Sweden’s housing market shares a lot of similarities with Australia.

As was the case in Australia, Sweden’s financial system was deregulated in the mid-1980s, which led to a house price boom and then correction as the Swedish economy entered recession in the early-1990s. However, whereas Australia’s banking system was almost brought to its knees via widespread corporate losses, Sweden experienced a banking crisis in the early-1990s after house prices crashed, as well as the nationalisation of Sweden’s banks by the government.

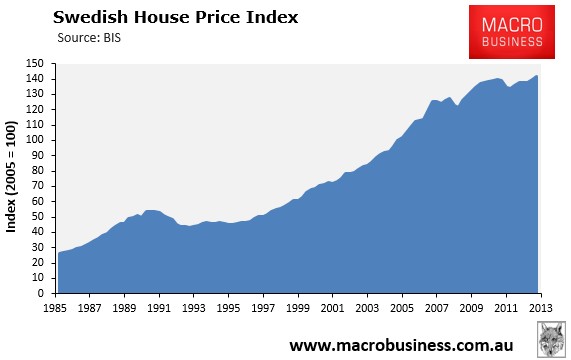

And like in Australia, Sweden also experienced a large house price boom that ran from 1996 to 2011, whereby prices rose tripled before flat lining in nominal terms (see next chart).

Swedish authorities also implemented a range of measures to stimulate the housing market and maintain the flow of mortgage credit during the onset of the Global Financial Crisis (GFC).

Whereas the Australian Government increased grants to First Home Buyers (FHBs), in Sweden tax breaks were implemented in 2008 for homeowners wishing to renovate newly purchased properties. Like in Australia, the government also stepped-up the provision of liquidity to the banking sector, guaranteeing the funding of the banks and mortgage institutions, as well as establishing a long-term stability fund to deal with any future solvency problems.

Arguably, the Swedish Government has accentuated the house price increases by operating policies that have stimulated substantial housing demand while also choking-off supply.

First and foremost, the Swedish tax system encourages house purchase over other investment options. In general, owner occupiers can deduct 30% of mortgage interest from their marginal rate of tax. Although there is also a capital gains tax of 30% on two-thirds of any price rises, this can be deferred as long as another owner occupied property is bought, and the rule applies to heirs as well.

A wealth tax was abolished in 2008 as was a national real estate tax, replaced by a lower municipal property fee, which helped to sustain the buoyancy of Swedish house prices.

Second, access to mortgage credit has been particularly loose in Sweden. In the years leading up to the GFC, loans were typically granted up to 95% of property value, although 100% plus loans were also available. Moreover, loan amortisation periods are particularly long in Sweden – at 100 years for houses and 200 years for tenant-owner apartments.

The Swedish planning system is also highly restrictive, resulting in homebuilding rates near the bottom of European countries. According to the RICS 2011 European Housing Review:

Housing construction costs are the highest in Europe, according to Eurostat, at around 55% above the EU average. The OECD attributes high house building costs to market structures that evolved in the era of high housing subsidies, limited competition, low levels of construction imports, and heavy regulations – all of which constrain competition and innovation.

Supply responsiveness is affected by land supply constraints. Land shortages occur for NIMBY reasons. Complex and lengthy processes of plan formulation and then appeals procedures generate considerable delay even where residential development is permitted. Furthermore, the structure of local authority finance discourages new development. Until the 2008 reforms, no local taxation was derived from property and municipalities still have large upfront costs, with little prospect of payback for many years to come, so the incentives still do not seem that positive.

The culmination of these drivers has seen the ratio of household debt to personal disposable income rise since the mid-1990s, reaching a record 163% in 2010. And mortgage debt as a share of household income rose from 73% in 1996 to 145% in 2010:

It has also had a pernicious effect on the young and disadvantaged, as explained by RICS:

The distribution of housing opportunities favours incumbent households over newly- or recently-formed ones and others wishing to move particularly into, and within, places where economic growth is strong. In other words, it is a system where lucky ‘insiders’ gain at the considerable expense of ‘outsiders’. This not only creates unintended social consequences but also imposes significant economic costs. Added to the cocktail is a political scene with recent closely fought elections, which have encouraged governments to cut property taxes and to put housing market reforms on the back burner.

Owner occupation has become the sole option for housing aspirations of many in a situation of constrained supply. This has encouraged a long trend of higher prices, which have generated wealth gains for some… and, so, has led to types of inequalities that the original interventions were supposed to smooth out.

The Swedish authorities have attempted to dampen demand by strengthening safeguards on excessive mortgage lending (but unfortunately not acting to free-up the supply-side). In October 2010, Sweden’s financial regulator, the Financial Supervisory Authority (FSA), capped mortgage loan-to-value ratios (LVRs) at 85%, a move that helped slow annual mortgage growth from more than 10% between 2004 and 2008, to 4.5% in December 2012. And earlier this year, it sought to to impose further LVR limits as well as increase capital adequacy requirements on Swedish mortgage lenders.

Now Bloomberg has emerged with an eye-opening article on the Swedish housing market, which warns of an impending house price crash:

“The Swedish housing market is dangerously overvalued,” says Bengt Hansson, a researcher at the Swedish National Board of Housing, Building and Planning (Boverket).

In October, he estimated house prices were 25 percent above fair market value, with apartments even more overvalued.

As prices have risen, buyers have taken on more and more mortgage debt, aided by record-low interest rates and interest-only mortgages…

As debt balloons, Swedish politicians, policy makers and bankers are feverishly debating whether they face a bubble and what, if anything, should be done to deflate it before it pops. The issue has been the subject of a half dozen parliamentary committee hearings; has split the executive board of the Riksbank, Sweden’s central bank, and has occupied acres of newsprint.

“It’s very, very important that debt doesn’t go up further,” Riksbank Governor Stefan Ingves, who’s also chairman of the Bank for International Settlements’ Basel Committee on Banking Supervision, told Sweden’s parliament in October.

“This is a problem we need to address today,” says Uldis Cerps, executive director for banking supervision at the Swedish Financial Supervisory Authority (FSA), the country’s bank regulator.

Sweden is experiencing a housing bubble and will face an inevitable crash, Nobel laureate economist Robert Shiller said in an interview with business newspaper Dagens Industri published on December 7…

The debate over a potential bubble is a vindication for Boverket’s Hansson, a soft-spoken researcher who toils in a tiny office on Norrlandsgatan, a boutique-lined Stockholm street. Hansson became troubled by the rapid increase in house prices in 2007.

“The real value of owner-occupied houses in Sweden had been stagnant for almost 50 years,” he says. Suddenly, prices jumped 80 percent from 2000, with the going rate for apartments rocketing up almost 150 percent. “Something very strange was going on,” he says…

According to the Riksbank, housing starts, about 20,000 units in 2012, are less than half what they were during the late 1980s and early 1990s, when the government provided builders generous subsidies and tax incentives.

Meanwhile, demand continues to rise. Sweden’s population, currently 9.5 million people, has expanded rapidly due to immigration and higher-than-expected birthrates, according to Statistics Sweden, a government agency. In 2012, the population grew by 67,000, or 0.7 percent, and Statistics Sweden forecasts it will increase by more than 80,000 per year during the next five, the fastest rate ever.

Strict planning and environmental rules that mean it can take a decade to build new apartments in Stockholm have scared off developers, Karamouzis says.

In addition, the combination of government rent control and a prevalence of co-op buildings (called federations in Sweden) reduces incentives for developers to build and constrains the supply of rental units, compelling more people to buy…

Sweden’s whole economy is living on borrowed time. And you can’t refinance the clock.

While no one can say for certain whether Sweden’s housing market will blow-up like it did in the 1990s, the signs don’t look good.