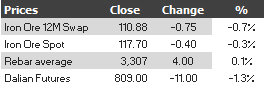

Find below the iron ore price tables for March 3, 2014:

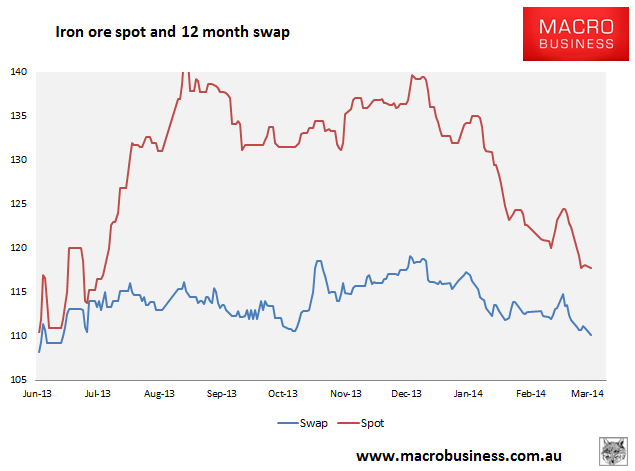

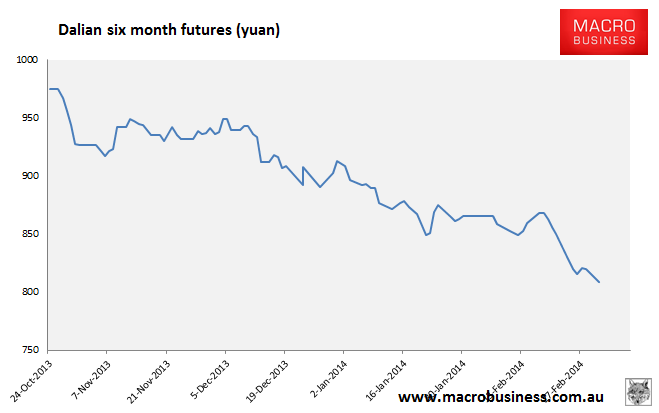

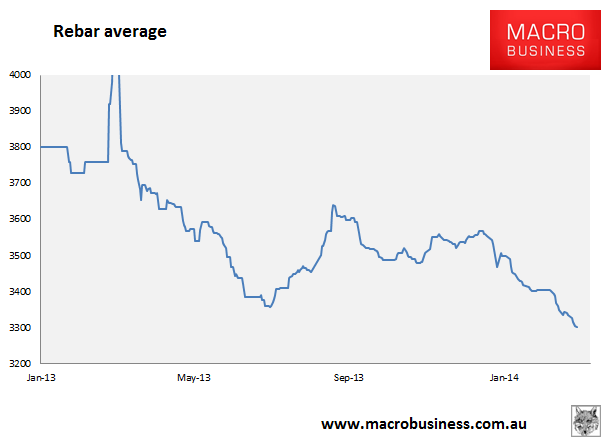

A marginal new low for spot, 12 month swaps have broken their mid 2013 support and Dalian futures are in free-fall. But rebar finally found a bid! Rebar futures also bounced a little.

For me this shows that there are still bids in the physical market and steel prices are looking for a finding a bottom as real activity slowing emerges after the Chinese winter. There is no doubt, however, that the abundance of ore in the supply chain is overhanging the market and derivatives are acknowledging that fact. There may also be some hope of stimulus emerging from the National People’s Congress.

From Reuters:

“We still have not seen much improvement in steel demand and I think it will be difficult to see a strong recovery even after the parliamentary meeting,” said an iron ore trader in Shanghai.

…The annual meeting of China’s parliament, the National People’s Congress, will kick off on Wednesday and expected to last around nine days. Signs of slower economic growth in China are curbing hopes of steel demand, with activity in the country’s factory sector reaching an eight-month low in February. A separate private survey showed manufacturing activity at its slowest in seven months.

The sustained increase in stockpiles reflected arrivals of iron ore contracted by Chinese mills under long-term deals with miners, traders said, as well as the growing use of the commodity as a loan collateral amid tight credit conditions.

Some of the mills holding cargoes at the ports were trying to sell them because they have enough material to run their steel plants that are operating well below capacity, said another Shanghai trader.

“Some mills are still buying spot material because they’re still producing steel but they’re only buying what they need.

Activity is very slow,” he said.

In this situation, any day when Chinese mills are not aggressively destocking is a good day. That risk remains.