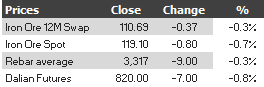

Find below the iron ore charts for February 25, 2013:

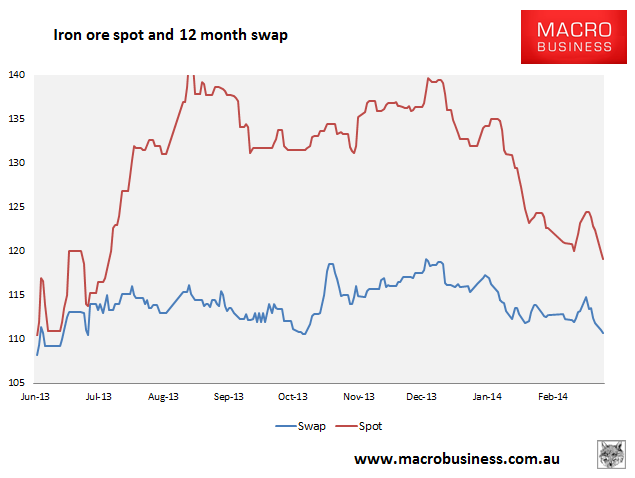

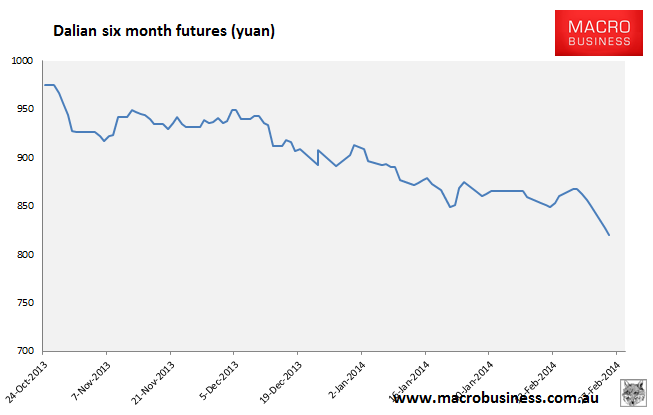

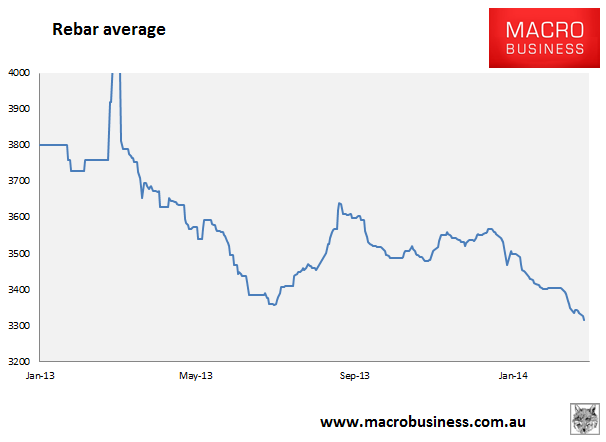

Less panic today but all red nonetheless. Iron ore spot has more decisively broken support at $120 and 12 month swaps are sitting right on the October 2013 low. Free falling rebar futures fell further to 3307 and are now in backwardation suggesting more weakness to come.

Reuters has two stories with more texture. The first looks at ore:

Weaker steel prices, lending curbs, plentiful supply of iron ore in the spot market and huge stockpiles at home have combined to drag down prices, said an iron ore trader in China’s eastern Shandong province who sees the price falling further to either $115 or $110.

“Before, when we offer cargoes at 800 yuan per tonne, buyers ask for a discount of 10-15 yuan. Now that’s become 30-40 yuan,” he said, adding his company has held onto 300,000 tonnes in inventory for two months now amid a scarcity of good offers from buyers.

“It’s a tragedy for traders like us.”

Yes, and ours as well. If this chap and his ilk (or their bankers) panic, it will open the trap door on iron ore prices as they dump inventory.

Reuters also offered a glimpse of how weak steel is:

Li Xinchuang, Executive Vice Secretary-General of the China Iron & Steel Association (CISA), said overcapacity in the sector was “probably beyond our imagination” and added that the sector was facing an extremely complicated situation as a result of slowing growth, structural adjustments in the economy and policies to close old capacity.

However, demand was still rising steadily, which, combined with the desire to gainmarket

share, has prompted mills to continue adding capacity.

China has around 300 million tonnes of surplus steel output capacity, equivalent to nearly twice the output of the European Union last year. Still, mills have continued to expand, adding new capacity of 69.2 million tonnes in 2013, according to a report by consultancy CUsteel earlier in February.

This gives an idea of how easy it will be for rationalised capacity to be filled by the remaining mills. But the problem remains the same. The consolidation is being driven by tighter credit which also hits wider growth and ensures that all steel production remains under pressure. Second, as this oil tanker slowly turns the virtuous cycle of steel will reverse. As demand grew, the need for greater refining capacity added to demand for yet more steel. As wider demand flattens or falls, stalled and falling capacity removes even more steel demand.

Do not underestimate the possibility of falling Chinese steel production this year.