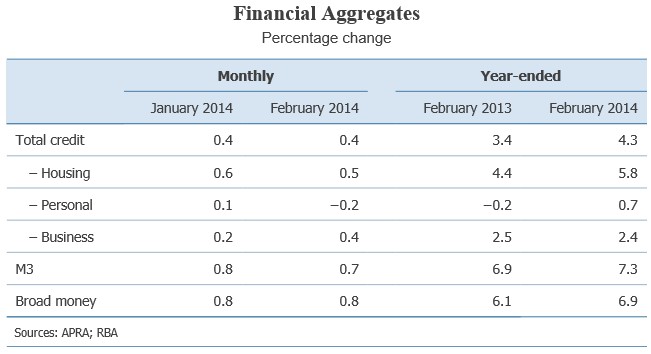

The Reserve Bank of Australia (RBA) today released the private sector credit aggregates data for the month of February:

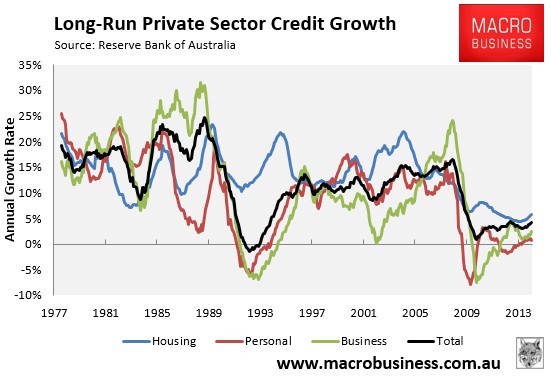

A chart showing the long-run breakdown in the components is provided below:

Personal credit growth (-0.2% MoM; 0.1% QoQ; 0.7% YoY) and business credit growth (0.4% MoM; 1.1% QoQ; 2.4% YoY) continue to grow at a modest pace in annual terms, whereas housing credit growth (0.5% MoM; 1.7% QoQ; 5.8% YoY) has been picking-up, although is remains at fairly subdued levels relative to its long-run average growth rate.

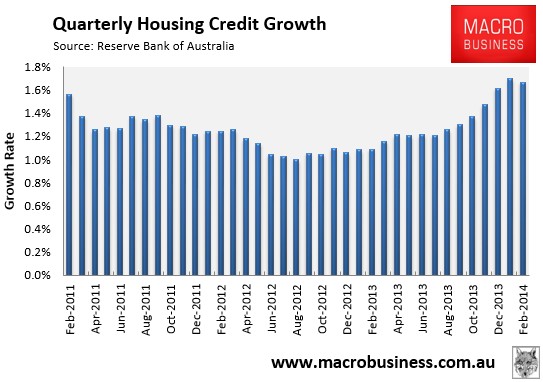

The below chart shows that housing credit growth has begun to slow after accelerating in the middle of last year:

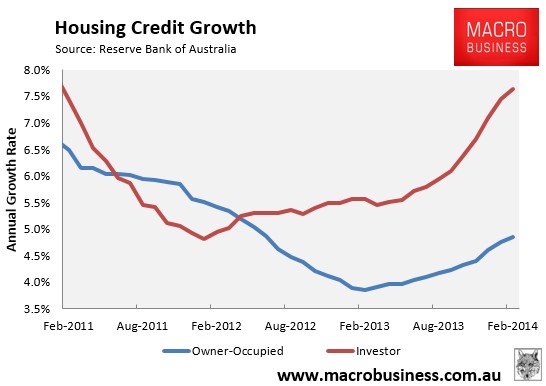

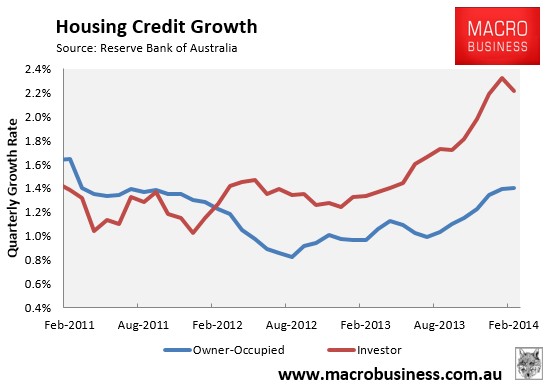

A long-run breakdown of owner-occupied credit (0.4% MoM; 1.4% QoQ; 4.9% YoY) and investor credit (0.6% MoM; 2.2% QoQ; 7.6% YoY) is provided below:

Clearly, much of the current mortgage demand continues to be driven by investors, which has also been reflected in recent housing finance data from the Australian Bureau of Statistics.

That said, investor demand has waned slightly for now, with the quarterly growth rate of investor mortgages registering its first fall in more than a year:

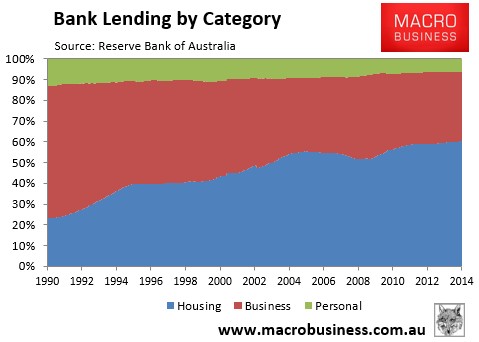

Finally, the share of loans going to housing hit a record high 60.3% in February 2014, whereas loans to businesses hit an all-time low 33.4%:

No wonder housing is killing Australia’s productive economy.

unconventionaleconomist@hotmail.com