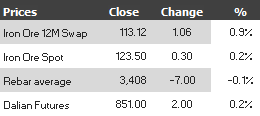

Find below the iron ore price table for January 22, 2014:

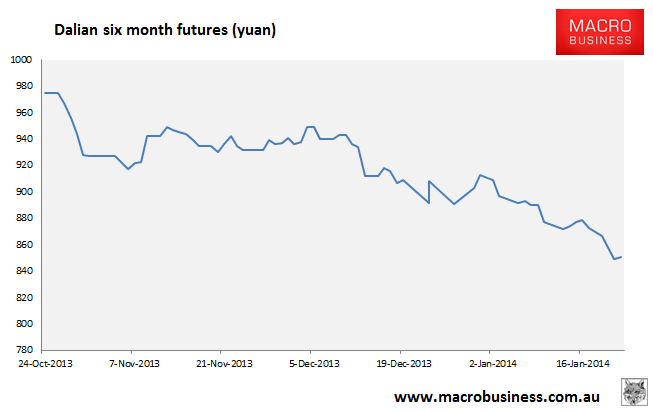

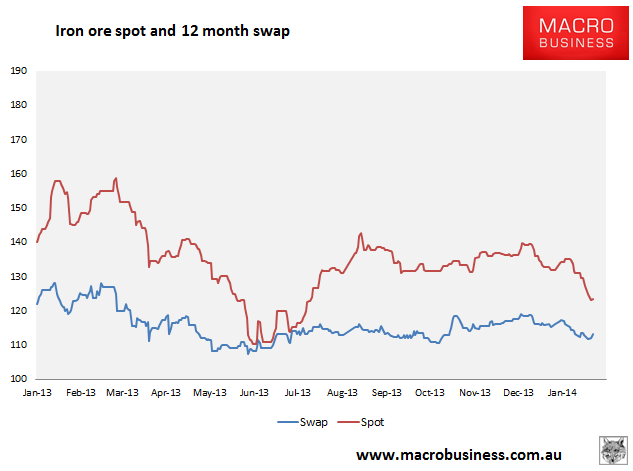

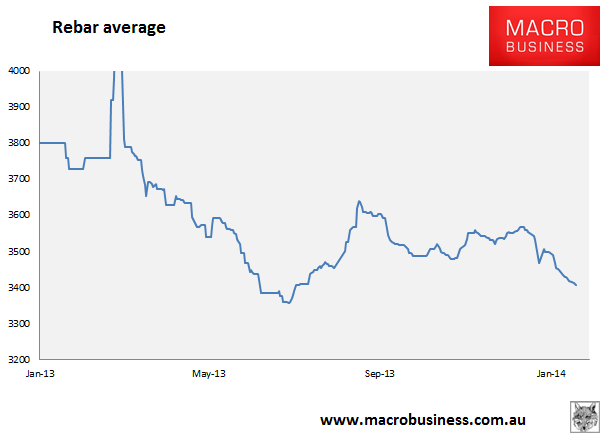

The charts:

Rebar futures also lifted a little.

Not terribly convincing as reversal but better than another fall!

Macquarie yesterday confirmed my recent ruminations of tentative Chinese destocking:

The latest Mysteel survey of iron ore inventory at Chinese steel mills shows an unseasonal destock over the past fortnight, to 28.1 days of use from 29.7 on the 3rd of January. This was accompanied by an $8/t drop in the spot iron ore price over the same time frame. In our opinion, this highlights the impact of the prevailing tight credit environment in China, which has left both steel traders and steel mills both unable and unwilling to build inventories. Should end demand remain strong, something recent property data (including a 35% YoY rise in new starts in December) suggests, this could lead to a strong steel demand push and price rises post Chinese New Year with inventory levels low. However, tighter credit also brings increased risk of weaker end demand into mid-year.

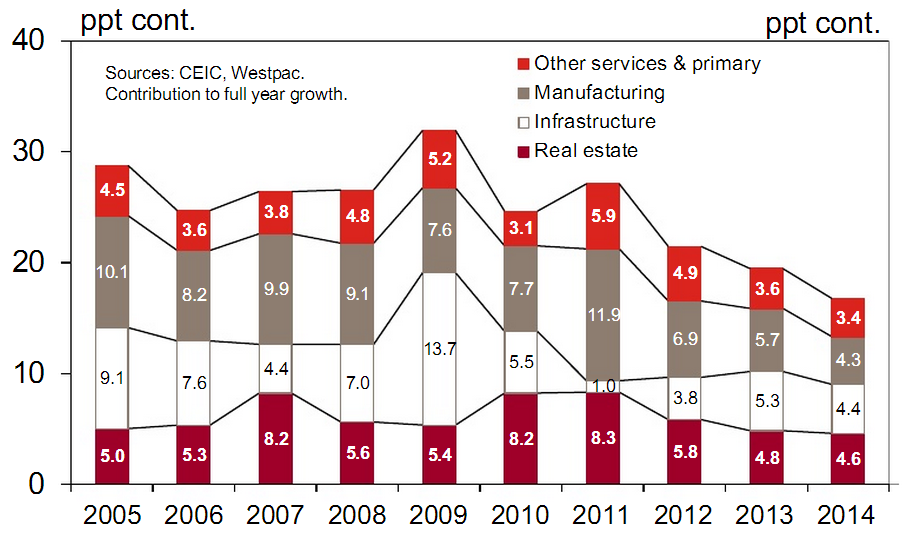

Property is a big component of demand and as I said in my 2014 forecast, we can expect support there. Here’s Phat Dragon’s breakout of fixed asset investment growth by sector:

Note the consistency of the real estate share but its not enough to offset the fading bounce in the 2013 infrastructure proportion. Without stimulus, iron ore will fall heavily.