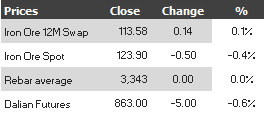

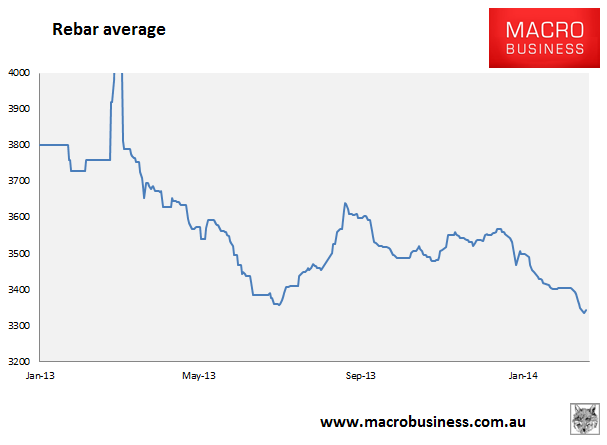

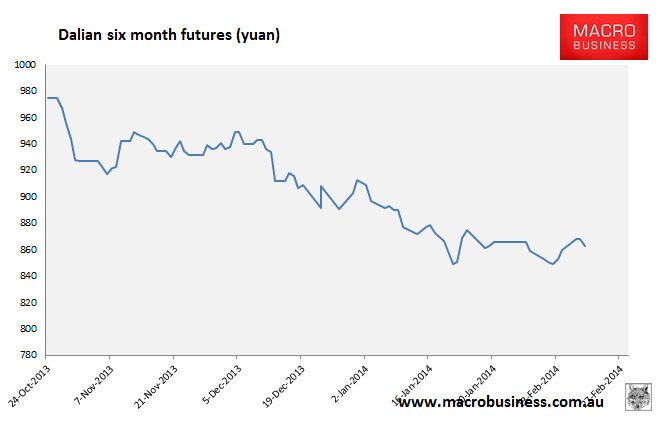

Charts for February 19, 2014 below:

In news the FMG bulls were out yesterday:

…That a serious bank of supply is about to hit the market cannot be contested. All three commercial corners of the Pilbara are racing to install new capacity. Everything running to plan; they will collectively add around 75mtpa to the system by the end of 2014 with both Rio and BHP looking to increase output further from there.

Power…says the market easily absorbed the new volumes the producers delivered last year as China’s steel industry stepped up output to a record 780mt.

…according to BHP the current run rate implies annual production in the mid-700s…But Power is buoyed by forecasts from the China Steel Industry Association that suggest steel output is on track to hit last year’s 2.1mt a day rate.

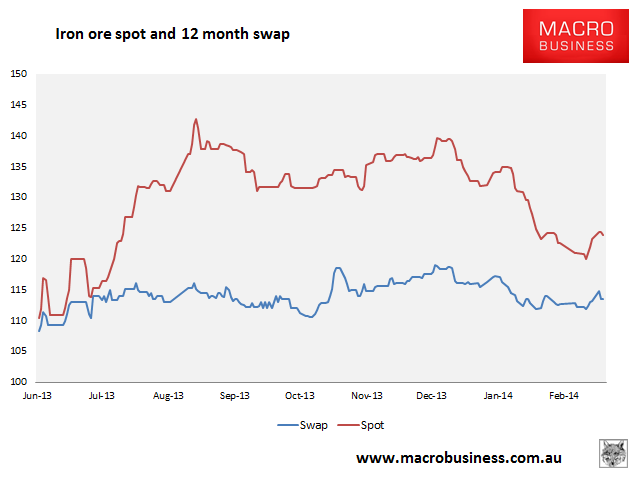

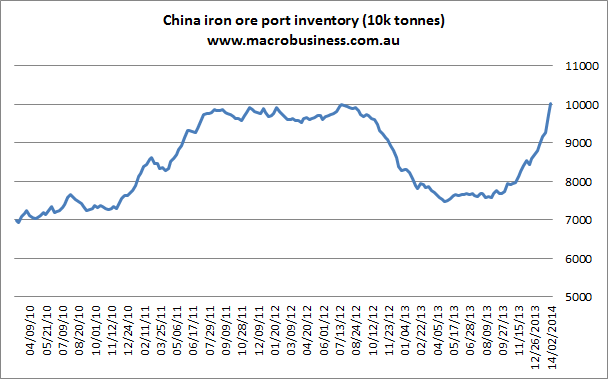

“Easily absorbed” is a bit of an overstatement. September quarter prices averaged around $140. Prices have trended lower since by some 12% during the strongest seasonal period of the year and despite a one-of-a-kind Chinese restock that began, you guessed it, right after the September quarter:

I reckon Chinese steel production has every chance of falling this year as excess production is slowly rationalised. Even Mr Power seems to acknowledge that a repeat of last year’s steel run rate would be superb!