From Morgan Stanley comes the latest must read bearish China report. The outlines here are right but MS underestimates the impact of a Chinese hard landing upon the world. I’m currently working on a members’ special report about how and when this business cycle ends but MS nicely describes how that ending begins.

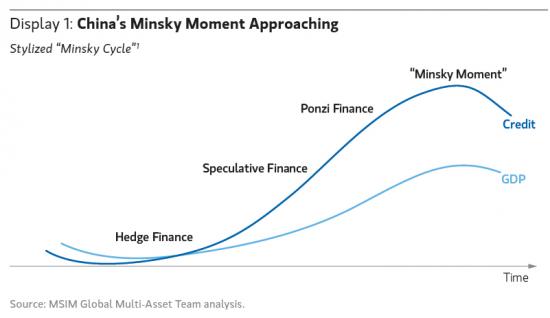

We have described in detail over the past two years how we believe China’s twin excesses (excessive investment funded by excessive debt) will inevitably unwind, causing a substantial slowdown in China’s economy, significantly below market expectations. In recent weeks, a trip to the region and further research into China’s shadow banking system have convinced us that China is approaching its “Minsky Moment,” (Display 1) which increases the chances of a disorderly unwind of China’s excesses. The efficiency with which credit generates economic activity is already deteriorating, as more investments are made in non-productive projects and more debt is being used to repay old debts.

Based on our analysis, our baseline case is that China may slow from the current level of 7.7% Gross Domestic Product (GDP) growth to 5.0% over the next two years. A disorderly unwind could take Chinese growth down to 4% in a shorter time frame with potentially disastrous consequences for levered Chinese assets (banks, property) and the entire commodity supply chain (commodity stocks, equipment stocks, commodity-sensitive countries and their currencies).

The consensus is more optimistic and expects China’s economy to grow by 7.4% in 2014 and 7.2% in 2015. Most market participants have concluded that the Chinese economy, despite its excesses, will slow only moderately as the government successfully manages to “soft-land” the credit and investment boom and that, as a result, the impact on global GDP growth could be moderate and is not likely to derail the global developed-market-led expansion. However, one of the more controversial conclusions of our analysis is that global economic growth could be impacted severely enough to cause a global earnings recession.

Hyman Minsky was a neo-Keynesian economist who developed a theory called the Financial Instability Hypothesis, similar to the Austrian school of thought, about the impact of credit cycles on the economy. In his 1993 paper entitled “The Financial Instability Hypothesis,” Minsky identified three financing regimes that economies can operate under: the first, which he called hedge finance, is a regime in which borrowers have sufficient cash flows to meet “their contractual obligations,” i.e. interest payments and principal repayment, usually by having a large equity component in their capital structure; the second, speculative finance, is a regime under which borrowers have cash flows that are sufficient to pay interest but not to repay principal, i.e. they must roll over their debts; the third, Ponzi finance, is a regime in which borrowers have insufficient cash flows to pay either principal or interest and therefore must either borrow or sell assets to make interest payments.

Minsky stated that “it can be shown that if hedge financing dominates, then the economy may well be an equilibrium-seeking and containing system. In contrast, the greater the weight of speculative and Ponzi finance, the greater the likelihood that the economy is a deviation amplifying system.” His paper draws the following two conclusions: 1) that “the economy has financing regimes under which it is stable, and financing regimes in which it is unstable” and 2) “that over periods of prolonged prosperity, the economy transits from financial relations that make for a stable system to financial relations that make for an unstable system.” In essence, the longer an economic expansion goes on, the greater the share of speculative and Ponzi finance, and the more unstable the economy becomes.

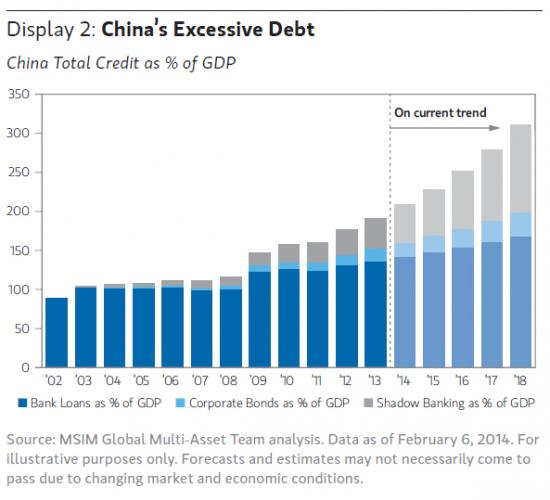

Our analysis indicates that China’s economy has arrived at that unstable state where speculative and Ponzi finance appear to dominate. From a macroeconomic perspective, very few economies have ever created as much debt as China has in the past five years. China’s private sector debt has increased from 115% of GDP in 2007 to 193% at the end of 2013.3 (Display 2) That 80% increase over five years compares to the U.S.’s 26% in 2000-2005. In recent years, only Spain and Ireland have achieved debt growth greater than China’s.Every year, China is now adding $2.5 trillion of private sector debt to a $9.7 trillion GDP.

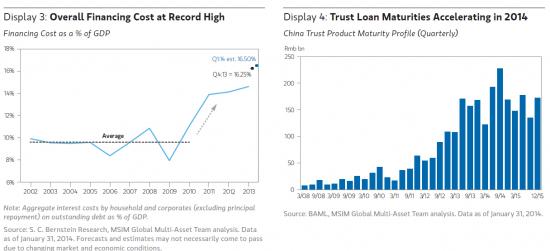

There is evidence that this debt growth has become excessive and non-productive. It now takes 4 renminbi (RMB) of debt to create 1 renminbi of GDP growth from a nearly 1:1 ratio in the early and mid-2000s. After the massive stimulus and more than doubling of new bank loans in 2009, the government attempted to stabilize credit growth, but the growth of the shadow banking system exploded instead. Shadow banking now accounts for more than a fifth of total credit in China—or about 40% of GDP from a base of 12% just five years ago. The shadow banking system funnels credit to borrowers who can no longer get loans from the formal banking sector, such as Local Government Funding Vehicles, the property sector, and companies in sectors with massive overcapacity and low or negative profitability such as coal mining, steel, cement, shipbuilding, and solar. Work by Nomura’s Chief China Economist indicates that more than half of Local Government Funding Vehicles, which borrow money on behalf of local governments to invest in infrastructure, have insufficient cash flows to pay interest or principal; the exact manifestation of Minsky’s Ponzi finance regime. Total local government debt adds up to RMB17.9 trillion (nearly $3 trillion) according to the latest, likely understated, national audit. In addition, estimates show that up to one third of all new borrowings are currently being used to roll over existing debt, and that interest payments on debt represent nearly 17% of Chinese GDP—a staggeringly large number (which excludes principal repayments) and which is nearly double the level that the U.S. reached in 2007. (Display 3)

It is clear to us that speculative and Ponzi finance dominate China’s economy at this stage. The question is when and how the system’s current instability resolves itself. The Minsky Moment refers to the moment at which a credit boom driven by speculative and Ponzi borrowers begins to unwind. It is the point at which Ponzi and speculative borrowers are no longer able to roll over their debts or borrow additional capital to make interest payments. Minsky states this usually occurs when monetary authorities, in order to control inflationary impulses in the economy, begin to tighten monetary policy. We would add that this monetary tightening often begins to occur at the time when the size of speculative and Ponzi borrowings have become so large that the demand for additional capital to keep these borrowers afloat becomes greater than the supply of such capital. We believe that China finds itself today at exactly this juncture.

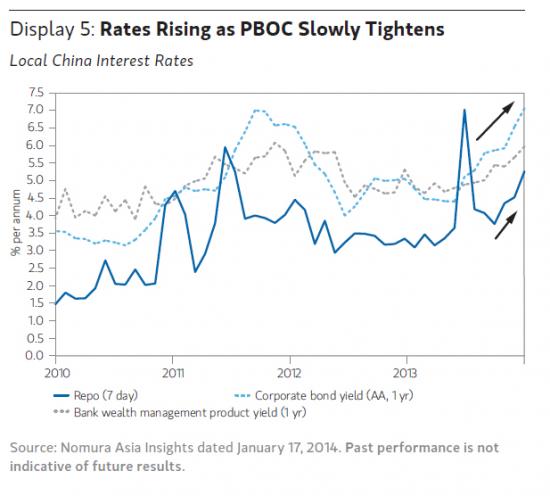

The People’s Bank of China (PBOC) has been slowly tightening credit for nine months. This can be seen in the steady uptrend in interbank financing costs (the one-month Shanghai Interbank Offered Rate, or SHIBOR, is up 220 basis points since last May). The PBOC’s latest Q4 Monetary Policy Report indicates it intends to continue to tighten liquidity in order to control the excessively fast growth of shadow banking credit.

Of the $1.8 trillion in Trust Loans provided by the shadow banking sector, nearly $600bn, or RMB 3.6 trillion will come due in 2014. (Display 4 shows maturities for a sample of half of collective trust loans, which represent one quarter of total trust loans)

Defaults or near-defaults have begun to occur with regularity over the past three months and are likely to pick up in quantity significantly over the next year. As it is becoming more clear that investors may not get all of their money back, interest rates on trust products, wealth management products (WMPs), corporate bonds, and bank loans have risen by roughly 200 basis points in the last year. (Display 5)

So at the same time that large amounts of debt come due and borrowers are increasingly stretched, growth is slowing, monetary policy is being tightened, and market rates are beginning to rise, making new borrowings even more expensive and difficult. The combination of these factors indicates to us that China’s Minsky Moment is approaching.

The unwind of this credit boom is likely in progress, and we expect it to pick up speed over the coming months and quarters. It will likely involve a steady drip of defaults and near-defaults as insolvent borrowers finally become illiquid. Market rates for all assets except central government bonds and central bank bills will likely continue to rise, reflecting increasing market fears of default by shaky borrowers. Asset values will likely begin to deteriorate as stressed borrowers attempt to sell assets to stay afloat. As a result, banks and other financial entities could begin to increase provisioning for bad debts and to reduce credit availability by gradually tightening credit standards. This could lead to a credit crunch where credit to the economy is choked off for all but the safest borrowers.

This rise in defaults, non-performing assets, and credit standards could exacerbate a significant slowdown in economic activity concentrated in the areas most dependent on debt, such as local government infrastructure spending and the sectors with the greatest overcapacity mentioned above.

The impact would therefore be most visible in the fixed investment side of the economy, particularly in infrastructure, real estate construction and related industries (cement, steel, machinery, etc.).

In time, the slowdown in growth and the increase in defaults could become significant enough that the government would intervene and ease policy to moderate the downturn. This policy easing would likely involve a combination of monetary easing and extraordinary liquidity by the PBOC and possibly, some fiscal stimulus. But until then, the impact on assets that are dependent on China’s debt growth and investment spending growth could be severe.

We recognize that it is extremely likely that the Chinese government will attempt to stave off the unwind or at least keep it orderly in an effort to achieve the ever-elusive soft landing. One way that the government could attempt this would be by stepping in to bail out borrowers on the verge of default. A version of this occurred in January, when the well-publicized default of a RMB3 billion China Credit Trust product was averted when an unknown entity stepped in to pay the principal due to investors, though not the remaining interest due (worth approximately 7% of principal). The unknown entity is likely to have been either the local government of Shanxi, home of the coal mining company that defaulted on the underlying trust loan, or the Ping An insurance company, parent of China Credit Trust. The benefit of the government or other entities stepping in to bail out borrowers is that it helps prevent investors from losing money, maintaining their faith in the financial system and ensuring they continue to buy trust products offering rates five times above deposit rates. The drawback is that credit continues to be extended to weak or insolvent borrowers, potentially leading to an even higher level of bad debts in the future. The problem is not eliminated, it is simply postponed. Interestingly, growth is likely to be negatively impacted whether or not the government steps in frequently to prevent borrowers from defaulting. First, scarce capital is being provided to prevent default by insolvent borrowers (“zombies”) rather than being channeled toward productive investments. Second, in order to limit the cumulative size of the bailouts, the government is likely to continue to restrict the growth of shadow banking and lending to these uncreditworthy borrowers. Lastly, market rates are likely to continue to rise, reflecting increasing market unease with the growing number of near-defaults.

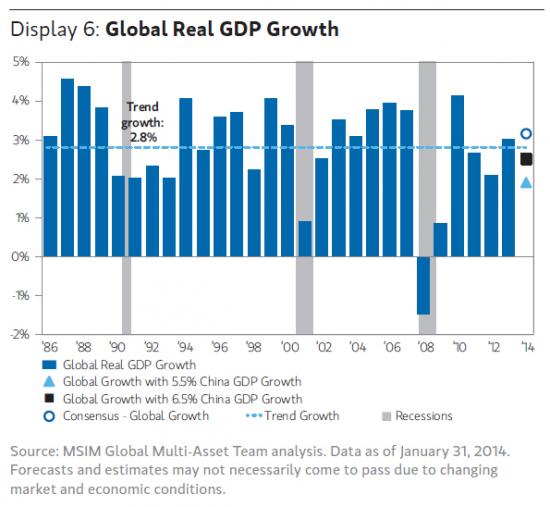

Most other analyses we have seen conclude that China could slow more than currently expected by the consensus, but that the global economy is well-positioned to withstand such a slowdown. Our conclusion is a bit more pessimistic. We have found that every 1% of Chinese GDP deceleration could reduce global economic growth by 60 basis points. On a current dollar basis (i.e., not purchasing power parity, or PPP), the global economy is expected to grow about 3% in 2014 and 2015. (Display 6)

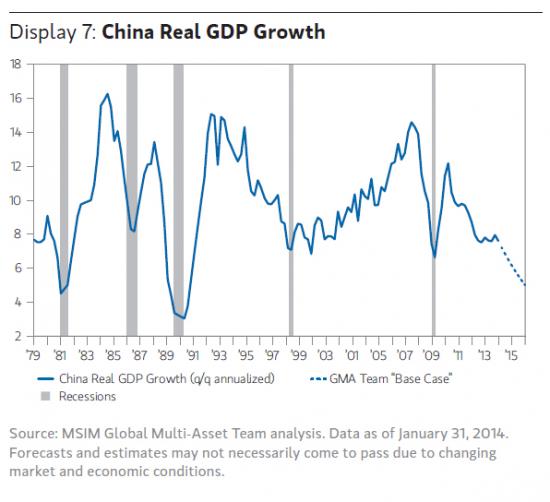

Therefore, if the Chinese economy were to slow by 200 basis points to 5.4%, from current expectations of 7.4% for 2014,13 (Display 7) global economic growth would slow to 1.8%, substantially below potential of 2.8%. This could have a significant impact on global equities, as our analysis shows that the global economy needs to grow at least 2.5% for global corporate profits to grow. Thus, a 1.8% pace for global GDP growth would result in earnings down roughly 13%, a huge miss compared to current expectations of 11% earnings growth. At this point, this is not our base case but a risk scenario we are closely monitoring.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.