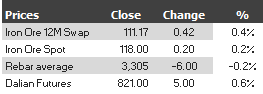

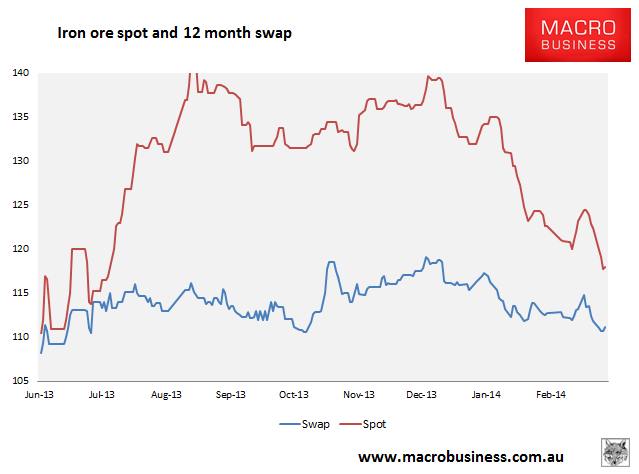

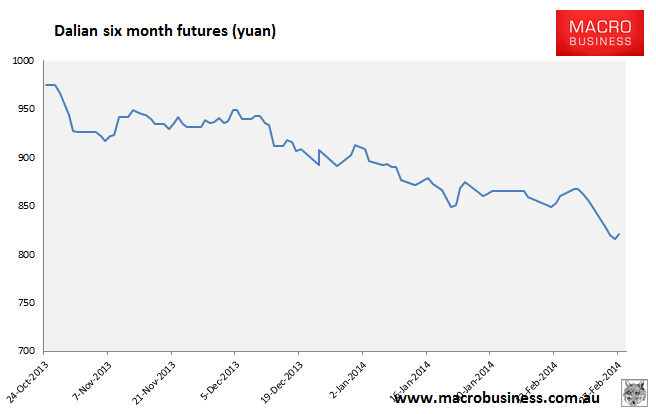

Find below the iron ore charts for February 27, 2014:

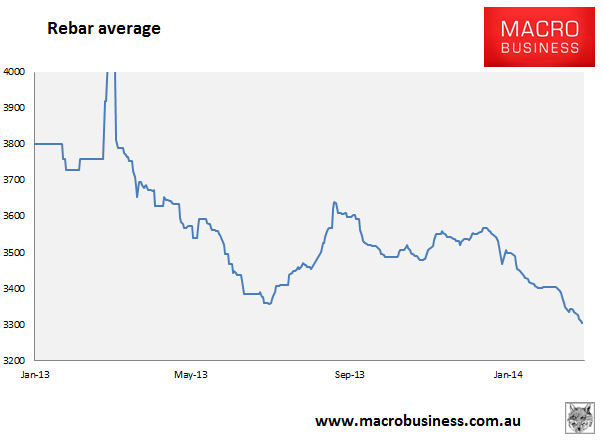

To my mind this is a dead cat bounce until rebar stops falling. Futures bounced yesterday and are back in contango but I’m not convinced. Reuters has more:

“Some mills in southern China are trying to sell part of their cargoes under long-term contracts that have yet to be delivered because they have more than enough at the moment,” said an iron ore trader in Shanghai.

Tighter liquidity and slow steel demand tend to force some Chinese mills to sell iron ore cargoes back into the market, aiming to turn stockpiles into cash before spot prices drop further.

…”I think the market’s still in a bearish situation and I personally feel that the price has a chance to touch $100 or a bit lower than that,” said the trader.

Meanwhile, Dow Jones has a story that throws light on what’s keeping iron ore equities levititating:

Fortescue built up massive debts during a decade-long campaign to break the dominance of rivals such as Rio Tinto, BHP Billiton and Vale SA in supplying China with iron ore. At its peak, Fortescue owed more than $US12 billion.

The miner began paying off its debt last year, but still had $US8.6 billion in debt after subtracting cash on its balance sheet at the end of December.Chief Financial Officer Stephen Pearce said Fortescue wanted to pay back “another couple of billion” dollars by year-end, but acknowledged the pace at which the miner would be able to repay its debts would depend heavily on the strength of iron ore prices.

Australian broker Morgans forecasts Fortescue could reduce its debt-to-equity ratio to 41 per cent by December versus an estimated 57 per cent a year earlier if prices hold around $US124 a tonne over 2014. At an average of $US100 a tonne, the miner would only be able to cut its gearing to 53 per cent by December, it estimates.

Perth-based Morgans analyst James Wilson attributed recent price falls largely to seasonal changes in demand…Still, if prices do start to fall below $US110 a tonne “then that’s when you’ll probably see people starting to re-evaluate their expectations,” he said.

Seasonal demand should be strong not weak, sheesh, but he’s right about the effect of falling prices.