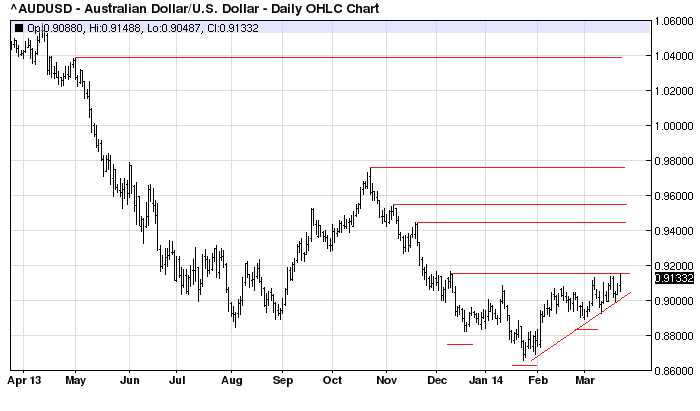

The Australian dollar wrecking ball is swinging. The technicals are screaming a looming breakout. We’ve got a head and shoulders bottom in place and an ascending triangle. Last night it spiked again, butting up against the 91.49 resistance level and it’s next step will the December high of 92. After that, technically at least, it’s a clear run to 94.5, then 97.6, and then clear air past parity:

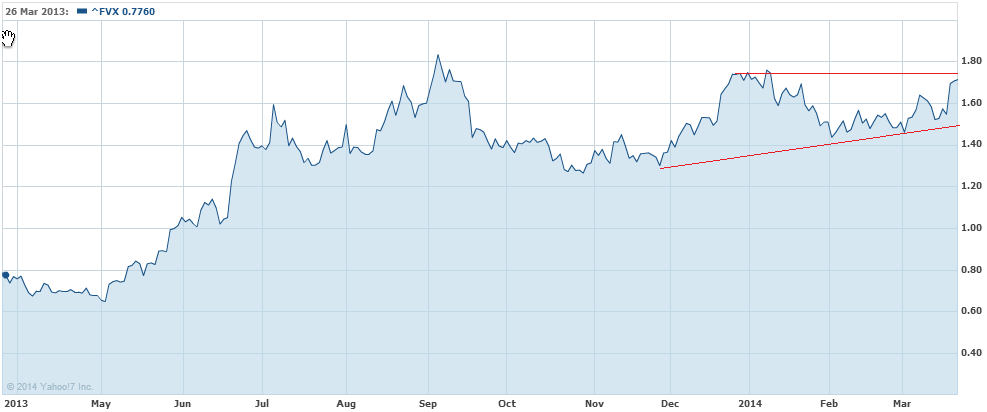

That this is happening while iron ore collapses and Chinese growth stagnates tells you all you need to know. The dollar wants to go higher on the RBA’s revitalised housing bubble, the specter of Chinese stimulus and, more importantly for now, movements in US bond markets, where the curve flattening is getting more aggressive. 5 year yields jumped 1% to 1.74% last night and also have a bullish ascending triangle chart:

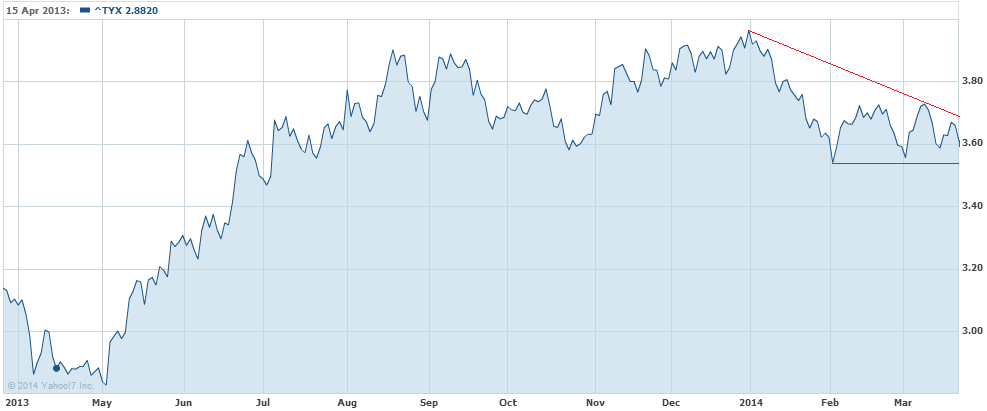

But 30 year yields fell the same and illustrate precisely the reverse:

This is a terrific combination for the Fed and the US recovery. Movement at the short end enables perceptions of interest rate normalisation but the long end – which determines mortgage rates – is actually getting more stimulatory.

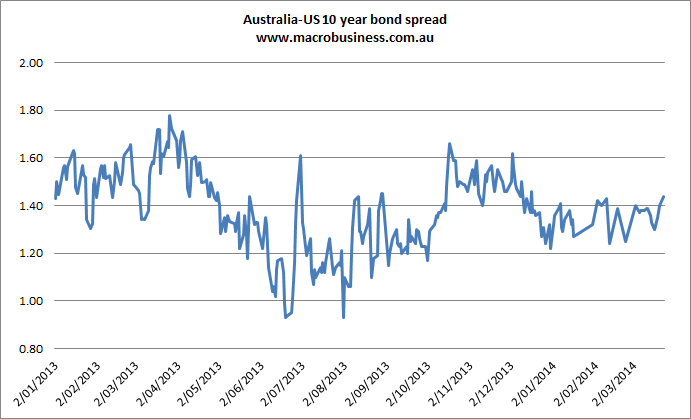

Yields on the US 10 year also fell 3 points to 2.72% and the spread to the Australian 10 year also reached its highest this year:

Let’s game this out for Australia. I see three possible scenarios if the dollar rises to 95 cents or beyond and stays there.

Scenario one: Zombificaction

The nascent recovery in tradables is squashed and hits the stock market hard as corporate profits tumble on weak realised iron ore prices. The Budget recovery is snuffed out on both iron ore and weak nominal growth. House prices keep rising as everything else falls away and that prevents the RBA from cutting rates. Even so, consumer confidence remains subdued and spending weak, exposing us to the capex cliff. A negative feedback loop forms steadily between the dollar, the Budget, the consumer and the capex cliff and eventually stalls house prices as well. More rate cuts flow as inflation weakens on rising unemployment. The dollar tumbles around a weakening economy in 2015 and the post-mining boom adjustment moves into a long phase of grinding real incomes lower.

Scenario two: Boom and bust

It’s the same as above except house prices keep running at their current pace. By year end the RBA is forced to raise interest rates. The dollar goes to parity. Housing and tradables bust together. The post-mining boom adjustment happens via a quick and very difficult step down in national income.

Scenario three: Managed adjustment

The alternative is to act on macroprudential tools now. Whichever mix of tools is chosen the effect will be to slow and even stall the housing market. It will take six months to see the effects but the dollar will, relatively quickly, begin to follow the plateau in house prices as more rate cuts are priced. The dollar will tumble to 80 cents by year end as rates fall to 2%, largely offsetting the drop in the iron ore price, hugely boosting corporate profits and the Budget. The ASX will rise to 6000 points, helping offset the impact of the housing slowdown on consumer spending, which will also be supported by cheaper mortgage repayments. Inflation rises but is addressed as temporary by the bank and part of the post-mining boom adjustment to lower real incomes.

The capex cliff will remain a large risk and because the RBA has already allowed house prices to determine the course of recovery, it’s possible that macroprudential tightening could tip us into the same negative feedback loop described above.

I’d still take the latter course but the longer it’s left undone the higher the risks there are in doing it. Higher house prices and dollar raises the stakes on all pulls of the macroeconomic levers. The time for macroprudential tools was two years ago and we’d now have somewhat deleveraged households, recovering competitiveness, a much lower dollar, some inflation and a real chance of getting through the capex cliff without a recession.

No longer.