Fairfax’s Max Mason has written a piece today in The SMH arguing that the Reserve Bank of New Zealand’s (RBNZ) speed limits on high loan-to-value ratio (LVR) mortgage lending, implemented on 1 October 2013, are failing to cool New Zealand house prices:

Tighter lending restrictions imposed by New Zealand’s central bank may be strengthening bank balance sheets there but have yet to put a cap on booming Kiwi house prices.

The median New Zealand house price has increased by $NZ27,000 ($25,500) since the Reserve Bank of New Zealand placed loan-to-valuation ratio (LVR) restrictions on mortgage lenders last October.

Regulators both in Australia and around the world have been closely watching the impact on the New Zealand housing market of the new lending restriction rules…

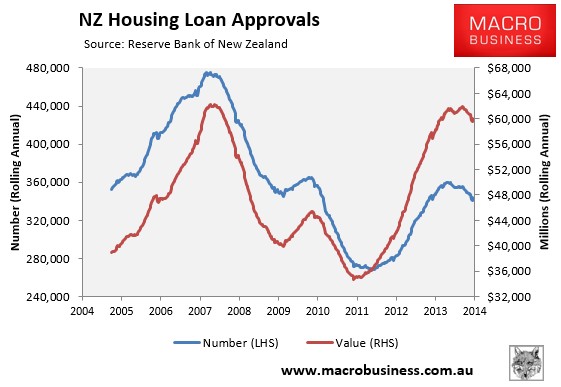

Despite fewer houses being sold, the number and total value of loan approvals increased since the LVR restrictions were put in place. As expected, the value of new loans with an LVR above 80 per cent fell dramatically.

Reserve Bank of New Zealand data shows that the number of loan approvals increased 31 per cent until they peaked in December, before tapering off over Christmas and New Year.

While I am sure that it is not deliberate, there are a number of errors in Mason’s analysis.

First, he has quoted changes in the REINZ simple median house price index in order to come to the conclusion that Kiwi house prices are still rising strongly. However, this is the incorrect series to use for this type of analysis, since it does not adjust for changes in the composition of homes sold. As noted buy Westpac chief NZ economist, Dominick Stephens, house sales in lower price brackets have fallen materially, increasing the proportion of higher valued homes sold and inflating the median price:

…the Real Estate Institute reported that nationwide sales of houses under $400,000 are down 14% compared to a year ago, whereas total sales are down just 1%.

Ironically, the dearth of sales in cheap categories means that the median price of those houses that did sell is higher – up 7% in three months.

We have seen some rather specious reporting casting this jump in median price as good news for property owners!

The better index to use when assessing New Zealand house price growth is the REINZ’s stratified median, which adjusts for compositional change. As summarised yesterday, by this measure New Zealand house prices fell by 1.0% in December and are up 1.8% since September.

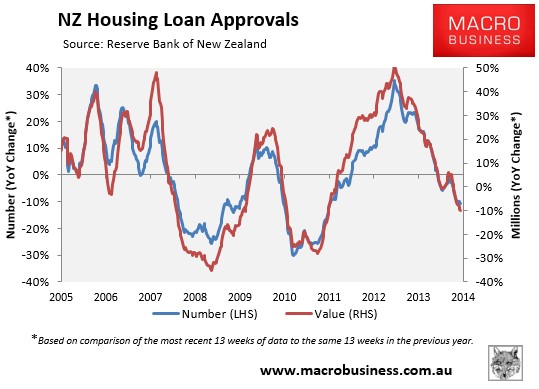

Neither is it correct to assert that the number of finance commitments have increased since the LVR caps were introduced – they haven’t. Looking at year-on-year growth, which overcomes issued around seasonality, shows that finance commitments are trending down after implementation of the LVR speed limits (see below charts).

In any event, the fall in New Zealand house sales is further evidence that the RBNZ’s mortgage caps are working, since any slowdown in the housing market could be expected to hit sales volumes first before prices. According to Westpac’s Dominick Stephens:

There is now no doubt about it.

New Zealand’s housing market is slowing.

The number of house sales per month fell 11% over the three months to December, in seasonally adjusted terms – the sharpest decline in house sales since 2009.

Lower turnover is one classic indicator of a market slowdown…

House prices tend to follow sales with a lag of a few months, so we expect house price inflation to begin cooling a month or two from now.

The bottom line is that the RBNZ’s mortgage caps are working to cool the housing market.

That said, macroprudential policy is a cyclical demand management tool only, and it is no substitute for addressing the structural barriers precluding affordable homes from being supplied in New Zealand, including artificial restrictions on land supply (such as urban growth boundaries and restrictive planning practices), as well as inadequate financing and provision of infrastructure. Changes to New Zealand’s tax system to limit negative gearing and implementing a capital gains tax on second homes would also likely be more effective in moderating credit/housing demand without adversely impacting first home buyers.