A couple of new notes from Citibank and Macquarie looking at 2014 equity strategy make good reading for the year ahead. Citi nicely summarises the prospects for the ASX this year:

More wary — Compared to the increased optimism that has met the new year, as the world outlook has brightened, we find ourselves a little more cautious on the Australian equity market. Two years of large increases have brought it back to a more normal valuation, and we’re mindful of being realistic about its potential.

Nonetheless, earnings growth looks more promising, particularly for the important resources sector, and we still end up anticipating the most likely outcome being another solid gain for the ASX200 in 2014, with an end year forecast of 5850.

Greater uncertainty — Around our general expectation, we also see more scope for variance than in recent years. One large uncertainty is the pace at which US monetary policy changes direction, with markets always vulnerable at this juncture in the cycle. Another uncertainty concerns the degree to which Australian GDP growth shows signs of picking up or not over the next 12-18 months, which we are relatively optimistic about, but where there could be frustration.

Fewer opportunities — A further consequence of the past two years of market recovery is that stock valuations have also converged, leaving less potential than when large divergences existed. The one major area with still modest valuations and potentially lessening earnings risk seems to be the resources sector, which we continue to favour. The more cyclical industrial stocks no longer have as compelling valuations, but have the potential to become expensive as their earnings recover, and we also continue to prefer them over the more defensive sectors and banks.

That seems to me a fair summary. But there is definitely some devil in the detail:

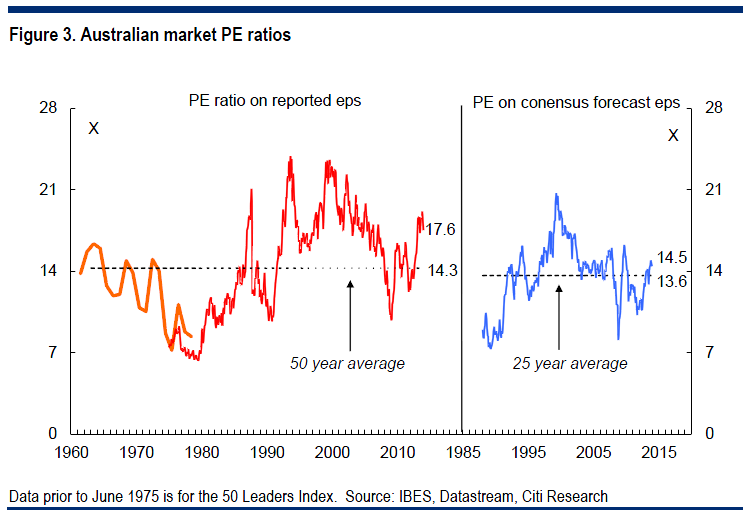

The market PE on forward consensus earnings, back at 14½x, is right on its two decade average under low inflation, and more fully pricing forecast earnings growth than at the start of recent years (figures 3 and 4). However, not being at an extreme, it could still move higher (or lower again) in certain circumstances, and need not necessarily limit performance. But we don’t really see those circumstances as most likely, and feel the market should stay in the vicinity of its current multiple.

Advertisement

In short, stocks are pricing a cyclical earnings recovery, though not as aggressively as some past cycles. Citi goes on to say that further re-rating is unlikely:

Investor interest in Australian equities also looks like it might remain “mixed”, with potential further AUD depreciation likely to keep foreign interest limited for the time being; and greater retail investor interest looking unlikely to be sufficient to make up for this. One risk, which our US strategist Tobias Levkovich points out, is the potential for the “Great Rotation” globally out of bonds into equities to drive further re-rating, but he tends to discount this.

That seems right to me as well. So, growth will need to be about earnings. On that front, Citi sees resources leading the way:

Advertisement

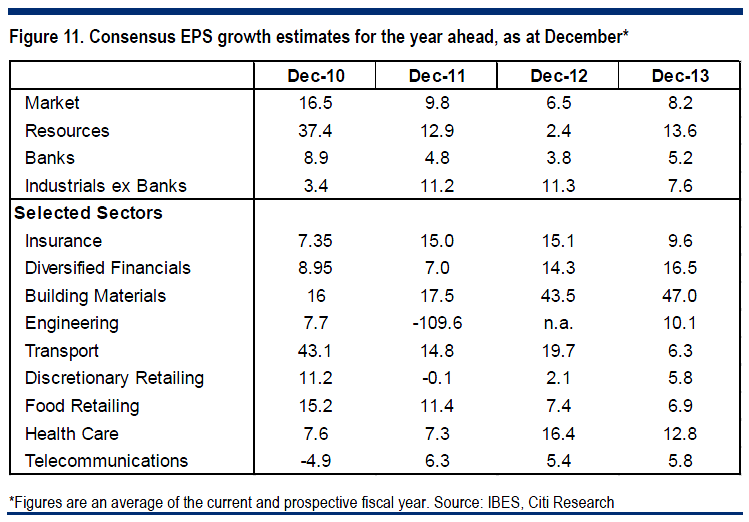

With market valuation fairly full, performance will be more contingent on earnings growth, but prospects there look more promising (figure 11). Unlike recent years, resource sector earnings are expected to increase substantially, and less because of commodity prices (though helped by a lower AUD) than by what’s happening at the companies, in terms of production growth and cost savings. So long as commodity prices don’t tumble again, strong earnings growth looks in store, and the improving outlook for the US and other economies provide encouragement, while China’s more expressed desire to maintain growth above a minimum rate lessens the unease as credit slows.

For the rest of the market, the “industrials”, growth is only expected to average around a trend rate in the next two years, 6-7%, similar to that already recorded in FY13. And in the near term, more earnings growth is expected to continue to come from the financial sectors (diversified financials, insurance, banks), than the nonfinancial sectors which are more exposed to the subdued spending in the economy, and growth is also expected to be weaker this year and strengthen next year. So the forecasts seem to account for the near term risks, and still moderate growth looks possible.

I have one problem with this analysis and it is this: consensus forward estimates for resources earnings have been missing badly. At the end of 2011 consensus estimates for 2012 were 12.9% growth but the end result was -2%. At the end of 2012, consensus estimates for 2013 were 2.4% growth and they ended at -22%. Now “analysts” are again catching the falling knife expecting 13.6% earnings for the year ahead.

Don’t get me wrong, the cost-out deflation story is real. Volumes growth is real. But an end to price falls is not. The only commodity that matters for the majors is iron ore and Citi’s assessment of why it won’t fall much is very thin indeed:

Advertisement

In China, the tightening in financial conditions seems to be slowing investment and industrial output, but stronger exports should provide some offset, and the government’s desire to maintain growth above a minimum rate, 7.5% in the past year, should also limit the slowdown.

In other words they’ll stimulate. Maybe they will but its one wild leap of faith with a tiny group of opaque Chinese communists who are saying in public that will be doing precisely the opposite.

In sum, Citi gets the outline of things pretty much right but its conclusion misses for me.

Advertisement

This is where we can turn to Macquarie, who has similar thoughts to Citi:

The period of strong equity returns driven by the cycle of valuation change, however, gives way to returns being driven by rising earnings momentum (refer to Figs 14 & 15). We believe this cycle will be no different. Hence in CY14 while we expect equity market returns will remain positive, returns can only match those of CY13 if earnings momentum rises strongly. Herein lies the challenge. The nature of the “LGC” is one of a weaker recovery, much weaker than normal, given the absence of any significant re-gearing of balance sheets across developed economies. Hence the demand upswing will be modest at best. Thus the challenge for equities in CY14 will be delivery of growth.

So where is the highest growth likely in CY14? Strong earnings leverage to lower A$ and/or rising or strong “top line”

…As the A$ continues to move back to a value that is more realigned towards “fair value” CY2014 is in our view likely to see a lift in EPSg is likely to all stocks leveraged to the lower A$ and also the modest improvement in demand in the developed world. This particularly would benefit the large diversified miners. The nuances of this cycle, in our view however, do suggest that small resources companies have the same risk/reward attractiveness as their larger peers because this cycle favours iron ore stocks particularly given the dynamic of the iron ore price outlook, cost reductions and growth.

In our view, many investors perhaps do not fully appreciate the degree of positive earnings leverage for the major mining stocks that will result from the convergence of the factors that are atypical for this point in the cycle from an Australian perspective and that will positively impact EPSg in CY14.

Again, nicely framed but Mac draws the same high risk conclusion, at least based more upon the currency:

Advertisement

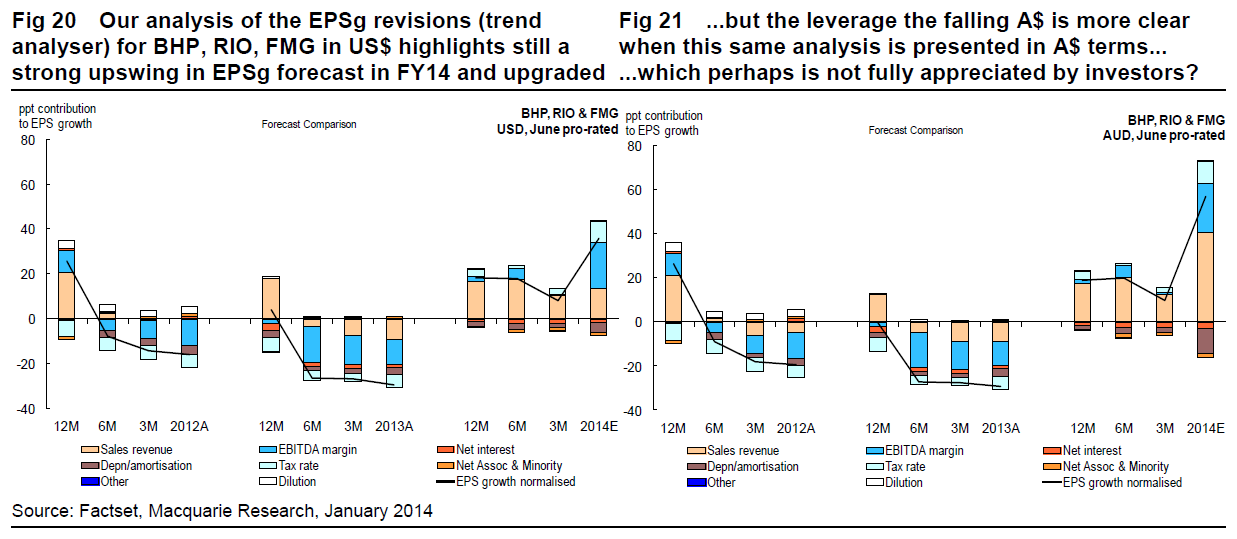

The leverage to the A$ for the major mining stocks is highlighted in the analysis presented in Figs 20 & 21 above. The analysis presents the progressions of this stock group’s EPSg forecasts FY12, FY13 and the progress of the current FY14 (June pro-rated) from both a US$ base which for each of these stocks is their reporting currency, versus translating this back to an A$ base. As can been seen the “underlying” FY14 USD forecasts as they have progressed show the clear upgrades over the last three months to EPSg ~+40%, driven by revenues, EBITDA margins and a lower rate of tax (predominantly BHP).

This same analysis when presented in AUD highlights an even strong rate of upgrades although the underlying drivers of the FY14 EPSg forecast in excess of +60% are similar although the revenue contribution to growth is unsurprisingly higher in A$ terms than US$ terms.

The critical point of this analysis of FY14 EPSg forecasts in both “underlying currency” and A$ highlights that the fall in the A$ will have a significant positive impact on underlying EPSg, and translating earnings back to an A$ base only magnifies this strong EPS uplift.

Impressive, certainly, but still based upon one assumption: China will stimulate. For me this is a risk that is not worth taking for two reasons.

First, if it doesn’t happen then regardless of the dollar, earnings are going to fall hard with an iron ore price ranging below $100. It’s an all or nothing bet.

Advertisement

Second, the same Australian dollar dynamic is at play in another group of stocks, what Macquarie calls:

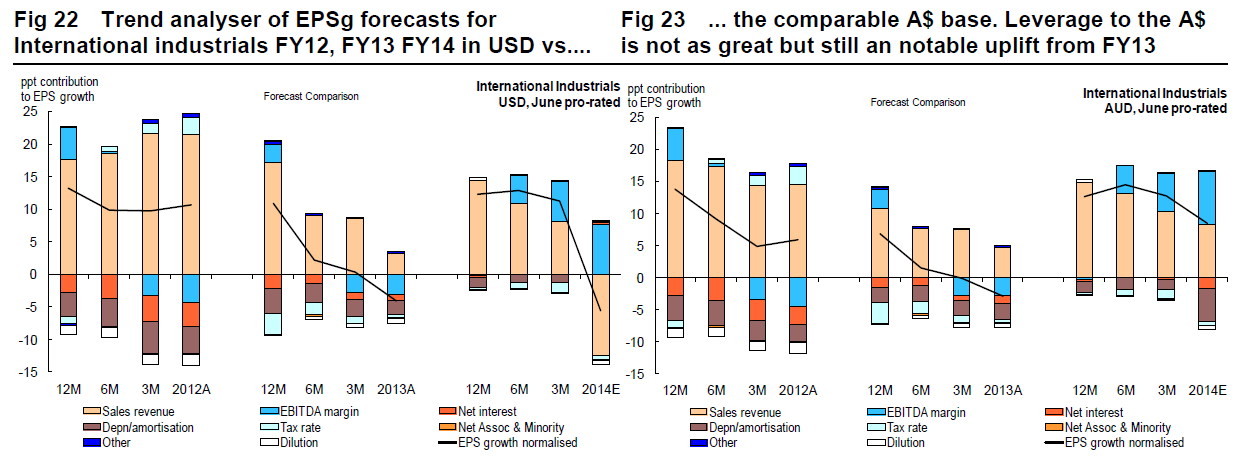

…“international” industrials highlights some degree of EPSg uplift in FY14 when EPSg is translated from US$ to A$. As many of these stocks will, however, also be translating some still sizeable profits from Australian operations at a lower A$ this would weigh on reported EPS if in US$. Only when these EPS are translated back to A$ is the FY14 EPSg uplift for this group of stocks both positive (+8.5%) but also a notable for the degree of upswing from the EPSg delivered in FY13.

I’ve been pushing this allocation for two years now and it’s still rolling nicely. Mac Bank’s basket of international industrials includes: ALL, ALQ, AMC, ANN, ASB, BKN, BLY, BRG, BXB, CPU, CWN, FLT, FOX, HGG, IPL, JHX, LLC, MIN, MND, MRM, NUF, NVT, ORI, RDF, SGT, SRX, SVW, TSE, TWE & UGL.

Advertisement

The upshot for 2014 is that ASX performance will be very dependent upon China, which may be a little surprising given the economic focus on rebalancing, but there is no reason to take that black and white bet.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.