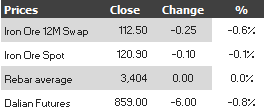

Here are the iron ore price charts for February 7, 2014:

First things first, from the BOM:

A well-structured tropical low (09U) lies over the Kimberley, about 95 kilometres east of derby at 11am Sunday and moving towards the west southwest at 14 kilometres per hour. This system is forecast to track close to the west Kimberley coast and Eighty Mile Beach area during Monday. There is potential for this system to move off the west Kimberley coast and if it spends sufficient time over open water, will develop into a tropical cyclone. Tropical Cyclone Advices are current for this system, please refer to the latest advice for further details.

Flood Advices are current for the Kimberley and Pilbara. Please refer to the latest advices for further details

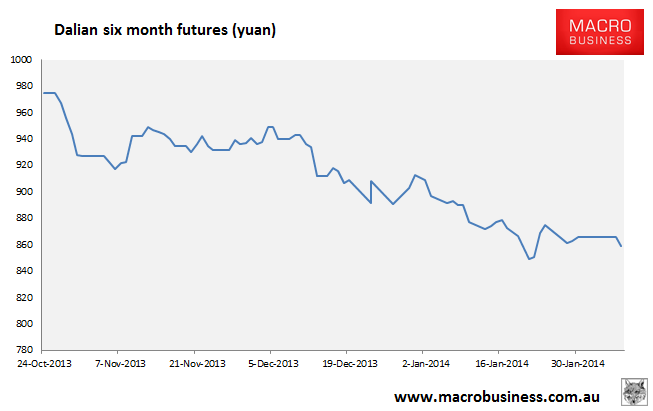

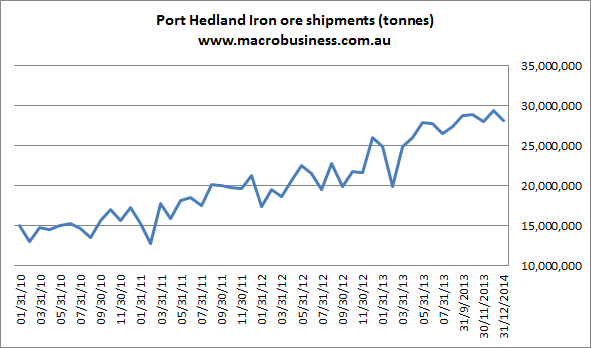

That’s tracking directly for Port Hedland and iron ore central so we might see some short term price support on potential supply disruptions. Still on the port, its January shipping figures are out and showed continued strength with 28.3 million tonnes hitting the high seas in the month:

That was down a little from December with Chinese shipments dropping 3% but still up 27% year on year. This makes the current weakness in spot pricing all the more noteworthy as a supply side issue.

On the current market Reuters has some good texture:

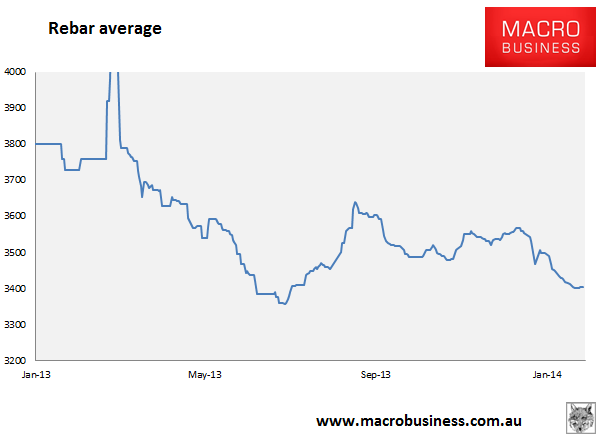

The most-traded rebar for May delivery on the Shanghai Futures Exchange touched a session low of 3,401 yuan ($560) a tonne, its weakest since the bourse launched rebar futures in March 2009. It closed down 1 percent at 3,411 yuan.

“There’s no positive sign for the market and we may see prices falling further,” said Zhou Ting, analyst at Jinrui Futures in Shenzhen, who sees support for rebar at 3,300 yuan.

…”We may only see a pickup in consumption when construction activity resumes in March,” said Ting.

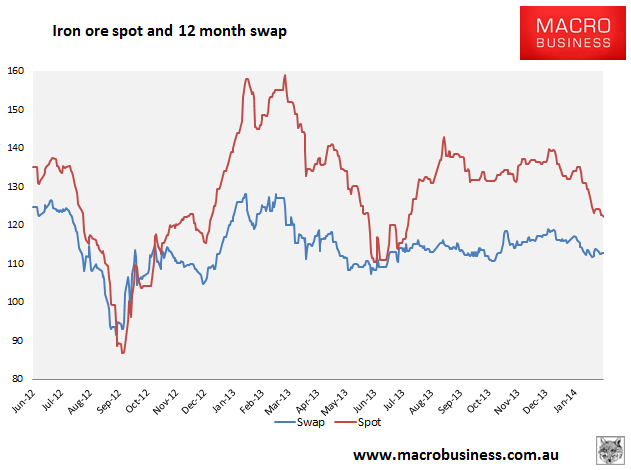

The weakness in the steel market is likely to put more pressure on iron ore prices.

…With the holiday over, traders expect Chinese mills to return to the market.

“I think restocking will happen but how strong it will be is a question mark,” said a physical iron ore trader in Shanghai.

“Since prices are falling, if I were a mill I would only buy the minimum of what I need for now. Maybe more mills will be

willing to buy when the price drops below $120.”

The rebar average price is still tracking slightly better but futures are threatening new lows.

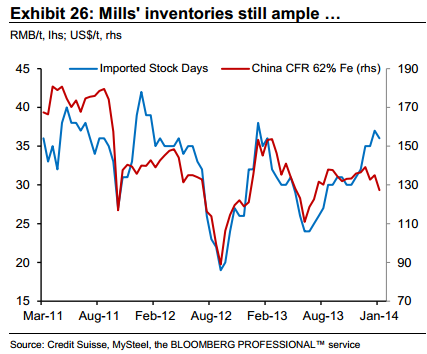

Whether Chinese mills continue to build inventories at this point is the billion dollar question. I can’t see why they’d do it for long if at all. Steel prices are at deeply loss-making levels. The economy is slowing as tight credit and an emptying infrastructure pipeline take their toll and the Chinese supply chain is already brimming with steel and iron ore. Mill ore inventories are high (from before the Lunar break):

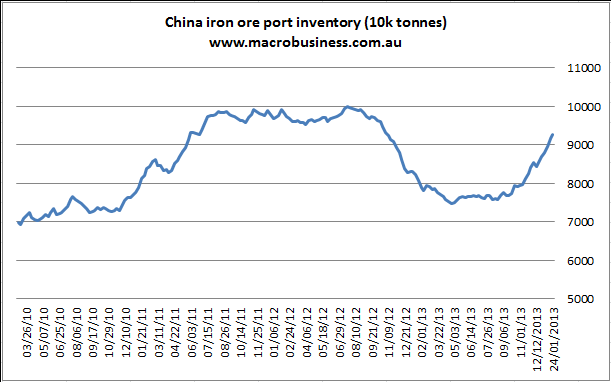

Port stocks are high. This chart is not updated post holidays yet:

At this point an iron ore destock looks a much more likely prospect though we might stumble through Q1 on weather disruptions first.

The last three inventory destocks, in 2011, 2012, and 2013, have each caused the iron ore price to fall the better part of $50. Each was in circumstances of broadly tighter supply than today and the balance is going to loosen by another 40 million tonnes or so after March. Using a starting point of $120, a full blown destock in the next few months gives you a price in the mid 70s.

It may not happen but the current combination of factors at work in the Chinese steel market are precisely those that have triggered big iron ore destock cycles in the past.