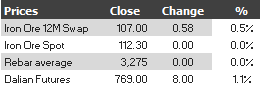

Here are the iron ore charts for March 28,2014:

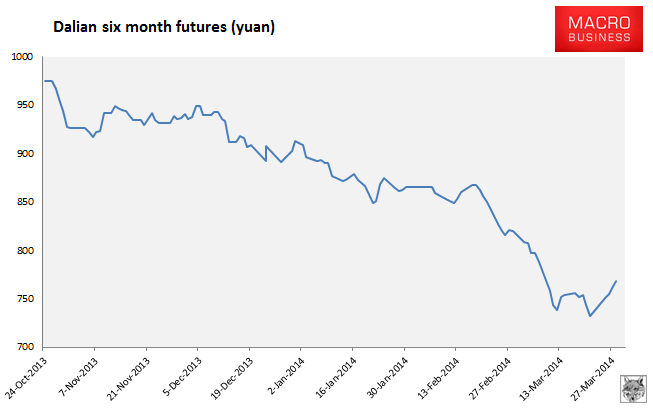

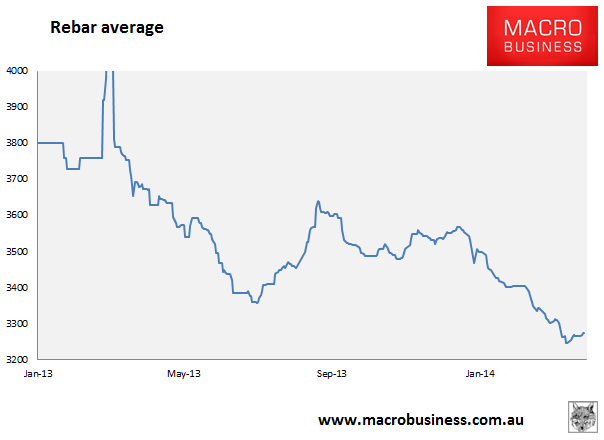

Friday rumours of Chinese stimulus boosted paper markets with rebar futures up a decent slab as well. Dalian in particular has a constructive chart with a juicy double bottom in place suggesting upwards momentum could continue.

Yes physical markets are still subdued with port stocks up slightly 0.35 million tonnes to nearly 111 million tonnes, rebar average is still stuck at record lows, spot is flat and the the Baltic Dry down another 1%.

In news, CISA high frequency data for steel output for mid March was out and continued its subdued growth. The average aggregate daily production was 2.096 million tonnes, a slight fall 0f 0.44% from the ten days prior. Despite this, steel inventory rose 2.26% to 17.03 million tonnes, reversing the prior periods decline. Not bullish, either.

According to Reuters, buyers remain choosy:

“Buyers are more interested in mainstream cargo than those from smaller suppliers such as Malaysia and Indonesia because the prices are still relatively low and the quality is better,” said a trader in Tianjin.

“I’m selling some Malaysian cargoes of 52-percent grade at around $70 a tonne, but not getting so much interest although I’m willing to negotiate.”

A cargo of 57.6-percent grade Australian Yandi iron ore fines was sold at $100.89 per tonne on Thursday and 61-percent Pilbara fines traded at $113.20 a tonne, traders said.

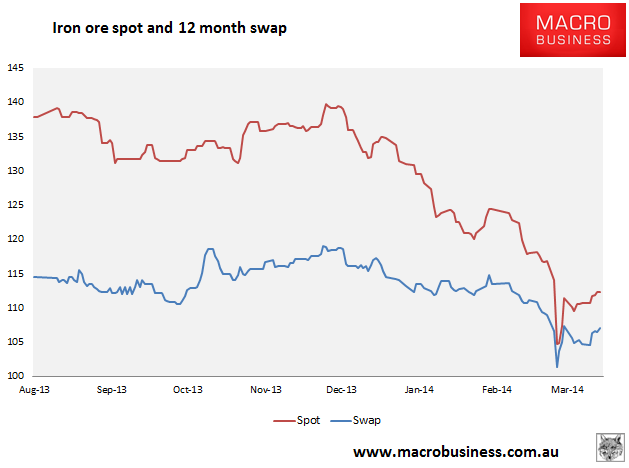

The benchmark 62-percent grade iron ore for immediate delivery to China .IO62-CNI=SI rose 0.4 percent to $112.30 a tonne on Thursday, according to data provider Steel Index. It has gained 1.4 percent for the week.

The price of iron ore, China’s top import commodity by volume, remains about $2 below where it was before an 8-percent rout on March 10 dragged it to its cheapest since October 2012.

Further gains will hinge on whether steel prices in China are able sustain their upward momentum. But some traders say an anticipated increase in global supply may limit any recovery.

“We’re not buying iron ore yet. We’re holding the view that the market will have another round of decline so we’re not taking any position now,” the Shanghai trader said.

As I wrote in another post today, I expect China to keep the foot on the brake as it hits the accelerator. We’ll get some steel sensitive stimulus in infrastructure but the tight credit conditions will remain, keeping pressure on ponzi borrowers. The upshot is we might get some more gentle upside pressure in the spot price but still no restock unless more aggressive spending is forthcoming.

Finally today, a piece on Dalian futures caught my eye at The Australian:

FLEDGLING Chinese iron ore futures traded by speculators and small-time industry players are giving accurate predictions of moves in the iron ore spot price, which has become increasingly important to the health of Australia’s biggest miners and national export revenue.

…Correlation analysis shows the most-traded Dalian iron ore futures contract this month and Platts’ The Steel Index iron ore price had a correlation coefficient of 0.82 — which in statistical terms makes them highly correlated (a coefficient of 1 means they always move in unison).

Yes, Dalian has been reasonable in this regard, but no more so than swaps before it. Both sets of futures still move too much in reference to the short term in my view.