Barclays has joined the increasingly loud roaring of the China bears. Via FTAlphaville comes a three clawed slash at the dragon’s throat:

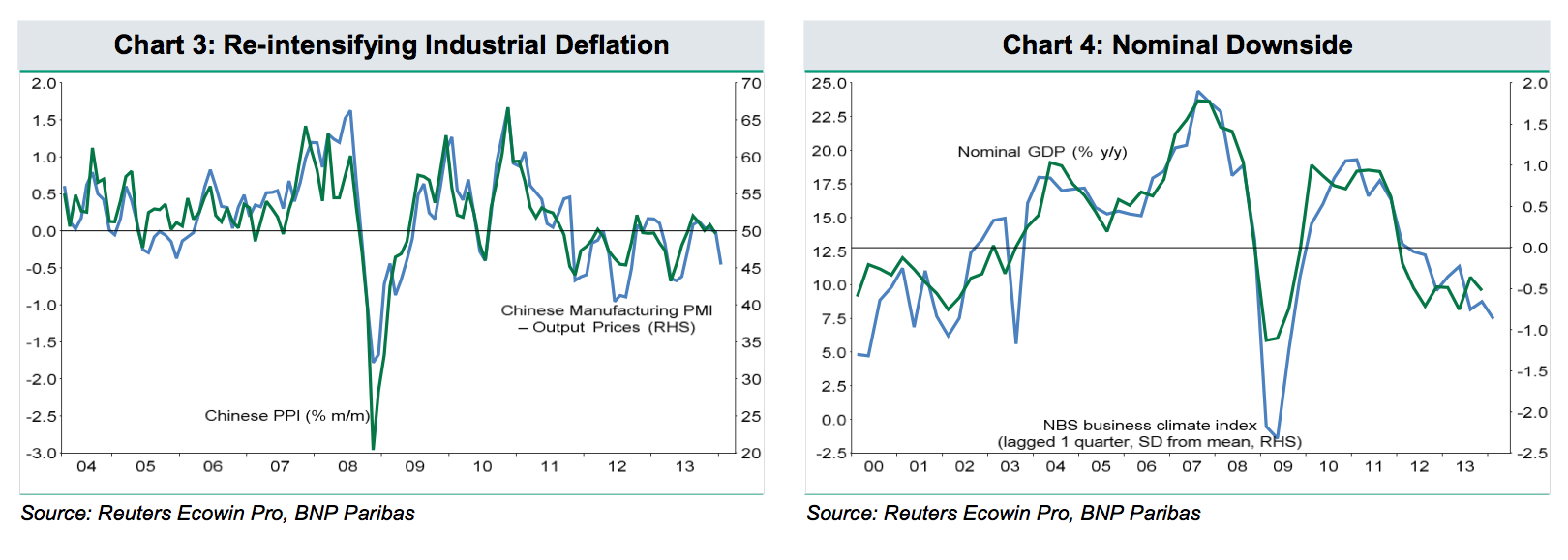

In terms of the first, the pace of China’s build-up of leverage since the global financial crisis is clearly unsustainable.Estimates of economy-wide leverage vary and can be calculated in different ways. Our preferred variant however is what can be labelled ‘total credit market debt’, which includes not just the orthodox gauge of non-financial credit but also the unconsolidated liabilities of the financial sector i.e. interbank liabilities. While the latter in principle should ‘net out’, the historical record is that they frequently do not when credit risk crystallises. Moreover, there is strong evidence that Chinese banks have used financial engineering to disguise risky corporate lending as inter-bank activity in order to circumvent regulatory requirements.

After being relatively stable in the 3-4 years before the global financial crisis at around 150% of GDP, total credit market debt has soared to over 250% by 2013Q3; a rise of just 100% of GDP in a little less than five years (Chart 1). Not all credit booms turn into busts with an attendant banking crisis. But credit booms are a necessary condition for banking crises however…

As Rudi Dornbusch used to remark, it takes two nominal variables to make a real variable so China’s debt dynamics in the coming years and the speed at which ‘real debt’ continues to rise will necessarily also be conditioned by prospects for nominal GDP growth. A second misleading and persistent canard is that the Chinese economy will effortlessly be able to sustain relatively rapid top-line growth despite accumulating evidence to the contrary. Nominal GDP growth has slowed sharply in recent years as diminishing returns to China’s investment-led growth model have increasingly set in.

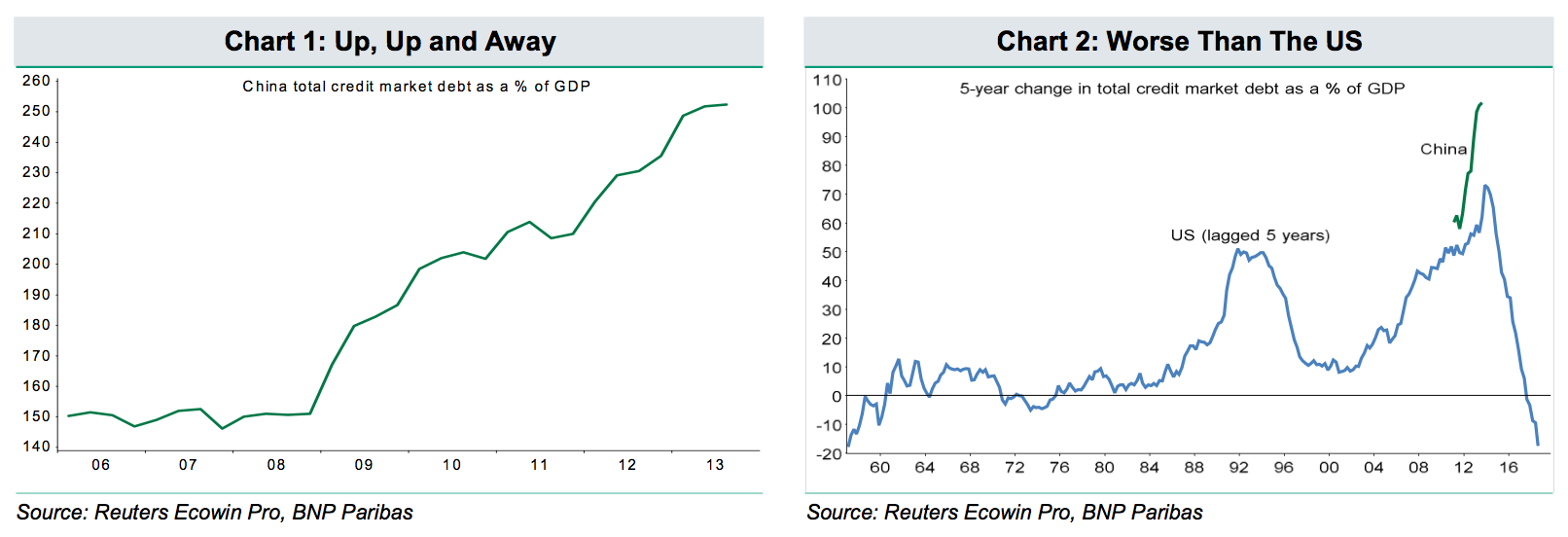

Accelerating malinvestment in frequently unfinished real estate developments and white elephant infrastructure projects has seen the credit efficiency of growth plunge while serial overcapacity in basic industries has led to engrained industrial deflation. PPI inflation has now been negative for 22 months with the latest survey evidence suggesting that deflationary pressure is again re-intensifying (Chart 3). The net result is that China’s nominal GDP growth has struggled to reach 10% in each of the past two years; the worst performance outside the global financial crisis since the late 1990s. The bottom line is that debt service capacity is diminishing even as debt service obligations continue to rise unsustainably fast.

And the economy’s nominal growth potential may diminish further over the next year, further narrowing the window available for effective reform and so a potentially benign ending to China’s credit boom.

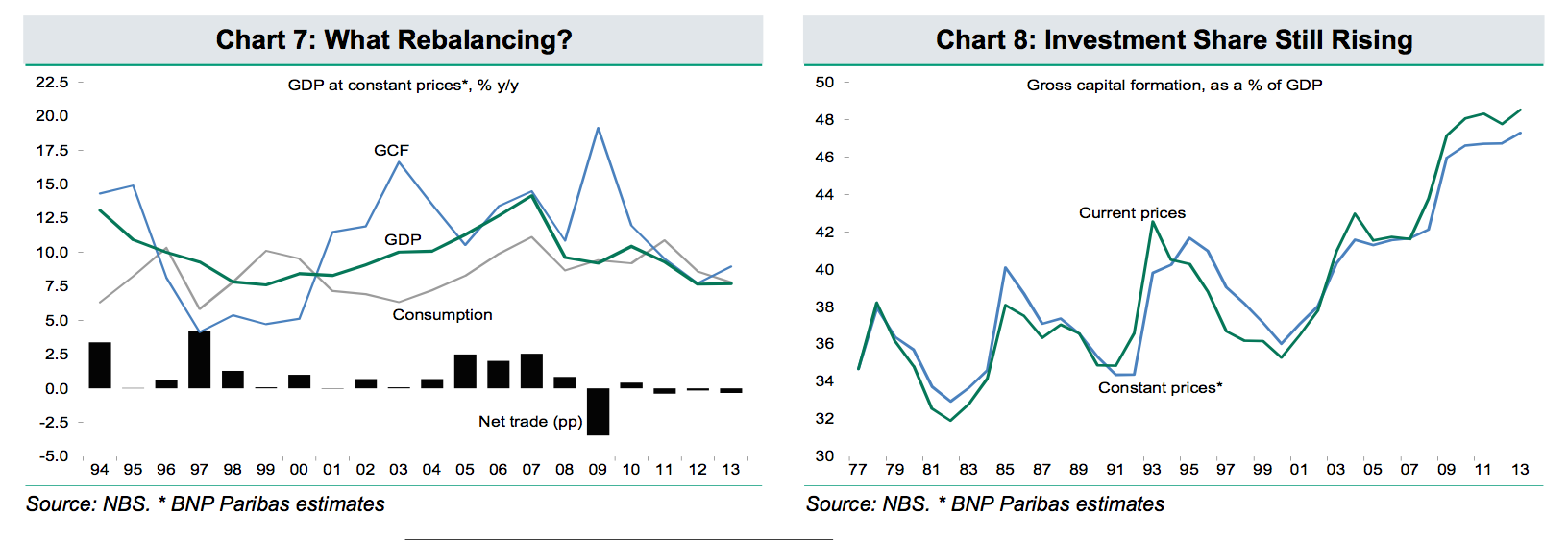

…A third widespread canard that bedevils the macro-debate over China is the view that slower economic growth implies rebalancing. Given an investment share of close to 50% of GDP and a household consumption share of around 35%, slower growth is a necessary but far from sufficient condition for rebalancing away from investment towards consumption. Despite a barrage of media headlines, there is little, if any, evidence of rebalancing towards more consumption-driven growth taking place. Rather, the Chinese economy over the last year or so appears to be getting the worst of both worlds; slower growth but investment-dependence becoming ever more extreme…

They conclude:

…the self-limiting argument that, because the Chinese authorities have been able to exert an impressive degree of control over cyclical volatility for many years, this will necessarily continue to be the case. This argument manages to conflate bad economics, poor history and unsound logic. The key lesson of the global financial crisis is that long periods of stability actually sow the seeds for bouts of future instability: the greater the apparent degree of control and stability, the greater the build-up of hidden vulnerabilities.

Philosophically, Bertrand Russell’s famous example of the farmer and his chickens offers a warning of the dangers of relying too heavily on supposed past empirical regularities to make over-confident forecasts for the future. Russell summarised the argument as ‘the man who fed the chicken every day at last wrings its neck instead, showing that more refined views as to the uniformity of nature would have been useful to the chicken’. While the Chinese authorities retain considerable ammunition to attempt to manage macro-volatility in the form of high reserve requirements and a strong central government balance sheet, the rising financial fragility of the economy, its still widening imbalances and its fading ability to generate strong cashflow growth all suggest that the degree of macro ‘control’ seen in the past will be increasingly hard to maintain and, to paraphrase Russell, more refined views of the uniformity of the Chinese business cycle are increasingly well advised.

I’d agree with most of that with the caveat that although slower growth may not necessarily signal rebalancing, it may not signal the opposite either. We may just not have slowed enough yet.

Of course timing is what matters and although well understood these structural adjustments are notoriously difficult to forecast. Authorities could kick the can once or twice more, I reckon, punting the problem perhaps a couple of years out. That would certainly be better for Australia as at least some of the capex cliff will be behind us. However, my base case remains that they will not. It will only make it ultimately worse.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.