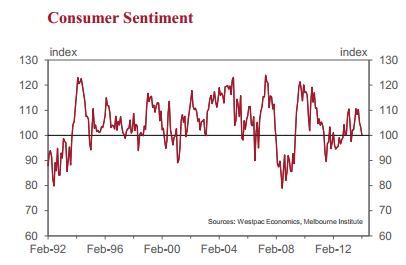

The Westpac Melbourne Institute Index of Consumer Sentiment fell by 3.0% in February from 103.3 in January to 100.2 in February.

This is a surprisingly weak result. The Index is now down 7.5% on a year ago; 9.5% on its recent September high and is at its lowest

level since July last year.

The theme from this survey appears to be that households are particularly worried about the future. The difference between the current conditions index and the expectations index widened further and is now at its highest level since June 2000. Specifically, the component of the Index measuring consumers’ expectations for the economy over the next 12 months is at its lowest level since March 2012 and the less volatile component tracking consumers’ expectations over the next 5 years is at its weakest since February 2009.

We will get a better guide to what is behind this loss of confidence in the economic outlook with the March survey which includes additional questions on news recall and news perceptions. We suspect the run of ‘bad news’ around the motor vehicle industry, other manufacturers and Qantas may have rattled consumers. There may also be heightened concerns about what lies ahead with the May Budget.

Households are clearly more worried about interest rates as well. In this survey 57% of respondents expect interest rates to rise over the next 12 months, with 18% expecting increases of more than 1ppt. That contrasts with only 6% who expect some mortgage relief. When we last surveyed this issue in August last year only 39% expected rates to rise.

Exuberance around house prices is starting to wane. The Westpac-Melbourne Institute House Price Expectations Index fell by 2.2%. The Index is now 4.3% below its peak in December but is still 26.2% above its level at the start of last year. Attitudes towards house purchase stabilised in February although the ‘time to buy a dwelling’ Index is 10.8% below its September peak.

Households continue to be very concerned about the labour market. The Westpac-Melbourne Institute Index of Unemployment Expectations rose by 2.3%. The Index is now 9.2% above its level in September last year and 7.5% above its level a year ago. Higher reads indicate more consumers expect unemployment to rise in the year ahead. The Index is at its second highest point since July 2009 – the weakness in the labour market, particularly over the last 6 months has been taking its toll on households’ confidence.

As discussed we saw solid falls in the two components of the Index that measure households’ economic outlook. The subindexes tracking expectations for “economic conditions over the next 12 months” fell by 7.1%; and “economic conditions over the next 5 years” fell by 4.6%. 12 February 2014

Attitudes towards finances varied: the sub-indexes tracking views on “family finances compared to a year ago “fell by 4.1% while “family finances over the next 12 months” lifted by 1.7%. The subindex on “time to buy major household items” fell by 1.9%.

The ‘economic outlook’ components are now down by 17.9% and 14.5% respectively over the last year. The ‘finance’ and ‘time to buy a dwelling components have been more stable’, with declines in the 2 to 5% range.

Conclusion

Households seem to be sending a fairly clear message in this survey. It is around questioning why fiscal policy is about to be tightened and interest rates lifted when the labour market is so weak and housing affordability is being squeezed.

The key dynamic which we have been anticipating for the Australian economy has been a marked feedback on consumer confidence and spending from ongoing labour market weakness.

The evidence around those themes has been clearly highlighted in this survey. However we have been surprised by the recent solid boost to business conditions and business employment plans. If these signals manifest in solid improvements in the labour market boosting consumer confidence and incomes then there will be no need for lower rates.

The Reserve Bank has indicated that rates will be on hold for some time and, in the February Statement on Monetary Policy noted that markets expected steady rates prior to a hike in about a year. Our “out of market” view that rates can fall later this year will continue to be tested by the data.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.