The Australia Institute’s (TAI) Richard Denniss has written a spirited article in The AFR today arguing that the Budget could easily be restored back to surplus if the 3% of GDP decline in revenues experienced over the past decade were restored via undoing tax cuts and concession implemented during the Howard and Rudd eras:

The Commonwealth budget is bleeding cash. The problem has virtually… everything to do with the decisions of the Howard and Rudd governments to introduce permanent, and massive, cuts to the revenue base when the economy was booming along nicely. Nearly a decade on, the price we are paying for their generosity continues to grow…

[Meanwhile]…the cost of tax concessions for superannuation continues to grow by about $5 billion per year and will soon top $50 billion…

Similarly, the cost of the 50 per cent discount on tax payable on capital gains costs the budget about $4.3 billion a year and, in so doing, creates enormous incentives for firms and individuals to engage in financially lucrative, yet economically wasteful, financial engineering…

Denniss also goes on to explain how the Abbott Government’s commitment to spend tens of billions of dollars on new joint strike fighters and submarines, along with $5 billion per year on the Paid Parental Leave (PPL) scheme, are at odds with the Government’s cost cutting program.

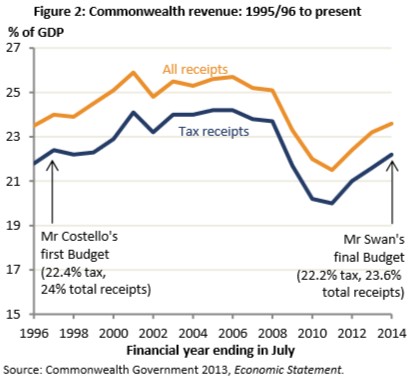

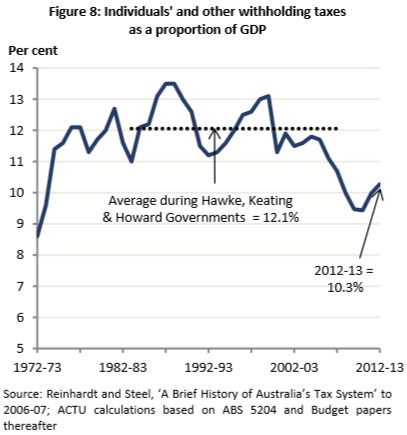

Denniss makes some valid points. To a large extent, the Budget is suffering from a revenue problem, brought about by tax cuts introduced as coffers were flowing from the once-in-a-century commodity boom. And now the boom is over, tax receipts have plummeted (see below charts).

Certainly, a good place to start to restore the revenue side of the Budget are cutting back egregious tax concessions like superannuation and negative gearing, which overwhelming flow to higher income earners and/or serve no social purpose.

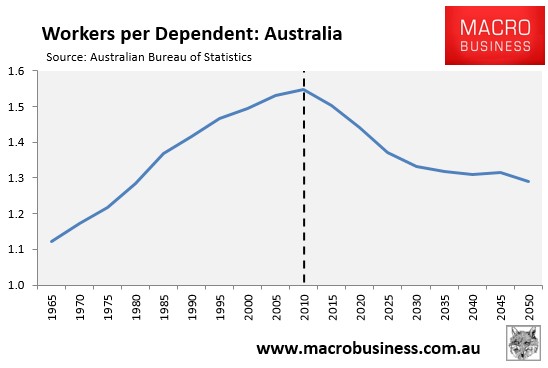

That said, it is an inescapable fact that the Budget is facing a demographic time bomb as the baby boomer generation retires and the ratio of workers supporting non-workers declines (see next chart).