It looks like my quick post on the TD inflation number this morning was hasty! With more data, the index is enough to freak uncle specufestor right out! By that I mean that underneath the relatively benign headline, there appears to be pricing trouble brewing for the RBA. From Westpac:

The Gauge rose 0.2% in Feb following on from a 0.1% rise in Jan, resulting in a 1.0% gain the last three months and the annual pace lifted to 2.7%yr from 2.5%yr in Jan. The annual pace of the Gauge is now back in the upper half of the RBA’s inflation target but more critically, there are signs the pace of acceleration may have lifted and the breath of price rises is broadening.

We do caution against reading too much into a single monthly print from the gauge particularly in the strong seasonal repricing months such as Jan and July. But for Feb, Westpac estimates a very mild seasonality of –0.1%mth resulting in an even stronger 0.3%mth rise in our seasonally adjusted Gauge.

TD-MI reports that contributing to the overall change in Feb were price rises for fruit & vegetables, furniture & furnishings, and non-alcoholic beverages. These were offset by falls in holiday travel & accommodation, bread & cereal products, and newspapers, books & stationery.

The price of automotive fuel rose by 1.2% in Feb, and the price of fruit & vegetables rose by 1.7%mth.

The trimmed mean of the Gauge rose 0.3% in Feb following a flat print in Jan and 0.4% in Dec. In annualised terms, the trimmed mean rose by 2.8% over the three months to Feb, following a 2.2% rise for the three months to Jan. In the year to Feb, the trimmed mean rose by 3.0% from 2.7% in Jan.

Excluding volatile items (automotive fuel, fruit & vegetables), the core inflation measure rose by 0.1% in Feb/2.0%yr.

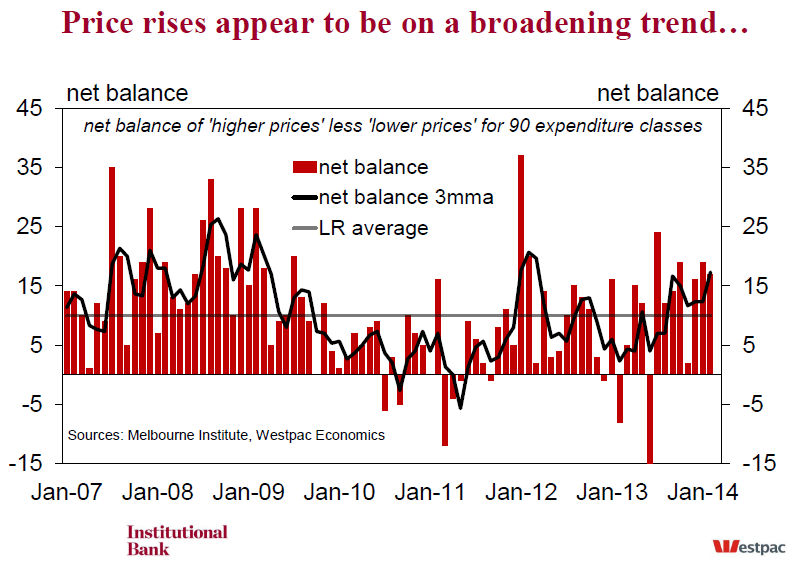

More critically, the broadening in the net balance (number of price rises less number of price falls) continues. At 17 in Feb, the net balance is holding above the long run average of 10. In addition, Westpac estimates the seasonally adjusted net balance fell only modestly from 18 in Jan to 12 in Feb. In 2013, the seasonally adjusted Feb net balance was –14.

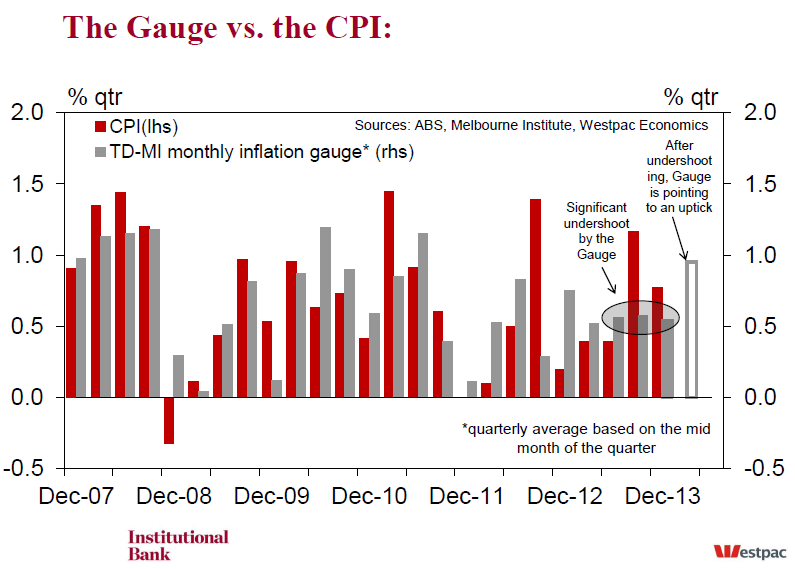

In the Dec quarter, the CPI rose 0.8%qtr and closed the gap with the level of the Gauge. The Jan report is pointing to further modest uptick in inflation which has continued into Feb. Our own preliminary estimates of the partial data suggests upside risks to our current 2014Q1 CPI forecast of 0.6%qtr.

The TDMI used to have a strong correlation with the CPI but its has waned in recent years:

Advertisement

Broadly speaking, however, the index still trades in line with the CPI in terms of trend. Let us hope that this is not the case for the December quarter CPI because if so the RBA will be firmly between a rock and hard place and the dollar will rally just we head off the capex cliff.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.