Business Spectator’s newb, Callam Pickering, argues the case today:

Investors have jumped on board the Sydney bandwagon but if they have invested in other cities recently then they would be disappointed in the results.

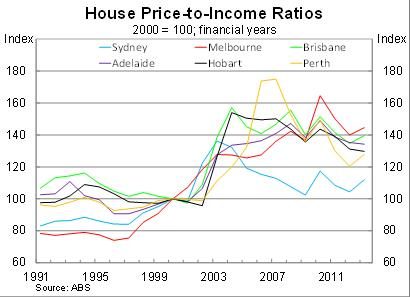

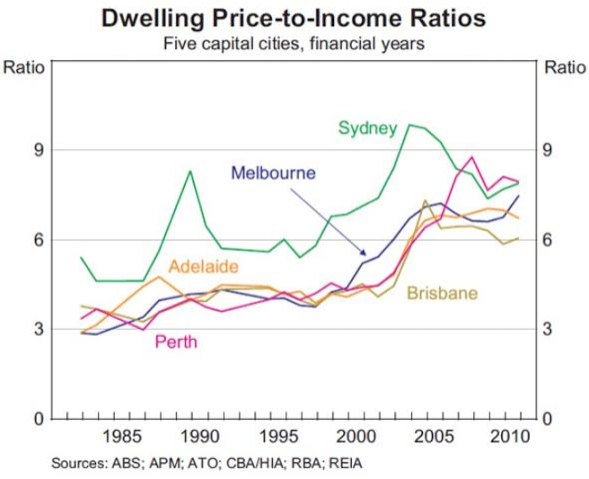

The state national accounts, released last week, provide information on the average gross disposable income in each state. This data can be used to assess which states have the highest relative house prices.

The house price-to-income ratio is below its peak in each city, in some cases significantly so. Generally the ratios show broadly similar trends with two main exceptions: Sydney house prices tend to do their own thing and Perth house prices rose to unprecedented highs during the first commodity price boom.

This is an index chart showing relative changes in capital city ratios. Sydney is lowest because it had the highest starting point. Here is the chart of actual ratios:

Advertisement

A bit behind the times and note as well that this is from the ABS household income survey. The RBA has previously used national accounts to calculate income to produce its absurdly flattering median price-to-income ratio of four.

But back to Pickering, is he right when he concludes:

Expect price growth to slow and perhaps even decline in 2014.

Advertisement

First, his read on the economy is right. As today’s GDP showed so clearly, the defining experience for households in our new GDP mix is going to be no income growth. There is also increasing supply hitting some housing markets and slowing price rises, especially in Melbourne where exuberance has eased. But will that stop house prices next year? It’s a bold call unless the RBA invokes macroprudential policy.

The moment house prices stall, consumer spending will as well. The economy is going to be facing all kinds of broader headwinds at the same time, including falling terms of trade and business investment and probably rising unemployment. Thus, if housing weakens, interest rates will immediately be cut again. And they will keep going down every time housing slows until the dollar is low enough to fire up a sustainable recovery in the tradable sectors. It’s hard to know where that is exactly but I’d guess 75-80 cents at least is needed and for an extended period.

That opens the possibility that housing can rise again on more debt as opposed to income growth. At some point there’ll be a cap on that as well. The RBA will not want household debt ratios to blow out to new records and APRA will not want banks borrowing offshore. But where the tipping points for those imbalances are is tough to predict. And remember, the post boom adjustment of falling business investment has three years to run.

Advertisement

Ironically, the best hope for Pickering’s stall is probably a dollar that falls harder and earlier than markets expect. A shock of some kind, perhaps China slowing, would also trouble housing.

None of this makes much sense. We should already have macroprudential and rates at 1% and be repairing competitiveness and working up a sustainable recovery instead of playing around with bubbles. The longer we don’t, the greater the Sydney bubble risk becomes and the chance that other markets follow, income growth be damned.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.