ANZ has published its major projects update and, sheesh, this is going to hurt. Here is the capex cliff in all of its hideous glory:

In 2014 it falls about 1% of GDP. In 2015 it falls closer to 2% of GDP. In 2016 more than that again. ANZ reckons:

We continue to expect that investment within the resources sector will decline sharply from mid 2014, as a number of projects in the mining sector are finished and as construction on the first few mega-LNG projects winds down. We expect resources investment to decline by 3-4% of GDP over the next few years with around half of this impacting on domestic activity. With resources investment expected to decline sharply, it’s critical that other sectors of the economy respond further to low interest rates and the decline in the AUD. While housing market activity has improved sharply, the strength and timing of an upswing in non-mining business investment remains somewhat uncertain.

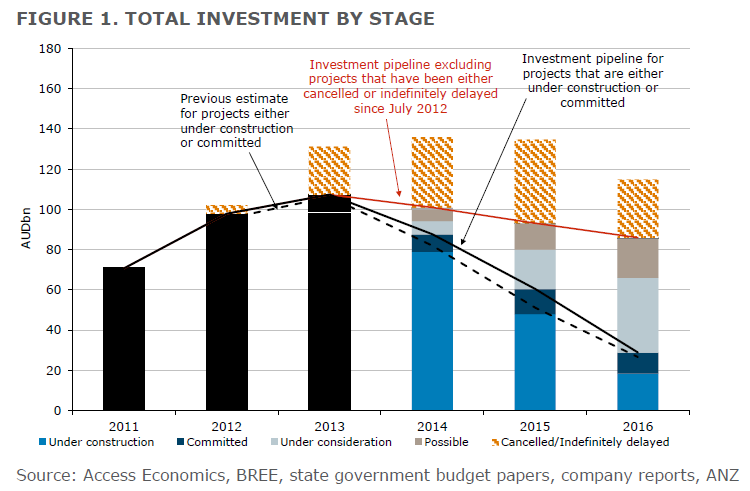

We have again revised lower the potential pipeline of major projects in Australia between 2014 and 2016 to AUD280bn from our estimate of AUD312bn in March. We have, however, upgraded our capital expenditure projection for those projects that are either committed to or already under construction to AUD180bn from AUD160bn over the same time period.

Investment in the energy sector remains elevated, but annual capital expenditure (excluding exploration) on LNG projects likely peaked in 2013 at around AUD55bn and will decline from 2014 onwards as the first few mega LNG projects near completion. The initial stages of both the QLNG and Gorgon projects are expected to be completed by the end of 2014 and H1 2015 respectively and the remaining projects (with the exception of Prelude) are expected to be finished by the end of 2016.

While conditions in the mining sector have shown tentative signs of stabilisation, there has been little evidence on the part of mining companies (or investors) to recommit to deferred projects or invest in new greenfield developments.

Encouragingly, state governments have signalled their intention to increase infrastructure investment, with a number of large-scale projects earmarked to proceed, which should provide support to activity from 2015 onwards.

As the investment phase of the resources boom winds down, the production phase will ramp up. Australian iron ore production is expected to increase to 685 million tonnes in 2015 from 550 million tonnes in 2013, with LNG output ramping up from 2015 onwards. We are currently forecasting resource exports to contribute around 1ppt to GDP growth annually in coming years.

I don’t buy a few points here. The first is the statement that half of the capex downdraft won’t affect “domestic activity”. That is clumsily put. Some percentage of falling capex will not affect headline GDP as net exports are boosted by falling capital imports, but the impact on domestic employment will be significant because the construction phase of the boom is the most labour intensive.

The second point is ANZ includes Arrow LNG as a watered down project doubtful in forecast which is bullish given doubts over it going ahead at all. Gorgon’s fourth train is probable because it increases project productivity.

Finally, on iron ore, these volume expansions are going to kill the price.

That all adds up to exactly what Leith and I have been arguing for several years. Headline GDP will be OK barring an external shock. After all, with population growth of 1.8%, we’ve got to go backwards 1.8% in per capita terms before we even enter a technical recession. But the realty of falling incomes and real activity are going to feel like a recession. Unless something else comes along!