Melbourne University economics Professor and tax expert, John Freebairn, has given a great interview to The Age arguing that it’s time to remove the tax rorts around superannuation, negative gearing, and the family home.

According to Freebairn, the first “rort” requiring reform is raising the access age to both superannuation and the aged pension, as well as including the owner-occupied home in the assets test, which is a key reason why a lot of welfare spending goes to those not actually in need:

”You can access your superannuation at age 60. You can access the age pension at age 65. The age pension age was brought in in 1908 when the average life expectancy was just 65”…

”We would slowly bring the access age to superannuation and the access to the age pension to 70. Yes, you have to bring it in slowly. And then I would index it to life expectancy.”

But he says it would take a ”gutsy” politician to reduce access to the age pension. ”It turns out that the age pension is used by about half of mature-age Australians for their sole source of income. Another 20 per cent to 30 per cent have a part pension. And that support is actually more generous than we provide to, say, people who are unemployed on Newstart.”

There is such widespread reliance on the age pension, despite it being means tested against income and assets. The problem, Freebairn says, is that the family home is not included.

”The principal barrier [to change] is political short-sightedness … As soon as I say I want owner-occupied homes to be in the assets test, a whole lot of people will say, ‘Now I have got access to the age pension, but it’s going to be taken away.’ They are going to be noisy as hell.

”What we have got to explain, and have politicians really tell the story about, is this group is really doing pretty well at the moment.

”The more challenging one is that bringing the family home into the assets test is a potential gain for the next generation. They will have less pension income to pay out, so that means their tax rate can come down. It also means we will make it easier for the next generation to purchase their own home.”

Too right. Freebairn’s views not only aligns with my own, but also those of the Grattan Institute, which recently argued that the only part of the tax and welfare system that is not well targeted is for old people. This view is also supported by researchers from Curtin University, who recently found that welfare policies across the period 1984 to 2010 overwhelmingly favoured the elderly at the expense of the young.

Back to Freebairn:

The distortion is exacerbated by so-called negative gearing, which is, in effect, a subsidy from lower-income taxpayers to those who can afford to borrow to speculate on property and financial securities. Australia is one of only a very few nations that allow such speculators to reduce their tax bills by deducting their borrowing costs from their income.

Freebairn, like many others, argues that negative gearing is one of the main reasons first-home buyers struggle to get into the market – there are too many speculative investors chasing properties to negatively gear. About 1.3 million Australian households have negatively geared property investments.

Again, spot on. Negative gearing costs the Budget around $2 billion per year, according to the Grattan Institute, but serves no useful social purpose. Simply, it’s a lurk that must go.

Back to Freebairn:

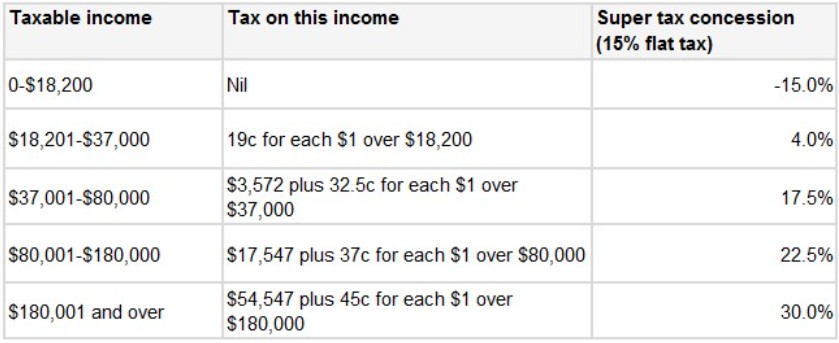

Freebairn says the taxation treatment of superannuation also needs overhauling. People on middle and upper incomes get a huge break by being able to put extra money into superannuation at a tax rate of 15 per cent rather than at their marginal income tax rate. They then get it out tax-free at 60.

”All remuneration, whether it is wages, superannuation or fringe benefits, should be taxed at your personal rate.”

Absolutely. Superannuation concessions overwhelmingly benefit higher income earners (see next table).

According to the Australian Treasury, concessions on superannuation contributions were estimated at $16.5 billion in 2012-13, with concessions on superannuation earnings valued at $15.5 billion. Moreover, the Treasury estimated that the top 5% of contributors would receive 20.3% of contribution concessions, with higher income earners also receiving the lion’s share of the earnings tax concessions.

By providing massive taxation concessions to those on the highest incomes, the Budget loses billions of dollars of forgone revenue. At the same time, the super system is unlikely to relieve pressure on the aged pension, since those that are most likely to need it – lower and middle income earners – receive minimal (if any) concessions, which both hinders their ability to build-up a retirement nest egg and discourages them from making additional contributions.

As argued many times previously, a simple reform that would greatly improve the equity and sustainability of the retirement system would be to abolish the flat 15% tax on superannuation contributions and replace it with a flat concession (e.g. 15%) that is the same for all income earners. A reform of this nature would not only improve equity, since all taxpayers would receive the same taxation concession, but also boost lower income earners’ super savings, thereby reducing reliance on the aged aension and relieving pressures on the Budget.

Back to Freebairn:

Freebairn believes one of the most pivotal reform options would involve a broader goods and services tax base, and increasing it to 15 per cent.

The extra revenue would replace distorting state stamp duties and would fund increases in social security payments and lower income-tax rates for reasons of equity.

Again, this is a no-brainer. The Henry Tax Review showed that GST is a relatively efficient tax – i.e. it has “a low marginal excess burden” (a small loss in consumer welfare relative to the net gain in government revenue) – since it is broadly applied, is difficult to avoid, and does not significantly distort behaviour (see next chart).

Increasing the GST and using the proceeds to replace inefficient taxes like stamp duties and boost social security payments to the poor would improve overall economic efficiency and welfare.

That said, other worthy sources of taxation not mentioned by Freebairn include broad-based land taxes and mineral rent taxes.

While not shown above, both taxes would have similar efficiency to the Petroleum Resource Rent Tax (PRRT) and Municipal rates, since they would be applied to a tax base that is completely immobile – land. In fact, the only loss in efficiency cause by land taxes would come from them being applied non-uniformerly to different land users (as occurs with municipal rates), thereby distorting the pattern of land use. They are also more equitable than consumption taxes, which tend to hit lower income earners harder (albeit deleterious impacts would be mitigated by increased social security payments).

Any discussion about tax reform should, therefore, also include implementing taxes on land/resources in place of less efficient and/or inequitable sources.