By Catherine Cashmore, a market analyst and journalist with extensive experience in all aspects relating to property acquisition. Follow Catherine on Twitter or via here Blog.

To a limited extent inequality and the ‘rich/poor’ gap is tolerated within society because economists have historically seen it as a necessary platform to stimulate ‘economic progress’ or even activate a sense of competitiveness within individuals in order to elevate themselves up the social ladder.

Certainly in the housing market this is evident. Who hasn’t aspired to their ‘dream’ home – or visualized some improvement similar to that of their neighbours?

It’s what the success of programs such as ‘Grand Designs’ thrive upon – the emotional aspect of ‘wanting’ bigger and better – and a proportion of home owners will stretch their budget in order to achieve their desired property of choice, taking on a larger mortgage to do so.

However, whilst a degree of inequality may be tolerated as an inevitable consequence of the benefits offered in a capitalist society, a widening gap can become disabling to ‘progress,’ or even dangerous, if items of basic need are perceived to be increasingly out of reach.

In their 2012 ‘Global Risks’ annual report, the Word Economic Forum put it like this:

“…when ambitious and industrious young people start to feel that, no matter how hard they work, their prospects are constrained, then feelings of powerlessness, disconnectedness and disengagement can take root. The social unrest that occurred in 2011, from the United States to the Middle East, demonstrated how governments everywhere need to address the causes of discontent before it becomes a violent, destabilizing force.”

The comments build on other research undertaken by Andrew Berg and Jonathon Ostry, two senior staff in the IMF’s Research Department, who found that once a country had entered a period of economic growth, the more equal the distribution of wealth over the ensuing period, the longer it lasted. They conclude “…sustainable economic reform is possible only when its benefits are widely shared.”

Inequality in Housing

The consequences of inequality in the housing market are painful and slow. The trend is increasingly evidenced over a lengthy period of years – not in the volatility of month-to-month first homebuyer statistics – always marginalizing those at the bottom of the income stream, whilst advantaging those at the top.

Effects include:

- Social polarization,

- A decrease in the number of low income buyers obtaining ownership,

- A drop in the number of affordable rental dwellings with demand outstripping supply,

- Greater requirements for public housing,

- A rise in homeless percentages, and those who drift in and out of secure rental accommodation.

- A rising percentage of long term tenants, and falling percentage of property owners, – across all demographics, – but particularly families with children.

- Fewer Australians – across all demographics – owning their homes outright.

- Evidence of severely crowded accommodation…. And so forth.

The list, which names only a few of the prevailing concerns, creates a growing body of evidence that we have more than an affordability issue in Australia, which focuses overwhelmingly on first home buyer figures.

We have a growing structural problem, which, if allowed to continue, with have a societal impact, chipping away at the future growth and stability of the property market, affecting the majority – not just a ‘few.’

Why?

The reason this has occurred is down to our property cycle – or perhaps better-termed a ‘land cycle’ – which has been further accentuated by poor housing policy – restrictive planning conditions and generous tax incentives, which are ultimately destructive.

Rising prices, and the expectation of such are initially seen as a ‘good’ thing, because they drive the economy, increasing consumption (the ‘wealth’ effect,) stimulating economic growth, infrastructure investment, construction activity and demand for ‘durables.’

This in turn flows through to wages – which advantage the workers at the top of the income stream, rather than the labourers at the bottom. (See Andrew Leigh’s, The Story of Inequality in Australia (2013,) which points out, since the mid-1970s, earnings after inflation for the bottom tenth of the population has grown 15%, in comparison to 59% for the top tenth.)

The gains are subsequently capitalised into rising land values, as investors, buoyed on by inflationary expectations, easier lending conditions, and ‘fear of missing out,’ lead a bull market of speculative activity (such as we’re seeing in Sydney) – until reality eventually steps in, and the trend inevitably turns.

In other areas of the economy that suffer from inflation, some form of substitution can typically occur, however land – and the infrastructure that gives it its value – is fixed in supply, an absolute necessity to all business and personal needs, therefore as land values rise, there is an inevitable strain on productivity, affecting job growth, private debt, small business, and unemployment (such as we’re seeing in Australia presently.)

Whilst monetary policy and the interest rate ‘lever’ are employed to moderate the damaging effects of a property cycle – at every step of the process, real estate has been used as collateral for further economic investment, a revenue generating machine for government, and ‘wealth’ fund for retirement, therefore whilst the aim is to prevent a ‘hard’ landing, the motivation is always bent on protecting existing values, rather than letting them fall.

Hence why demand side subsidies are favoured as a ‘band-aid’ to affordability, rather than cure.

The result

Without direct political intervention to rectify the damage, the greater and more destabilising the divide becomes, not only placing pressure on the welfare system, but evidenced ‘vocally,’ as rising numbers enter the housing market later, pay far more over the lifetime of their loan, and risk reaching retirement still servicing household debt – as is the case in Australia.

This was noted back in 2012 in a CPA study entitled ‘Household Savings and Retirement – where has all my super gone?’ And most recently by executive chairman of ‘Yellow Brick Road,’ Mark Bouris, who ‘concerned’ about lump sum superannuation payments being used to pay off mortgages, made a submission to Joe Hockey’s parliamentary financial inquiry, suggesting we can ‘solve’ the above impacts, with additional tax breaks to allow people to pay down their housing debt faster.

Needless to say, it doesn’t take much of an economist to understand that subsidies – no matter attractive they may seem – are ultimately capitalised into prices, thereby raising the entry costs for first home ownership further, and increasing the pain for the next generation of aspiring buyers.

But then considering the line of business Mr Bouris represents, I suspect this is isn’t about ‘solving’ the crisis, so much as supporting it.

The self perpetuating cycle..

To some extent, it’s a self perpetuating cycle – after 30 years of mortgage repayments dedicated to paying off their principle place of residence, vendor’s obviously don’t want to see the price of their biggest asset drop.

Investors are similarly motivated, an AHURI study released in December 2013, identified the typical investor, as one who expects their property to ‘double every ten years’ as a strategy to finance retirement.

Incidentally, the same study also noted that three-quarters of the investors surveyed, do not see negative gearing as a reason to purchase – but merely as ‘an added bonus’ – thereby weighing against the myth of an ‘investor lead exodus’ should the policy be scrapped.

However a system that tries to both feed speculation, whist creating unaffordability through supply constraints, is ultimately set to fail, as low-income households are continually forced to the outskirts, whilst the higher income individuals get to purchase the front row seats.

Social polarisation…

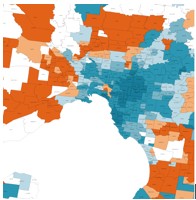

This results in social polarisation, which is clearly visible on the Melbourne map below, taken from the REIV, which illustrates the median house price by suburb, relative to the metro median.

The colours coded with the darkest blue indicate house prices more than double the metro median, and orange, house prices that are more than 25% below the metro median. (The white spaces are areas for which there is insufficient data.)

This aligns very closely to a map constructed using data from the ABS, which ranks geographic areas in terms of their relative socio-economic advantage and disadvantage, highlighting diversities such as incomes, education levels, occupations, rent and mortgage payments, family structure and unemployment.

Once again, the beetroot red and bright orange ‘fringe’ suburbs, sit well away from the affluent dark blue vicinities, which contain the top schools, medical facilities, shopping strips, high paying jobs, train and tram networks, childcare centres, social amenities, and so forth – all of which our tax payer dollars collectively fund – yet under the current structure, only the local home owners get to advantage.

This would include not just the various social benefits offered, but the additional on-flow of capital gains each property attracts from a squeeze of consistent market demand.

To emphasise, top performing government schools in Australia, do not reserve places for those showing merit, rather the families both willing and able to support the 20-50% premium, charged for accommodation in a desirable school’s catchment zone. ‘Fair go Australia.’

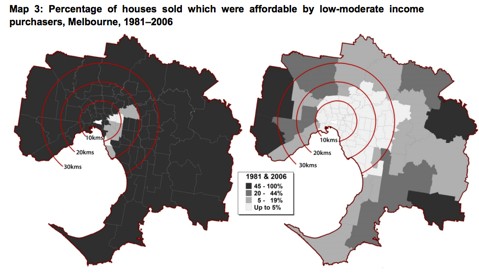

In case you need further convincing, you can chart how the trend has evolved using the image below, which is taken from a previous AUHRI investigation, showing how the percentage of affordable dwellings available for low to moderate-income purchasers, has changed in Melbourne, between the years of 1981 and 2006.

The darker areas are the ‘most’ affordable, whilst the white patches are the least.

What of the ‘price’ ripple effect?

Even heading 45km or so away from the CBD, low-income purchasers can only acquire affordable accommodation – in the range of $200,000 – $400,000 – if the lot size is much smaller than 600 square metres, which is still deemed ‘standard’ in many middle suburban regions of Melbourne.

Further more, any hope of ‘backyard cricket’ is unlikely, as the new developments are littered with homes that have a footprint, which extends to the boarders of each block.

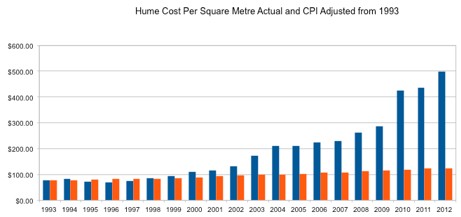

The graph below highlights why this is so – it was put together by a colleague, Steven Armstrong – using valuer general statistics, and it charts the extraordinary rise in land values per square metre in Hume City – an outer metropolitan growth zone in north-western Melbourne – between the years 1983 to 2012.

The remarkable escalation in prices had nothing to do with homeowners wanting the castle, when a modest suburban home would do. Rather the issues I outlined last week in regard to planning restrictions (false scarcity), tax and infrastructure overlays, land speculation (the underlying cause of ‘all’ bubbles), that are exasperated further by ineffective supply side policy.

It’s important to make this point, because whilst most people assume the ‘price/ripple’ effect works outwards – under the current system, the causation works both ways.

It’s the marginal price of land at the fringes of our capital cities, that sets the ‘base’ value for the better-located plots further in.

In other words – it’s not supply that ‘solves’ affordability for low-income purchasers, but the cost at which that supply can be delivered to the ‘homebuyer’ (not speculator) market.

Property Overvalued? A bubble? A concern?

In light of the information above, when I was recently asked to make comment on whether Australian real estate was overvalued or not, I sensed the intention was to take the traditional view, and instead of charting ‘why we’re here’ – assess whether job growth, population expansion, demand for credit, housing turnover, wage growth, interest rates, mid term supply and so forth, were supportive of a future sustained increase.

However, whilst the above data will give a mid-term indication over whether current process are ‘serviceable’ at existing rates, or if market turnover can maintain pace, it gives little indication as to the long-term effects I’ve highlighted above, which in my mind, present a far greater destabilizing force, as we bear witness to a slow generational shift, eating at the edges of home ownership in the months and years ahead.

I’ll leave the reader to come to their own predictions on market movements as we traverse through 2014. Albeit, in light of the Government’s response to previous housing ‘affordability’ inquiries, I think the above concerns will merely worsen rather than improve – and at some point, we’ll all feel the impact.