The NAB Business Survey for January is out this morning and shows ongoing recovery:

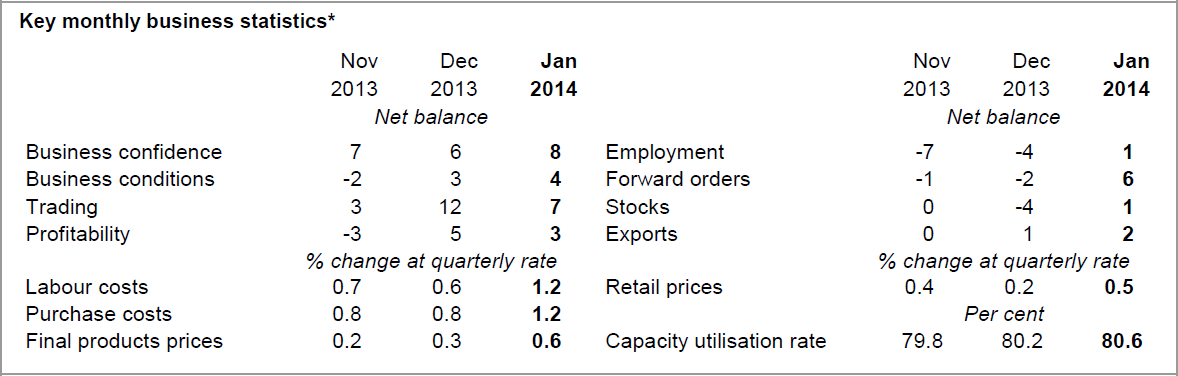

More encouraging results. Business conditions maintained last months momentum and is approaching 3 year highs while confidence was up for the first time in 4 months – both near or above trend levels. Employment index much better, but still suggests soft labour market conditions. Sales and profits dipped slightly, but still healthy. Sharp turnaround in manufacturing – surprising in the current environment and will need a lift in domestic demand to be sustained. Better forward indicators give some comfort about near-term outlook. Price inflation still moderate, but driven higher by upstream pressures. Unemployment key to rate outlook. Upside risk to near-term growth forecast, but fundamental outlook unchanged. Final RBA cut to occur in late 2014.

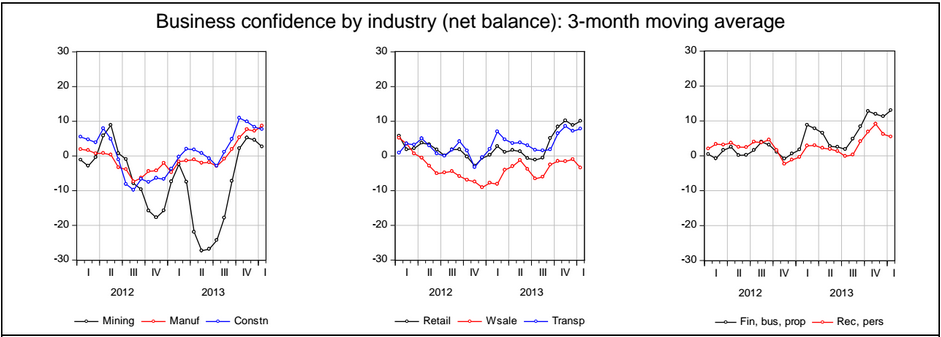

Business confidence recorded its first rise in four months in January, to be above long run average levels. Now that conditions are on the rise, confidence may continue its run of surprising (post-election) resilience for a while longer. Confidence is now positive for most industries, although wholesale (a bellwether industry) and mining are both negative – significant given the increased importance of mining to the Australian economy. Confidence is generally positive across all states.

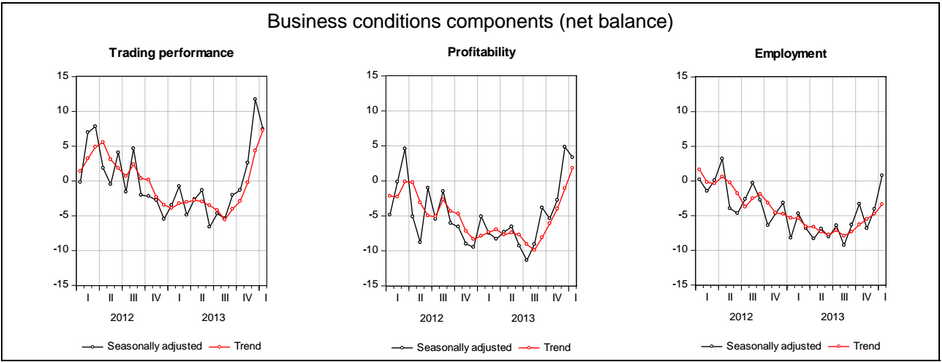

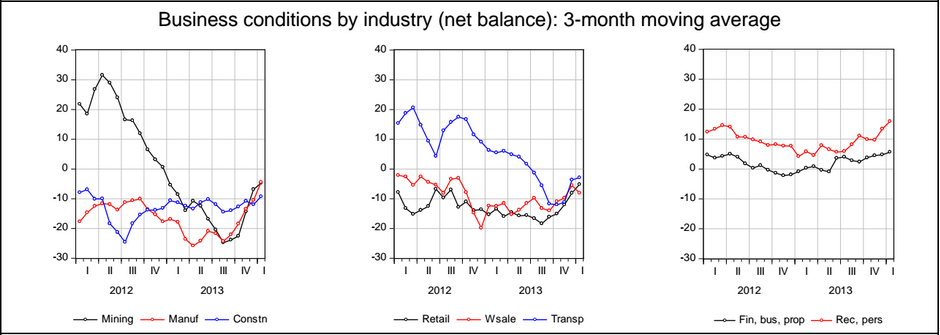

Business conditions consolidated the strong pick up in December, reaching an almost 3 year high. Overall conditions are still chasing confidence, but are now close to their long run average. Manufacturing recorded a surprisingly strong turnaround – somewhat counter to other industry indicators. The next best improvement was in construction, followed by retail. All other industries deteriorated. Forward orders look more supportive of better conditions, but capacity utilisation remains below long run averages, and the employment index still suggests a jobless recovery.

Our wholesale leading indicator suggests much weaker underlying conditions, pointing to below trend demand growth continuing into the first quarter of 2014 at around 3%. Against that, the improving trend in business conditions (if maintained) implies underlying GDP growth of around 3¾% in Q1, well above our forecast.

Inflation pressures remain subdued, but are building on the back of rising costs inflation. Labour costs growth is restrained, consistent with increasing slack in the labour market, but lifted in the month. Purchase costs have shown a similar trend.

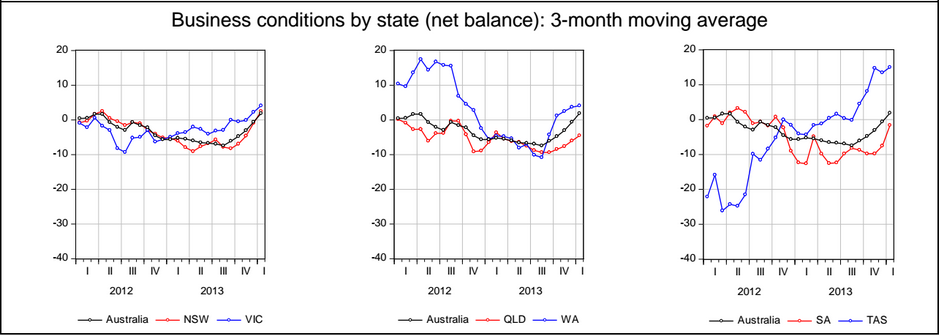

The cyclical bounce carries on then. The recovery in employment is encouraging but remember that this survey is light-on in mining. No mistaking the bounce in eastern services economies, though:

Advertisement

Advertisement

I still expect it the cycle to erode as the year progresses but a good report today. Full report here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.