Sell side analysis really is rubbish some days. I watched yesterday as various “analysts” declared the EM crisis over after Turkey hiked interest rates from 7.75% to 12% in one day. As I said:

This follows India’s 25bps hike yesterday. While wider markets are taking succor from these moves the next penny to drop will be slowing growth, which will be under serious and perilous revision in affected nations. These are the extreme examples but tightening is taking place across emerging markets, 40% of the global economy. I’ll take a punt and say taper pauses after the March tightening at ongoing Fed purchases of $45 billion per month.

That penny dropped last night and the Turkish lira collapsed again, to new lows, on fears of slowing growth:

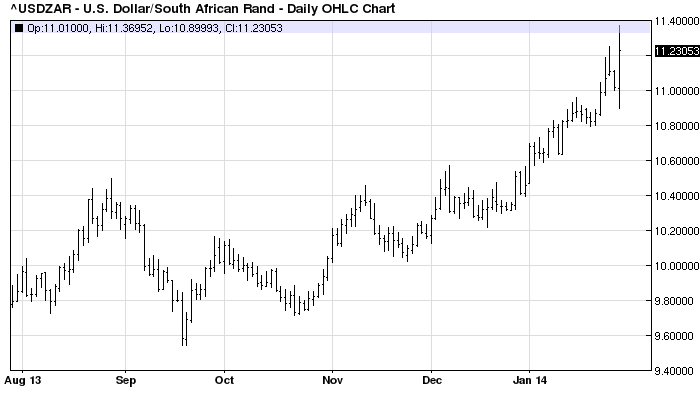

South Africa added to the fears by hiking interest rates 50bps overnight yet its currency fell as well:

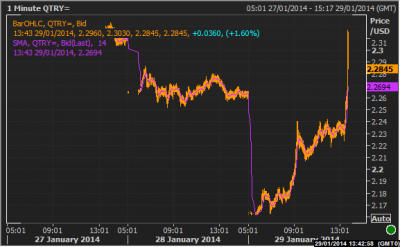

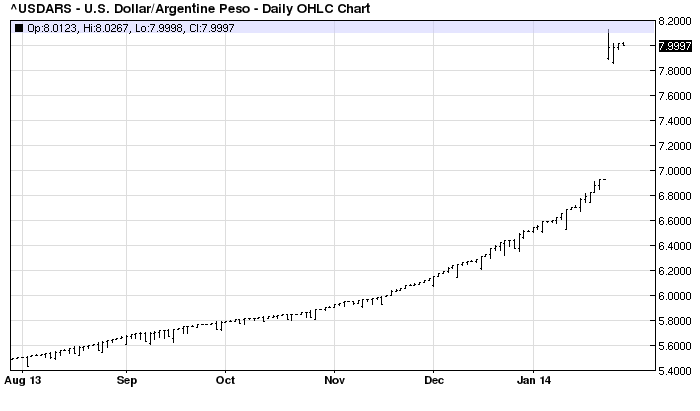

Indeed, contagion is spreading. Emerging markets now watching currencies take a flogging include Argentina:

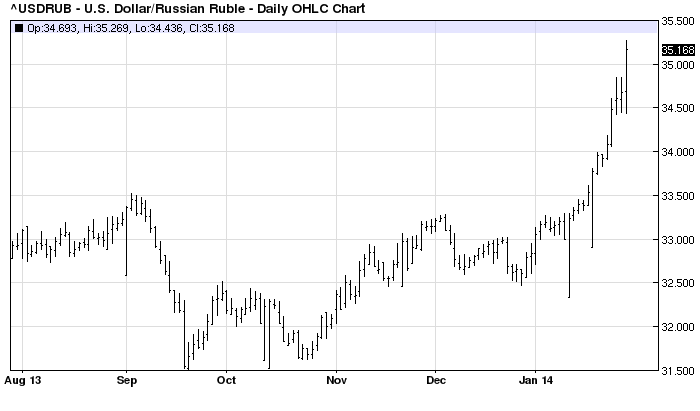

Russia:

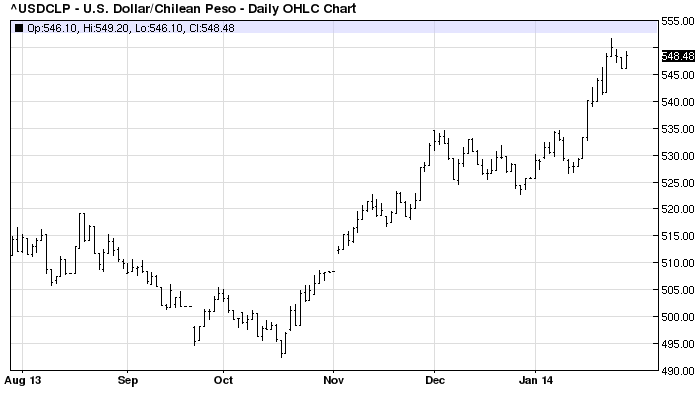

Chile:

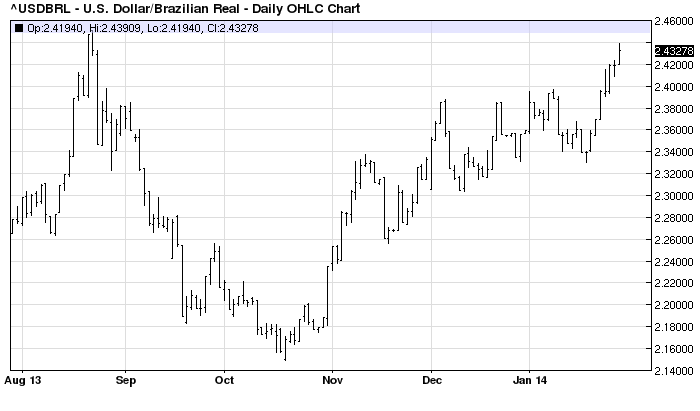

Brazil:

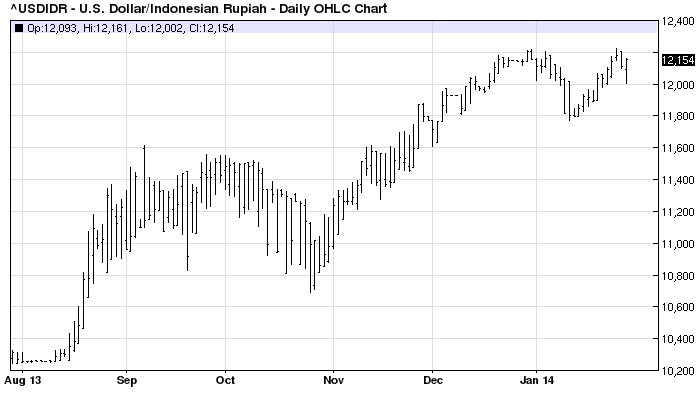

Indonesia

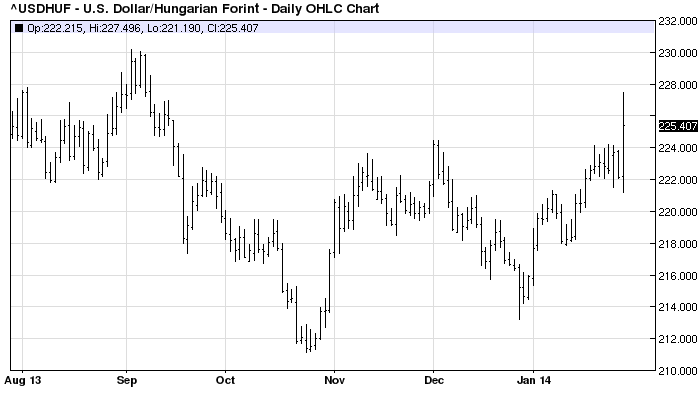

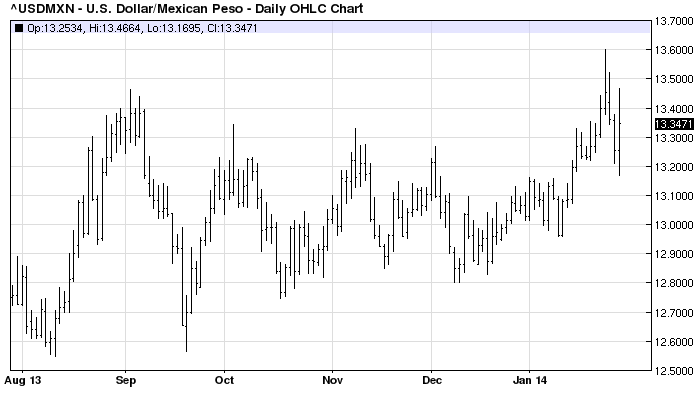

While Mexico and Hungary are threatening:

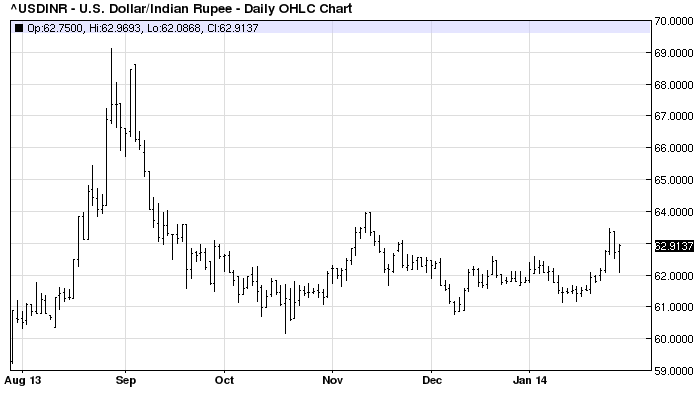

In better news, the Indian rupee appears to be stabilising:

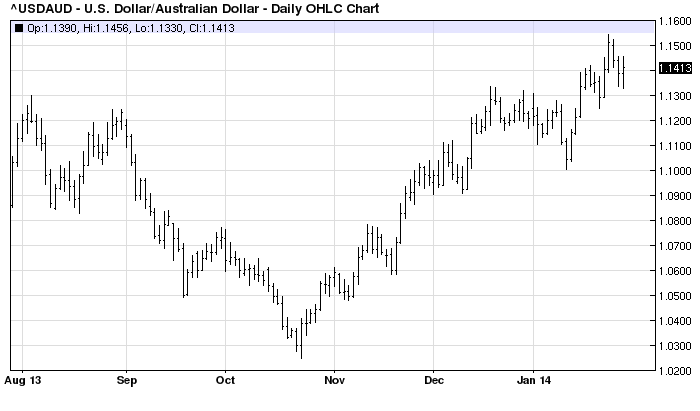

The Australian dollar also failed to rally:

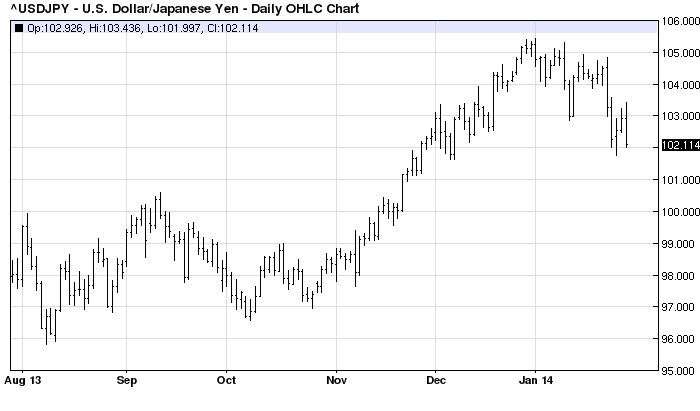

Meanwhile, the Japanese yen is undoing Abenomics on “risk off” flows, also hurting growth in the great mercantilist state in short order:

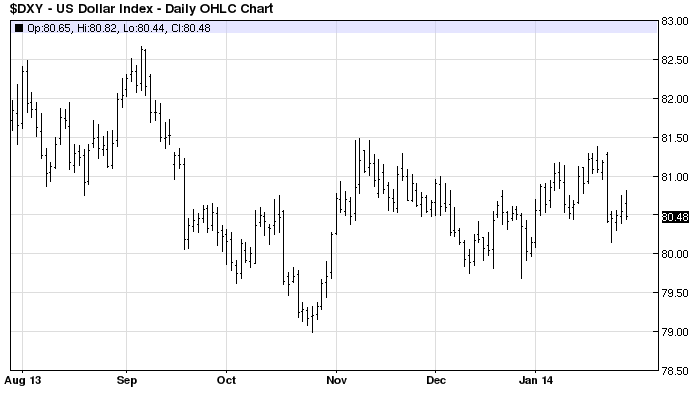

The US dollar was itself relatively stable and although bonds were bid last night, yields are holding on the expectation of more taper. Stocks were thumped of course:

So, if dramatic rate hikes aren’t going to reverse the rush for the exits in emerging markets, what will? One option is an aggressive Chinese stimulus but that would kill rebalancing.

If history is a guide then CitiFX has an answer:

- 1989-1991: Housing and savings and loan crisis: Fed eases aggressively as economy enters deep recession1992-1994: Existing financial architecture in Europe (ERM) blows apart

- 1995-1998: European convergence trade in both FX and Bond spreads keeps European currencies relatively stable vis a vis the USD with a good rally in 1998.By 1996 BUBA has lowered the discount rate to 2.5% while US rates remain well below the pre-crisis highs of 9.75% in 1989.

- The carry trade and capital flow into emerging markets (Asia in particular) is center stage

- March 1997: In a seemingly “innocuous” move the Fed “tinkers” by raising rates 25 basis points.

- April 1997: Japan raises its consumption tax as USDJPY has rallied from a post Kobe Earthquake low of 79.7 to 127.50 . USDJPY collapse to 111 by June

- June 1997-Jan 1998: Severe reaction in Asian currencies as “hot money flees”

- August-October 1998: Russia defaults, Long term capital folds and the Fed eases aggressively as the equity market drops 22% (S&P)

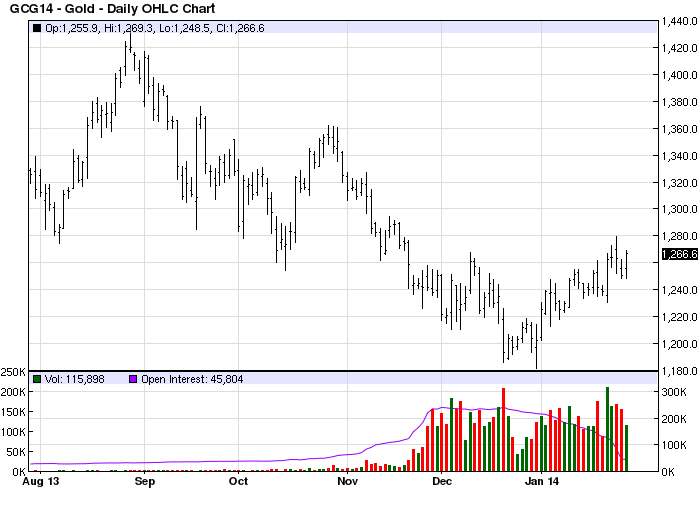

Fed eases aggressively as the equity market drops! A gold breakout will warn you in advance: