MB Members Special Report: Asset allocation in an era of Dutch disease

In the 1970s, The Netherlands enjoyed a North Sea gas boom. But the resulting macroeconomic impact of a rising real exchange rate meant that it also suffered a material decline in manufacturing output. At the time, The Economist magazine described this phenomenon as Dutch disease. It has since been described in various forms as the “resource curse” or in Australia as the “Gregory effect” after economist Bob Gregory.

The existence of Dutch disease is uncontroversial. It has been seen to take effect in various countries where an endowment of natural resources has resulted in boom conditions.

As well as the Netherlands and Australia in the 1970s, prominent examples include the UK and Norway and Nigeria in the 1990s and Russia in the 2000s, as different oil and gas discoveries boomed.

Is Australia currently suffering a renewed dose of Dutch disease? And if so where are we in the cycle and what are the implications for stock investment?

What is Dutch disease?

The key to understanding the phenomenon of Dutch disease is it impacts on the real exchange rate, which is a calculation based upon the combined value of a nation’s currency and its goods and services (that is its inflation). A boom in the resources sector can inflate either the currency, the inflation rate, or both, depending upon factors such as labour market flexibility and currency convertibility. Either way, the end result is a loss of competitiveness in tradable sectors like manufacturing.

Australia’s last two commodity booms are illustrative. During the 1970s boom, the country had a fixed-rate currency so much of the inflation transpired in wages as the need for labour expanded beyond capacity.

In our recently ended and even larger commodities boom, the Reserve Bank of Australia (RBA) made a conscious decision to prevent a repeat of this wage inflation by instead raising interest rates and pushing the currency very high. The result was a shakeout in tradable sectors (those that export or compete with imports) which meant demand for labour fell in those areas and could be soaked up by rapidly expanding mining. This is known as a structural adjustment.

The RBA largely succeeded in preventing a wage cost breakout (at least beyond a few narrow sectors) but the result has still been Dutch disease, with a three year recession in manufacturing and weakness in other tradable sectors including retail via the internet.

Undoing the damage

A commodities boom is a welcome phenomenon but if it is not managed well, it does leave a legacy of damage that needs to be repaired over time.

In the earlier of our two Australian cases, much public policy of the 1980s was aimed at undoing the rampant wage inflation unleashed by the boom – with successive wages accords slowly deflating the input costs to production. Competitiveness was also restored through the float and subsequent falls in the Australian dollar.

The RBA chose a different course for the economy this time firstly because it had a floating exchange rate at its disposal. But secondly, it did so because it judged the commodities boom to be more enduring than those that we had experienced before. Thus a permanent (structural) adjustment to more resource exports and less non-resource exports made sense to it.

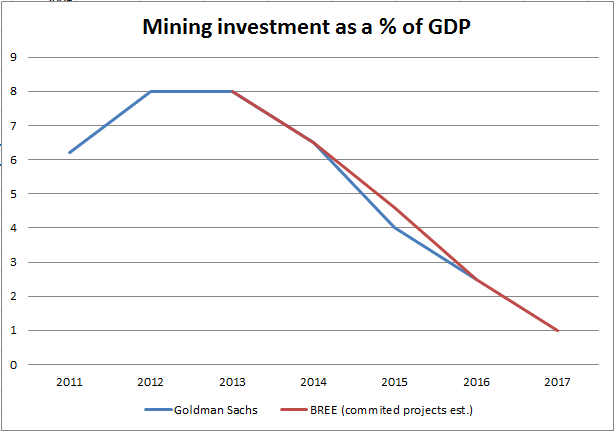

The notion of permanence will probably be true to the extent that for a long time to come Australia’s terms of trade (ToT, the ratio of our export prices to import prices) will remain higher than they were prior to 2003 owing to increasing global scarcity in many commodities. But it is not as true as the RBA assumed. The boom has ended earlier and more suddenly than it anticipated and the bank finds itself facing ongoing falls in the ToT and dramatic falls in mining investment over the next three years without an obvious replacement to drive growth:

There will be some offset in the so-called “third phase” of the boom, which is when the volumes of shipments rise. But commodity price falls have so far outstripped those gains (and will likely keep doing so) as a wave of supply comes to market, so another source of growth must be found.

Enter “rebalancing”

The RBA (and Treasury) have turned to housing to fill the gap. Although the rate cutting cycle has eventually produced a response in property prices and a more subdued return in construction, this avenue for growth is also limited.

Given Australian households’ already very high exposure to mortgage debt, authorities do not want to see an extended housing boom. The RBA has repeatedly stated that it would like to see house prices growing at the rate of income (its target is more for construction) and Glenn Stevens has directly warned Sydney housing speculators to back off (without much luck so far).

Signs are everywhere as well that after years of holding on, major Australian manufacturers are now capitulating to an overly slows rebalancing process. The closure of the three major car manufacturers as well as Electrolux and potentially SPC Ardmona will weigh on consumer confidence and a labour market struggling to absorb with workers pouring back into the economy as mining projects are completed.

Complicating matters, the RBA is still stuck with a high exchange rate and does not want to raise interest rates but it recently mentioned it is canvassing macroprudential rules along the lines of those already deployed in New Zealand, such as loan-to-value caps.

This talk will increase if housing does not slow and there is a rising probability that the policy will be enacted.

In short, housing is still not enough for Australia to retain full employment, which is why the RBA has worked very hard in recent months to lower the dollar and begun to discuss a real exchange rate adjustment.

The heart of Dutch disease

This is the heart of the matter. The combined inflation of the currency, wages and prices must be reversed so that non-resource exporters and import competers can become competitive enough to invest again and fill the growth gap left by Dutch disease.

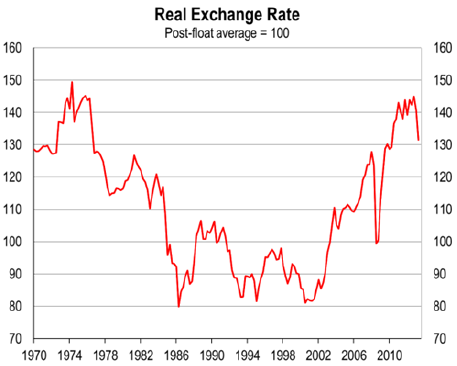

Some of this can be achieved through the accumulating falls in the currency. But even the 21% decline in the dollar since its peak at $1.10 has only made a small dent in the REER:

Many of the bilateral charts are far worse than this basket chart. Australia’s REER against our non-resource competitors in developed markets like the US, UK and Japan remain at unprecedented levels.

Crucially, to rectify this, the dollar must fall much further. But more, as that induces inflation in tradable products at home, wages must not be allowed to rise in response or the devaluation is lost in inflation and competitiveness is not improved. In short, to cure Dutch disease you need a real devaluation with falling real incomes. That is the key to understanding macro investment trends in the years ahead.

So much for theory!

This diagnosis leaves Australia with a political problem. Reducing wage growth and making people poorer (so that fuller employment can be maintained) is not the kind of political narrative that is easily sold to the electorate. In an era marked by cowardly professional politicians addicted to “kicking the can” rather than solving problems at their root, there is every chance that authorities will ignore what is needed in favour of shorter term stimulus measures.

The RBA has noted the need for a real depreciation in Australia but the Abbott Government most has not. Indeed it appears bent upon restoring Australia’s growth rate as soon as possible. Both the treasurer and prime minister have endorsed rising property prices and are fast-tracking infrastructure projects without the appropriate analysis to gauge their productivity benefits.

The government appears intent upon replacing one building boom with another but in the medium term this will not suffice. The only thing that can repair Dutch disease is improved competitiveness no matter how much authorities seek to delay it.

More encouragingly, they have mentioned a need to improve competitiveness even if their micro-economic reform agenda is timid. If it comes to it and the RBA needs the Abbott Government’s help to prevent a wages breakout as tradable inflation bubbles then they should deliver.

If they don’t, and the RBA is forced to hike interest rates to prevent wage inflation, then competitiveness will more likely improve via recession as housing busts.

Where to invest

An environment of intermittent inflationary bursts but weak household incomes is a hard place to be for investors. It may sound like stagflation, which is ugly enough, but it isn’t because there is no persistent inflationary pulse in wages owing to the falling terms of trade, a weak labour market as mining investment unwinds, as well as the RBA’s inevitable move to cap housing inflation.

That means interest rates will remain low despite the inflationary bursts coming from a falling dollar. The RBA understands all of this and will “look through” these bursts.

The first point to note is returns in cash are unlikely to rise (as they do in a stagflation). Monetary policy will not be tightened and when it does it will be slow. Still, the inflationary bursts will also hamper more rate cuts, at least until the RBA innovates with macroprudential tools. When that happens, bonds may prove more attractive as interest rates fall further.

That will be a boost for share market valuations (the price component of P/E). But here too there are problems. On the earnings side of the equation, typical cyclical growth stocks like consumer discretionary will not benefit as much as they normally would because incomes and jobs growth are held back.

To make this more complicated still, defensive stocks like the banks will find themselves in a slowing housing market with struggling consumers. With their bad debt provisions already wound down, cost structures fairly lean and credit growth muted, profit growth will get tougher.

Yet all of these sectors are already priced for stellar growth. Not so aggressively as past cycles but aggressively enough. The likelihood is that these cyclical growth sectors will see earnings rise early in the cycle but less so as it wears on and the great Dutch disease adjustment proceeds.

The one relative certainty in a post Dutch disease context is the currency must fall. Without that, there can be no repair to non-resources tradables. Dollar-exposed firms are the great beneficiaries of a real depreciation and it is here that investors should be picking their enduring cyclical growth winners.

Miners versus industrials

That points to one outstanding sector where the value is obvious. Mining valuations are low and they will be the biggest beneficiaries of a falling dollar on the market. But there is a rather large caveat.

The entire process of shaking out Dutch disease is the result of the end of the commodities boom. That end is still playing out, most especially in the bulk commodities that dominate earnings. Thermal coal is at the forefront of the correction and has fallen in price a lot already as well as seen some rationalisation in global production. There’s further to run not least because China is likely to move away from coal-fired power as quickly as it can owing to unrest around pollution. But it may be that miners here have less downside in price to worry about.

Coking coal has also fallen a long way but has further to fall. Production remains high and as a key ingredient in steel it is very exposed to China’s “rebalancing” project (the shift from investment in building to consumption to drive growth) that has brought the global commodities boom to a close. Coking coal has further price downside and rationalisation ahead.

The big one is iron ore, which is still trading at exceptional prices. The iron ore supply glut is upon us just as China is slowing again. Its price will fall again this year and very sharply if China does not boost growth with more stimulus, which its leaders have ruled out because by definition such prevents rebalancing. If they are good to their word (and last year they were not) and no more stimulus is forthcoming then there is a high risk that iron ore will trade at an average of $100 and below this year and lower again next year. Such average prices imply downside spikes to $80 and even lower.

Neither volume growth nor a falling dollar, nor cost reductions will be enough to offset severe price declines and high cost producers will be threatened.

A better investment strategy is to look to Australian firms that are exposed to the falling dollar but not to China’s transformation, the dollar-exposed industrials and energy firms. These will also be exposed to the improved conditions in developed markets and ongoing global carbon mitigation.

There are serious questions over Australia’s gas boom in terms of long run viability owing to high costs of production and being the marginal cost producer. But those concerns are long term, particularly from 2018 onwards when US gas begins to flow. In the meantime, as local LNG projects approach completion, exports will flow and project risk will diminish. That’s an argument in favour of the sector for a medium term punt.

Industrials with developed economy earnings are the most natural fit in a post-Dutch disease environment. They are leveraged to the global, and especially developed, economy recovery and will benefit greatly from the falling currency. Most importantly are not exposed to the vagaries of a highly questionable Chinese transition. These are the long term growth stocks of the cycle.

It is either those or consider offshore investment.

—————————————————————————————————-

Finally today, here is your MB traffic update, which is faring better than our economy is: