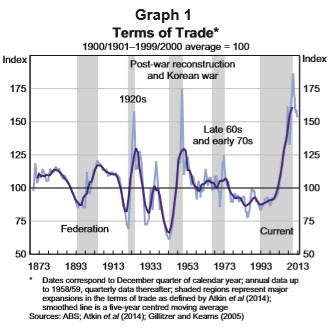

Australia’s terms of trade – the ratio of export prices to import prices – have increased significantly over the past two decades, with particularly large increases in export prices occurring from 2004 onwards (Graph 1). The terms of trade reached their highest level in history at their most recent peak – nearly 85 per cent above the average of the preceding century. This was also the longest terms of trade boom in Australia’s history and the terms of trade today remain at a very high level by historical standards…

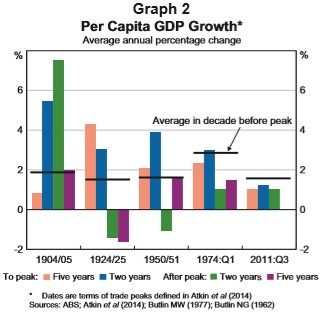

Movements in the terms of trade can have a significant impact on the Australian economy. Upswings in the terms of trade increase the real purchasing power of domestic output. Historically, upswings have tended to coincide with above-average growth rates of GDP per capita and have boosted national income considerably (Graph 2). In addition, falls in the terms of trade generally have coincided with a two-year period of below-average growth in GDP per capita and lower national income…

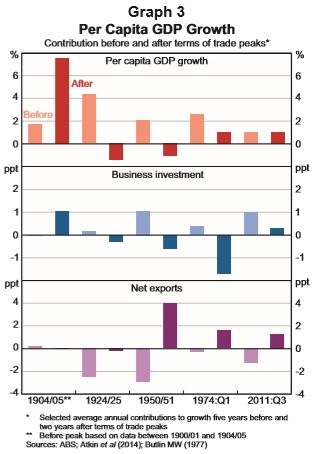

Cycles in the terms of trade affect all of the major expenditure components of GDP. However, in the current episode, business investment and trade have been of particular importance (Graph 3)…

Resource investment is expected to continue to decline over coming years, with the current level of iron ore and coal prices less conducive to investment in new projects. Investment in LNG projects has continued to be high in the two years following the peak in the terms of trade, with investment generally supported by long-term supply contracts. However, resource investment is expected to decline significantly in the next few years as current projects are completed. Meanwhile, non-resource business investment has been subdued following the peak, with domestic demand growing at a below-average rate…

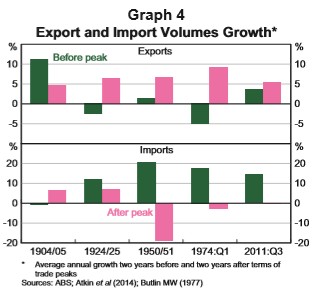

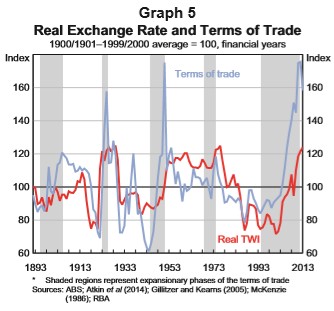

As the terms of trade decline, the external sector typically contributes sizeably to output growth (Graph 3). This is, in many ways, the flipside to developments during the boom. Export volumes grow as previous investment becomes productive (Graph 4). The fall in the terms of trade is typically accompanied by a depreciation in the real exchange rate, making exports from outside the booming sector more competitive (Graph 5). Historically, imports have grown more slowly, or even declined, following peaks in the terms of trade.

History suggests that growth of output per capita is typically slower for several years following a terms of trade boom compared with the period before, and that the weakness in national income is even more protracted. Past episodes suggest that per capita growth tends to return to an around-average rate within five years. While the current episode has parallels with those in the past – for example, being largely driven by a narrow range of commodities – the most recent terms of trade boom has lasted much longer than those in the past and the lag from investment to production in the resources sector has been considerable, particularly for LNG investment.

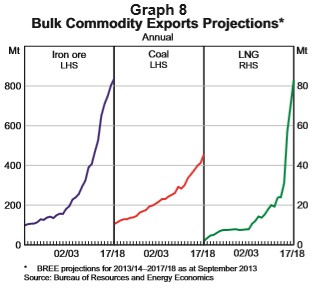

The transition from the investment to production phase of the resources boom has been underway for some time in the iron ore and coal sectors (Graph 8); coupled with increased supply from elsewhere in the world, it is likely to weigh on global prices…

A large part of the run-up in investment in the current episode was in the LNG sector. The delays between investment and production for LNG are long, and consequently strong growth in production is only expected from 2015/16 onwards (Graph 8). This is likely to contribute sizeably to GDP per capita growth. The high degree of foreign ownership in the resources sector, however, will mute the income gains retained domestically as production increases. It also means that foreigners are sharing the risks associated with any downswing in commodity prices.

As the real exchange rate and the terms of trade tend to move closely together, further declines in the terms of trade could also be accompanied by a further real depreciation. This increase in competitiveness is important in facilitating the transition in the sectors that contribute to output growth, as it promotes growth in the tradable sector outside of resources. A nominal depreciation is one way such an increase in competitiveness may occur; higher productivity growth and real wage restraint would also support Australia’s competitiveness. In coming years, measured national productivity will be boosted by the growth of production in the resources sector; however, productivity growth in the rest of the tradable sector will also be of importance in increasing Australia’s competitiveness.

In addition, there is likely to be a considerable reduction in demand for labour from the resources sector as the shift to the production phase continues. Wages in the resources sector, relative to those elsewhere in the economy, may decline (Plumb et al 2013). Such a change in relative wages would be a signal to assist the reallocation of labour and would have been less likely to occur under the more centralised wage-setting systems of the past. Overall, the expected decline in the terms of trade over coming years will pose challenges for both firms and policymakers. Nevertheless, the greater flexibility present in the economy today – such as the wages system and the floating exchange rate – should help to facilitate the necessary adjustments.

In my opinion, the RBA has under-played the risks to the Australian economy as the once-in-a-century terms-of-trade boom unwinds. By focusing on growth in GDP per capita, the RBA misses the far more important impacts on incomes and jobs.

Advertisement

As the mining boom shifts from the investment phase to the production phase, the reduction in real GDP will be offset, at least in part, by the expansion of mineral exports. However, as supply rises, export prices are likely to fall, resulting in a reduction in overall national income.

The below stylised example highlights these dynamics:

assumed an average cost of production of $60 per tonne

2013 average iron ore price price: $130 per tonne

2013 volume (example only) 500 million tonnes

Total profits: $35 billion

Assume in 2014:

Advertisement

export volumes grow 20% to 600 million tonnes

average iron ore price falls 20% to $104 per tonne

Average cost of production still $60 per tonne

Total profits = $26.4 billion

So despite volume growth fully offsetting price falls, profits from iron ore exports actually fall by $8.6 billion (24.5%).

Under this example, real GDP, which only measures volumes, would record big gains but national disposable income – the more important metric – would record a fall.

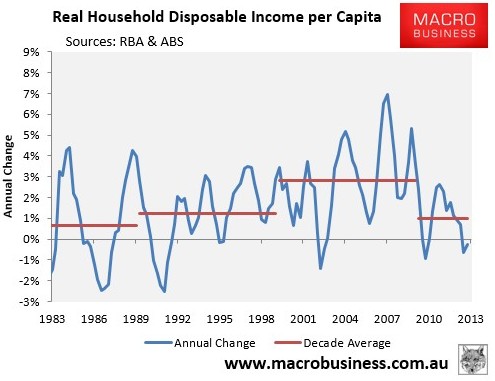

Indeed, this is exactly what has been occurring in the Australian economy. The next chart plots the annual growth rates in per capita household incomes and the average growth rates for each decade:

Advertisement

As you can see, the terms-of-trade induced surge in household incomes over the 2000s was remarkable, with real per capita income growth averaging an extraordinary 2.8% over the decade, well above the 0.7% average growth rate experienced over the 1980s or the 1.2% average growth rate experienced over the 1990s. By contrast, between 2010 and 2013, real per capita household income growth has averaged just 1.0%, despite the terms-of-trade index still sitting above where it was at the beginning of this decade.

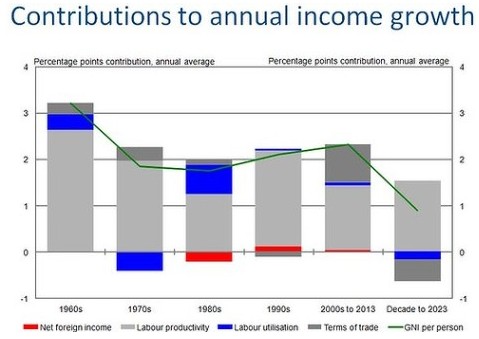

And late last year, the Australian Treasury forecast that average per capita income growth would halve over the next decade to the lowest rate of growth experienced in 50 years, weighed down by the falling terms-of-trade (see next chart).

Advertisement

To the extent that commodity prices and the terms-of-trade continue to retrace back towards their longer-term average levels, it will detract from household income growth. And with it, much of the income gains enjoyed over the 2000s will be unwound.

Then there is the deleterious impact on employment as the terms-of-trade falls, which the RBA has failed to adequately acknowledge. According to its own estimates, the mining sector accounts for nearly 10% of Australian employment, with most of these jobs in areas directly related to mining capital investment, such as construction workers, engineers, and other mining services. As mining projects are completed, much of the labour utilised during the construction phase will no longer be required, leading to a material increase in unemployment unless other areas of the economy can expand sufficiently to fill the void.

Advertisement

Rising unemployment and falling income growth are the key risks to the Australian economy as the mining boom unwinds, not changes in GDP, which are largely irrelevant.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.