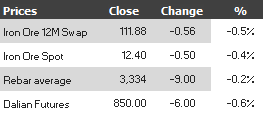

Fine below the iron ore price charts for February 21,2014:

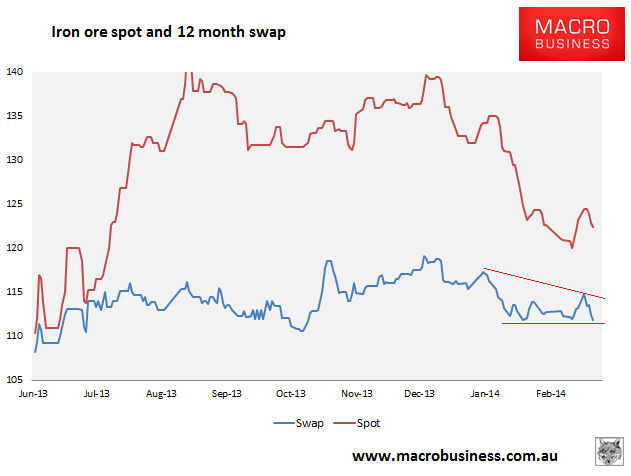

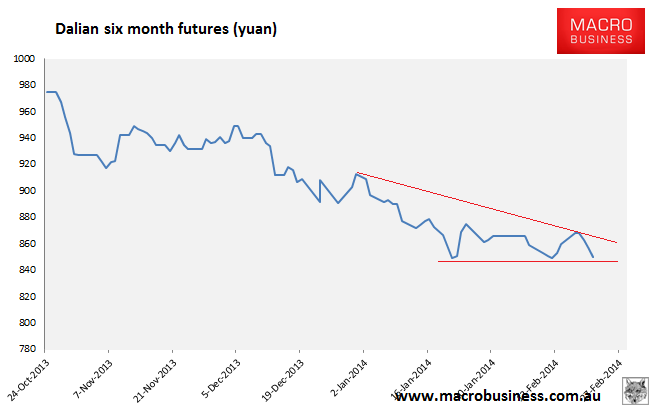

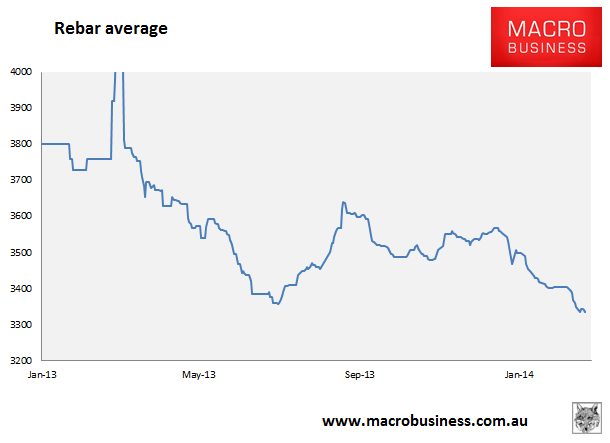

This is not a happy technical study. Iron ore is holding but rebar average has breached new lows. Both Dalian six month and 12 month swaps have hit marginal new lows as well, though a more useful observation is that both illustrate descending triangle patterns, suggesting more significant breakdowns loom. A deeper backwardation would make sense at this point given the seasonal strength but weakening fundamentals.

“I don’t think the steel market can recover anytime soon because the macroeconomic environment is not looking good,” said an iron ore trader in Tianjin.

“This is why mills are not storing so much iron ore because if they put too much money on raw material it will have a bad

impact on their cashflow.”“A number of domestic Chinese iron ore producers in Hebei and Shandong cut their prices for concentrate by around 25-30 yuan per tonne, while traders trimmed 5 yuan per tonne from their offer prices for imported grades held at port due to sluggish sales,” Steel Index said.

Traders say it also curbs any rush for steel mills to buy forward cargoes.

“There’s no urgency for them to book vessels or future cargoes because there’s a lot of available material at the ports,” the Tianjin-based trader said.

This may prove too bearish in the short term as the Q1 steel ramp up continues. It does appear mills returned to markets for more stock last week as iron ore bounced and there’s not enough downside in the spot price now to suggest a return to vigorous destocking.

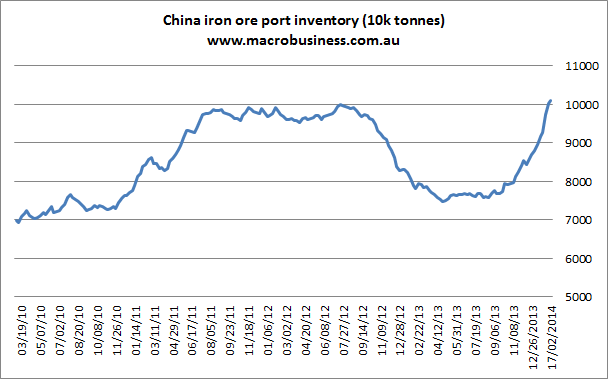

Port stocks kept climbing into new records last week but much more slowly adding 450k tonnes:

Also of note was a jump of the same magnitude in Indian sourced inventories to levels not seen for a year.

The odds still favour some short term stability followed by more destocking with a material risk that it comes sooner.