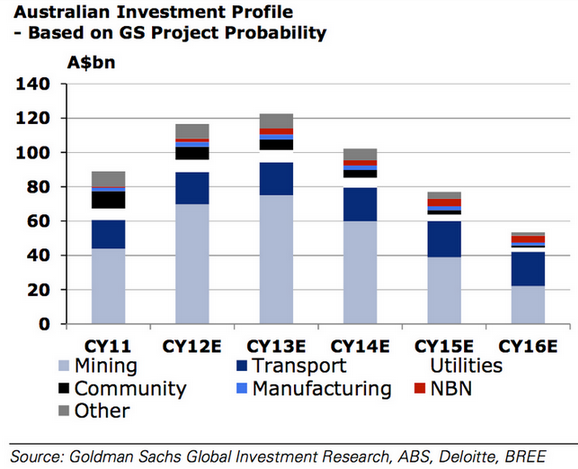

The second headwind is the capex cliff which will keep pressure on the jobs market. Here it is again in all of its hideous glory. from Goldman Sachs:

I have acknowledged for several months that we’ll see some loosening in the labour market in the first of half of this year, which is great. But as the capex cliff gets steeper, job losses will accelerate. NAB estimates 100k jobs will go in the next 12-18 months. Nobody knows exactly how many and there will be offsets in 457 visas and in falling imports but the multipliers will be very significant anyway. Of course net exports will rise and support headline GDP but that will do nothing for real activity or jobs. In effect we’re swapping the component of our growth that’s created all of our post-GFC jobs for a new one that contributes the same amount of growth in the accounts but eliminates all of the jobs it previously created.

That brings me to our third headwind, which is that after 23 years without a recession, the economy is incredibly inflated in reference to other countries and can’t compete in anything. Hence we are seeing many of our iconic businesses collapse. This is another drag on employment.

So, the upshot of all of this is that for the economy to keep growing, consumers are going to have to carry a lot of the growth load simply by spending and they’ll have to do it into the teeth of these three headwinds.

Their one great support, the house price boom in Melbourne and Sydney, is obviously behind the new momentum in the services economy. The construction boomlet is also useful. These are creating new jobs in the old housing and consumption economy and will offset, in some measure, the pressure in domestic demand driven by mining. Government will probably not detract from growth and will add too it from 2016 as its roads agenda gets moving. I happily acknowledge that it’s possible that the Australian economy could triumph over the odds if we consume our way over the capex cliff. It’s not very good for our structural issues longer term but leaving that aside we could pull off a tremendous can-kick.

That is not the issue I have with the bullhawks nor do I wish to address these today. My issue is that in these settings, Bloxo sees rates rising in Q3 and Q4. In December, Kouk saw rate hikes in Q1, Q2, Q3 and Q4.

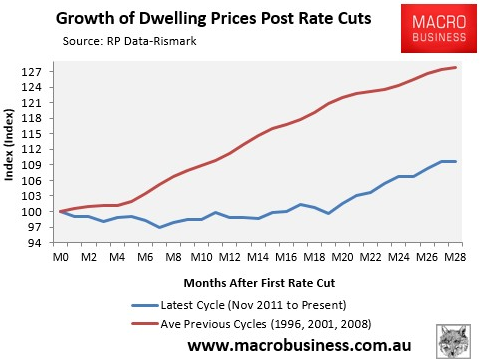

This is where the bullhawkian delusion presents itself. This rate cutting cycle has witnessed the slowest response in housing markets of any in the past twenty years:

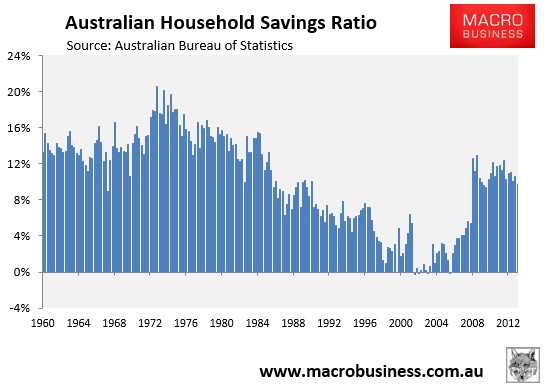

Consumers remain more conservative than during the pre-GFC period. It’s a structural shift. The national savings rate has eased but remains high:

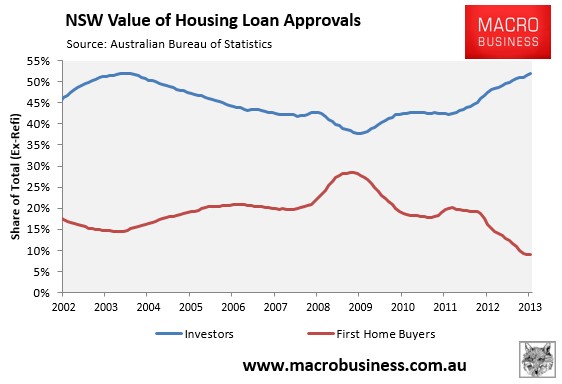

Truth be told, it wasn’t until the RBA’s last cut in August 2013 that the south eastern housing market really took off. The structure of the response is very odd as well, completely dominated by investors, with new households absent:

Both of these facts lead me to conclude that the neutral cash rate is actually not very far above where it is today and that the momentum in the housing market will very quickly reverse in the event of a rate hike or two (let alone a ludicrous four in quick succession). The negative flow onto consumption would also be very rapid and shift demand from reasonable to stall. If it happened before the Fed moved in mid 2015 then the dollar would soar as well. Underneath the consumption activity we’d find…well…nothing, except a deepening capex void which we would then tumble into.

This business cycle is not a healthy rinse and repeat of the Great Moderation as these chaps imply. Our situation is much more akin to that of the US today, replete with it’s financial repression that forces investors to chase yield. Give them a safer option and they’ll take it. In the mean time, they’ll blow bubbles wherever yield can be located.

As such, the RBA will not have the option to slowly ease off the credit spigot. Just as in the case of the US “tapering”, the removal of stimulus will threaten a flight to safety. So long as the capex cliff lasts, the RBA has an on and off switch not a lever. This is why we needed, and still need, macroprudential policy; to prevent this very conundrum from coming to pass. To his credit, the Kouk has acknowledged this, Bloxo has argued against it.

To finish, I can only observe with a wry smile that it appears to be my curse to have to repeatedly defend a housing bubble that I have argued so long against.