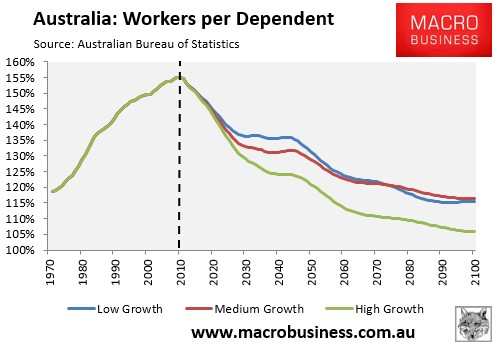

Australia’s retirements system is riddled with problems that make it both unsustainable and inequitable in the face of Australia’s rapidly ageing population (see next chart).

One of the many flaws in is that the superannuation system allows an individual to retire at 60, withdraw their super tax free as a lump sum, piss the money away on their homes or on consumption, and then go on the aged pension from 65 years of age. In such instances, the taxpayer is left wearing the cost of superannuation concessions throughout the individual’s working life, and then again once that same individual goes on the aged pension. Put simply, it is a loop hole that must be closed, and taxing superannuation lump sums, whilst at the same time encouraging retirees to withdraw their savings as a annuity (instead of the pension), is a good step.

When I have raised these concerns previously, some readers countered that I was scaremongering and had no “proof” that such behaviour was in fact taking place. Well, the release of the latest Retirement and Retirement Intentions survey by the Australian Bureau of Statistics (ABS) has put paid to that, with the survey identifying that more than half of retirees withdraw their super as a lump sum, with many then blowing the windfall on their homes or a new car:

Of the 3.3 million people aged 45 years or over who were retired from the labour force, 2.0 million (61%) had made contributions to a superannuation scheme. Men were more likely to have made contributions to a superannuation scheme than women. Just under three quarters (72%) of retired men aged 45 years and over had contributed compared to 52% of women (Table 10).

Of those who had made contributions, 55% had received all or part of their superannuation funds as a lump sum payment (54% of men and 57% of women). Many of those who received a lump sum payment used it to pay off or improve their existing home or purchase a new home (32% of men and 31% of women) or to buy or pay off a motor vehicle (14% of men and 11% of women).

Meanwhile, the ABS survey also found that reliance on the aged pension increases the longer someone is retired, suggesting that superannuation is failing in its objective of replacing the aged pension:

For many people, their main source of personal income in 2012–13 at the time of the survey, changed from that at the beginning of their retirement with more people becoming reliant on a ‘government pension/allowance’. While 1.5 million (46%) of those aged 45 years and over who had retired reported that a ‘government pension/allowance’ was their main source of personal income at retirement, almost 2.2 million (66% of all those who were retired) indicated that this was now their main source of current personal income. This represents an increase of 45% compared with the number of people who stated that it was their main source of personal income at retirement.

Obviously, the exclusion of the family home from the assets test for the aged pension adds to the incentive for retirees to access their super as a lump sum, since they can sink the funds into the family home and have the wealth sheltered from the means test for the pension. This is why the family home (or some part thereof) needs to be included in the pension assets test, in order to ensure that taxpayer assistance only goes to those most in need.

unconventionaleconomist@hotmail.com