One of the great races of Australia corporate history continues under the radar (if the Australian press deserves a moniker so precise). From Credit Suisse:

Comments by the CEO at Credit Suisse’ Asian Investment Conference in Hong Kong (reported by Dow Jones) indicate that FMG remains focused on debt repayment for the next two years and further massive expansion plans are not being worked on. FMG is aware of the threat that iron ore production might outpace demand and has not looked at the 355Mtpa scheme for a while. This should provide comfort for investors nervous that FMG might launch off on another big expansion. FMG has other plans for cashflow – it wants to repay another ca.$3bn in debt by the end of 2015.

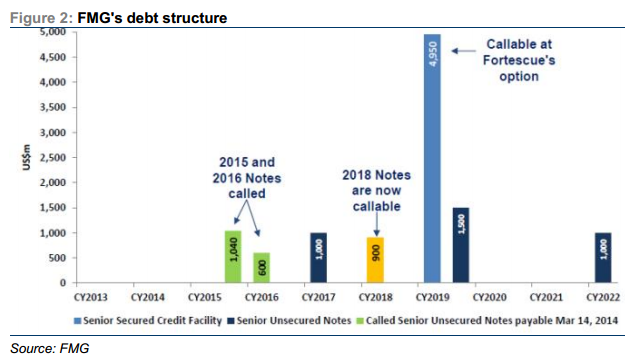

FMG noted its net debt will be around US$7.8bn by the end of the month. Assuming FMG has excluded about $300mn of finance leases, then its cash balance will be $1.6bn and it is running about one quarter ahead of our gearing reduction forecasts (we forecast 40% by the end of CY14). However, FMG may have boosted cash with further iron ore prepayments.

FMG’s plan to repay another billion in CY14 implies it may repay the $900mn note (6.88% interest) that is callable this year. This has a pricey 5.2% early call penalty. In FY15, FMG wants to repay $2bn, but we assume it will actually do $2.5bn, comprising a $1bn note (6%) and a $1.5bn note (8.25%), the latter having the highest interest rate in the debt stable. We doubt it would repay the $5bn secured facility as the cost will fall to a lowly L+2.75% by mid-year.

Catalysts: FMG will report its MarQ production results on 17 April. The market will be watching the result closely to see whether FMG’s guidance of 127Mt shipments for FY14 is achievable.

So why is FMG repaying its debt so aggressively, so far ahead of schedule and at greater cost than if it let it run it’s course? The answer tells you all you need to know about where it really thinks that the iron ore price is headed as the supply deluge arrives and China reforms itself.

Advertisement

It will be a tragedy if Andrew Forrest and company lose the race. He is the clear pick of the boganaires, earned his way and has a charitable soul.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.