Investment bank, JP Morgan, has released an interesting research note today arguing that there is only limited upside to Australian non-mining investment, which is likely to be capped by low levels of confidence, still tight credit conditions, low capacity utilisation, and the falling Australian Dollar.

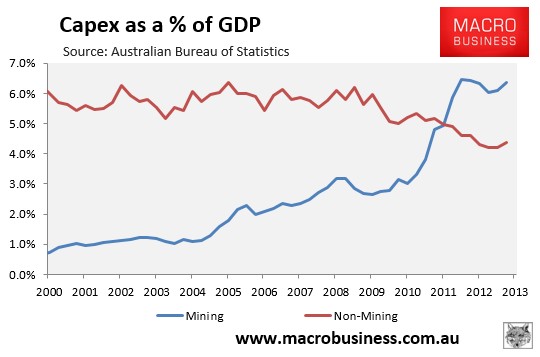

In its report, JP Morgan asks whether Australia’s non-mining economy is in the position offset the expected fall in mining capital expenditures, which roughly tripled as a share of GDP from 2009 to all-time highs.

JP Morgan forecasts only a modest pick-up in investment outside mining, with the environment remaining difficult. Of particular concern is that capacity utilisation remains below average, which means that “firms can ramp up output using existing plant and equipment”. When combined with low levels of confidence, brought about by weak demand and tight credit conditions, there is little incentive to invest. Further, the falling Australian dollar “means the price of many imported capital goods is rising; 15% of Australia’s capital formation is imported”.

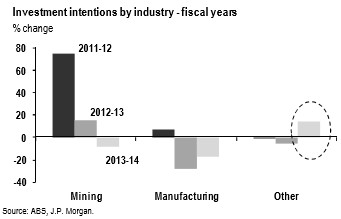

The most recent ABS capital intentions survey also showed that spending in the year ended June 2014 in mining and manufacturing will have fallen below the prior year’s level (see next chart), with manufacturing faring especially poorly facing “high and rising costs, a lack of critical mass (particularly in the auto industry)”.

This leaves the non-manufacturing sector to fill the mining void. And while “firms in transport, retailing, healthcare, finance,and tourism, for example, intend to lift spending 14% in the current fiscal year, after several years of little or no growth”, the uplift is unlikely to be anywhere near big enough to offset falling mining investment.

JP Morgan therefore concludes that “the absence of additional supports to GDP growth explains why we expect another year of sub-trend growth in Australia, a further rise in joblessness, benign inflation, sluggish growth in incomes, and perhaps another RBA rate cut”.

Obviously, I concur with JP Morgan’s assessment. The fact remains that mining investment in Australia is roughly 50% bigger than non-mining investment, meaning that for every 10% fall in mining capex, non-mining capex would need to rise by around 15% just to keep overall investment constant (see next chart). This is a highly improbable outcome, particularly in light of manufacturing’s ongoing struggles.