Tim Toohey at Goldman Sachs today offers a sobering a antidote to the cheerful recent UBS note about it raining jobs in the near future:

Given that the official jobs data will often send a misleading signal in any given month, we continue to lean on our Labour Market Indicator (LMI) to distill the signal from a broad sweep of data points…

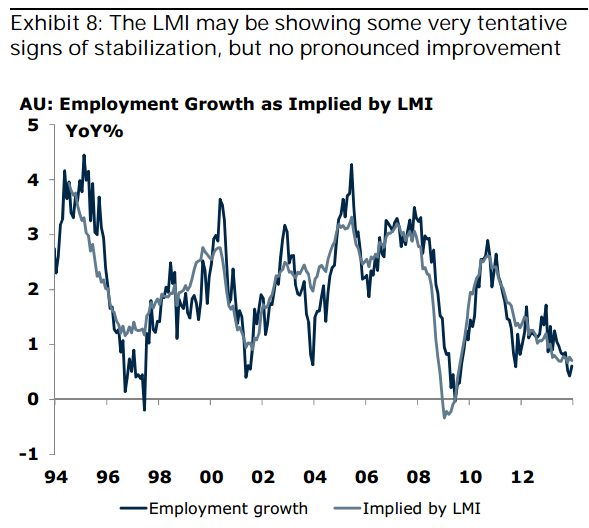

As shown in Exhibit 7, together the 16 subcomponents of the LMI currently point to a similar rate of annual growth in employment as the official data (+0.7%yoy vs. +0.6% yoy; Exhibit 8), with the recent improvement in the ANZ job ads component being broadly offset by an ongoing deterioration in the employment/WAP ratio and long-term unemployment. In turn, the LMI tells a similar story in unemployment rate change equivalent terms, corresponding with the underlying uptrend in official unemployment.

Overall, at best, the recent trend in the LMI might be characterized as a tentative stabilization in employment conditions after a period of protracted weakness. Ultimately, jobs growth continues to track at a clearly below-trend pace, jobless claims remain elevated (Exhibit 10), turnover and structural change metrics are subdued (as is the norm in a weak labour market; Exhibits 11 and 12) and there is little evidence in support of the apparent sharp turnaround in conditions suggested by the February Labour Force report.

Looking ahead, we expect both rising jobs growth and rising unemployment

…while we caution against extrapolating forward February’s rapid jobs growth, we do expect total employment to gradually trend higher over the coming quarters as the non-mining recovery gains traction. Indeed, on average, our employment forecasts embed an average monthly jobs growth of +10-15k a month over the remainder of the year (skewed to 2H2014).

The unemployment rate is also likely to rise, however, even as employment growth turns the corner…as a healthier labour market encourages some recently detached workers to re-engage, even a stabilization in the rate of participation will be sufficient to drive the unemployment rate up to a cyclical peak of ~6.2%.

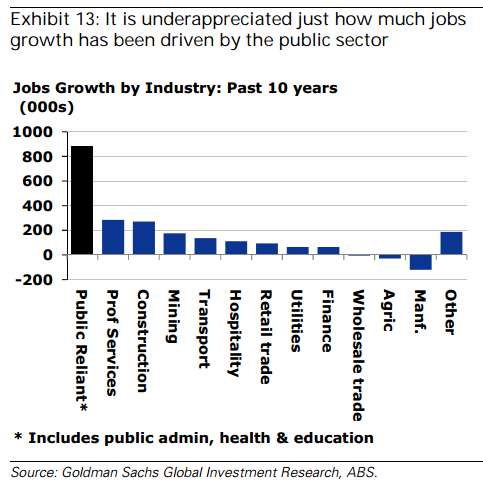

Where will the jobs come from? As public growth slows and mining unwinds

Over the past decade, more than 40% of all the job creation in the Australian economy has been concentrated in public administration and other sectors highly reliant on public funding (e.g., health & education; Exhibit 13). In context, the contributions from the next strongest contributors (professional services: 13.4%, construction: 12.8% and mining: 8.3%) have been relatively modest. Looking ahead, however, with the mining construction boom going into reverse, and all levels of government experiencing multi-year constraints to their fiscal capacities – a key question is where future employment growth is likely to come from?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Looking ahead, we expect both rising jobs growth and rising unemployment