From Business Spectator:

Gina Rinehart has secured backing from a group of global banks and export credit agencies for a new $US10 billion ($A11.0bn) iron-ore mine that can feed Asian steel demand, just as miners like BHP Billiton scale back investments amid a broad decline in commodity prices.

Australia’s richest person said lenders, including US, Japanese and Australian banks, had agreed to put up $US7.2bn in debt to build the Roy Hill mine deep in the Australian outback. The deal was signed in Singapore on Thursday.

…Ms Rinehart has already sold 30 per cent of the unit developing the Roy Hill mine to Asian steelmakers and trading houses, including Japan’s Marubeni Corporation and South Korea’s Posco, in separate deals agreed in 2012, not long after iron-ore prices peaked near $US200 a tonne. That has eased concerns that there wouldn’t be a market for the 55 million tonnes of iron ore that Roy Hill will produce annually.

…Some analysts question whether the world needs more iron ore when new mines are starting up in countries from Brazil to the Republic of Congo. BHP Billiton, the world’s biggest mining company by revenue, predicts global iron-ore demand won’t keep up with additional production for the next five years. Also, China’s push to tighten credit and rein in pollution could put a squeeze on steelmaking.

There will always be a market for Miss Rinehart’s ore. The question is at what price? My view is that China is embarked on a reform process that will see its steel production effectively peak in the next year or more so Roy Hill will enter a market under intense strain. This includes the argument that it can displace Chinese iron ore. Sure it can but if demand growth is weak the price is going to be much lower than anyone currently expects.

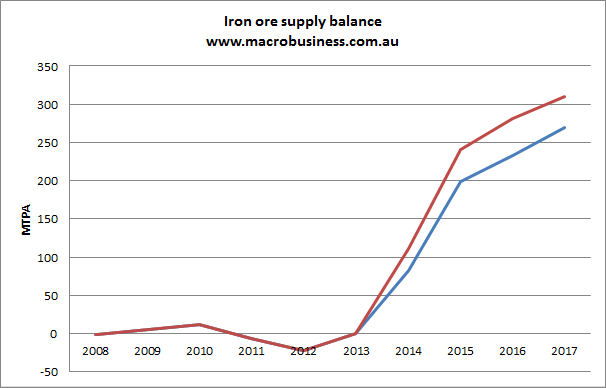

Most analysts see the seaborne market growing by about 20% to 2017 but what if it’s half that as China goes ex-growth? Here’s the supply curve based upon the two scenarios using Goldman Sachs data:

Blue is the scenario of 20% seaborne demand growth. Red is the scenario of 10% seaborne demand growth. You might think that in such a situation of gross oversupply it doesn’t matter anyway. Perhaps. But Mac Bank once estimated that knocking India’s 50 MTPA raised prices by $20 per tonne. Do the math.

That’s not to say the banks have erred. If they got guarantees from Ms Rinehart then that’s a no loss deal. Moreover, Miss Rinehart’s deep pockets mean the mine can behave irrationally for a long time during any shakeout, if it comes to that.

For anyone at the wrong end of the cost curve, and by that I mean producing above $80 per tonne (and probably $10 lower than that), Miss Rinehart just tolled your bell.