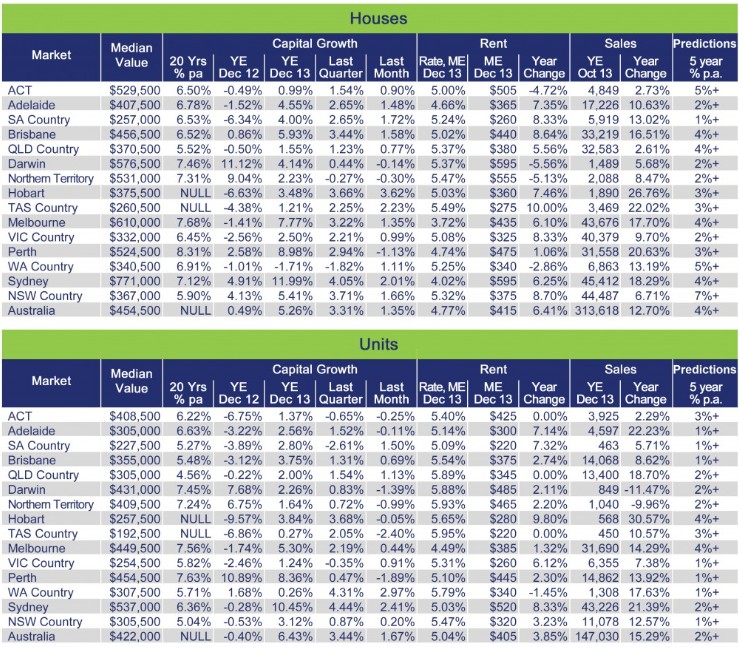

Residex has just released their December home price results, which revealed strong growth in December, with national values up by 1.35% (houses) and 1.67% (units):

According to Residex’s founder, John Edwards, mortgage affordability constraints have turned Sydney and Melbourne into renters markets, whereby it has become very difficult for a typical family to achieve home ownership:

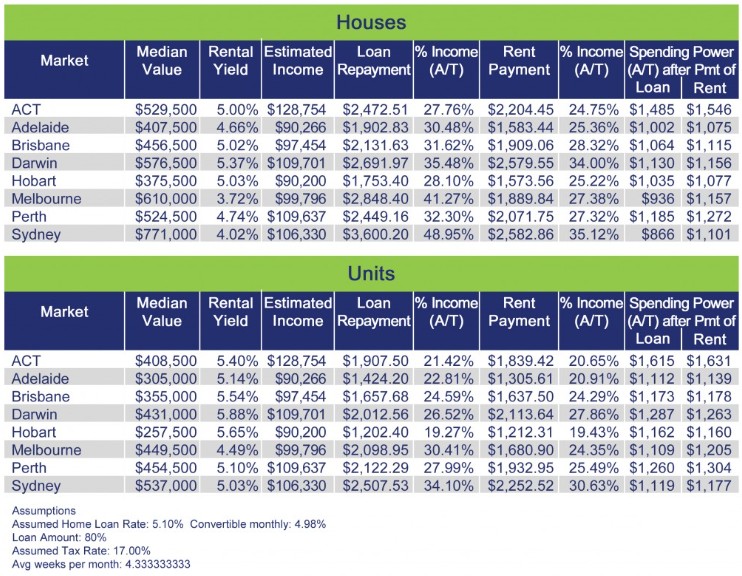

Table 2 [above] demonstrates that it is very difficult for the median family in Sydney and Melbourne to support a family on the remaining cash following home loan repayments. This suggests that First Home Buyer (FHB) activity should be under represented in these markets, which is in fact the case…

Further analysis reveals that the FHB have largely been replaced by investors. The percentage of FHB in the market today is probably the worst recorded in history, and is the worst recorded by the ABS.

Sydney and Melbourne are moving to be renters markets where investors (both local and international) and superannuation fund investors are the owners of residential property. The latest releases on investor activity by the ABS confirms the growing activity of these two groups…

The Sydney market has traditionally been the leader in trend setting. However, like Melbourne, it is in uncharted territory. These markets are maturing and an unfortunate consequence of this is the increasing unaffordability in the markets. However, when looking at mature markets throughout the world, particularly in Europe, you can see that renting is more the norm than ownership.

The uncharted aspect relates to investors driving growth. There is little to no history on how investors will behave as we move forward. This group is driven by greed and risk issues, and they do not have the same constraints as owner-occupiers. Investors generally have significant amounts of security so banks/lenders are happy to provide them loans in a market where there is strong competition for quality lending. Currently, housing provides low levels of risk and reasonably good returns, hence their interest in this asset class. Further, interest rate increases have less impact on this group due to interest deductibles for taxation.

The above is a recipe for substantial increases in rents, which will significantly diminish the standard of living in the longer term for the next generation. For the existing homeowner/investor, this will create solid security and secure superannuation investment opportunities. However, in the longer term, it will cause problems for governments who will have to act to find a solution at some point in the future as rental affordability becomes unacceptable.

How governments will solved the looming problem is unclear as we live in an international global environment where lending restrictions can be circumvented by foreign investors simply borrowing in their own country. We have allowed foreign investment in new dwellings in an effort to boost housing supply, which needs to continue. However, if property is simply delivered and unsold for the purposes of speculation (as may be the case with many international buyers) then the problems are simply made worse as scarce city land supply is reduced without providing supply. Should we simply stop foreign investment? Probably not, but I suggest that there should be limits on the volume of foreign capital invested into new housing in any one year.

Many people will suggest that we should remove tax incentives. This also won’t be the solution as it will simply cause existing property owners to hold onto their assets and diminish their supply side activity at the same time. Housing will remain unaffordable and will become worse as rental costs become unacceptably high.

Basically, the government has to carefully create a situation that causes housing costs to stagnate in the unaffordable cities so wage inflation can gradually allow housing to become affordable. However, in saying this, it cannot afford to cause housing to decrease in value too rapidly as this would cause significant economic issues for the state government. It can do this by reducing demand for housing stock in the unaffordable markets. It is possible that this will happen naturally as housing becomes excessively expensive and hence the population is given an incentive to move away from unaffordable markets. However, the government needs revenue from housing stamp duties and hence has to maintain selling activity. At the same time, the government also needs the population to grow. Therefore there is one option – cause the population to disperse throughout the state. To do this, the government needs to create job opportunities in regional areas by causing industry to regionalise. Hence, the government has to offer industry incentives to do this. No matter what the outcome is, it is difficult to see a situation where housing prices decrease in value and rentals do anything other than increase in the medium to longer term.

The above discussion highlights some of the implications arising from the housing quango created by Australia’s governments. Instead of allowing the market to function normally, they have choked supply through restrictive planning, taxes on development, and other means, while simultaneously pumping demand through tax incentives, high immigration, and lax enforcement of foreign ownership rules. To add insult to injury, state governments have become addicted to property-related taxes, making them naturally opposed to undertaking reforms that would free-up supply and improve affordability.

That said, I disagree with Edwards that removing tax incentives, such as negative gearing, would be counter-productive. As shown many times before, negative gearing has substantially increased investor demand, pushing-up property values, but has done absolutely nothing to improve supply or keep rents down. Moreover, Edwards himself argues that the increased ownership by investors “is a recipe for substantial increases in rents”, so using his logic, why wouldn’t a policy change that reduces investor demand improve rental affordability?

I also disagree with Edwards that “it is difficult to see a situation where housing prices decrease in value”. What Edwards is effectively saying is that ‘Australia is different’ and immune from a significant housing correction. Yet, similar arguments could have been used in a number of “mature markets” around the world – many of which experienced big price corrections at some time over the last decade. There are plenty of emerging risks: the unbalanced nature of the rally itself, the capex cliff and car industry woes, a Chinese housing pop, rising interest rates on tradable inflation. All could easily decrease house prices.