John Piggott, director of the ARC Centre of Excellence in Population Ageing Research, wrote an interesting article over the weekend on the ageing conundrum facing Australia, and proposing to raise the rate of GST to mitigate the budgetary impacts. From The AFR:

Demography gets much less attention from economists than it ought. Population ageing dynamics generate changed government outlays and economic growth patterns. Take the idea of a demographic dividend – a period when low fertility and still evolving late-life longevity mean that the working age population makes up an unusually large proportion of the total. A buoyant labour market and limited calls on government outlays to support education and retirement transfers mean governments sometimes reduce taxes and neglect pension access age.

Then there’s a flip point, and within a few decades the picture is entirely reversed. Social support structures require more government expenditures and the labour tax base shrinks relative to GDP… We’re now experiencing Australia’s flip point – the population share of those aged 15 to 64 peaked in 2009…

At the same time, life expectancy at mature ages is increasing. Whereas most of the life expectancy increase in the three decades following World War II was generated by declines in mortality at young ages, in the last 30 years the increase in life expectancy has come from reduced mortality at later ages, generated by medical and pharmaceutical breakthroughs, and also behavioural changes such as reduced smoking…

This trend to a longer life and an older population will continue. What can policymakers do?..

One of the most important levers to encourage older people to remain in the workforce is to increase pension access age. The superannuation access age need not be the same, but it shouldn’t be far off…

More imaginative retirement products, and the market and regulatory structures to support them, would help…

And then there’s the revenue requirement. Tax as a proportion of GDP will have to increase to maintain the age pension and health services at their current levels…

For my money, some increase in consumption taxes seems inevitable. It is less distortionary than most other taxes, it reaches the retired as well as workers and is therefore robust to changing ratios of retirees to workers, and the poorest in the community are largely protected because they tend to rely on government transfers which are indexed.

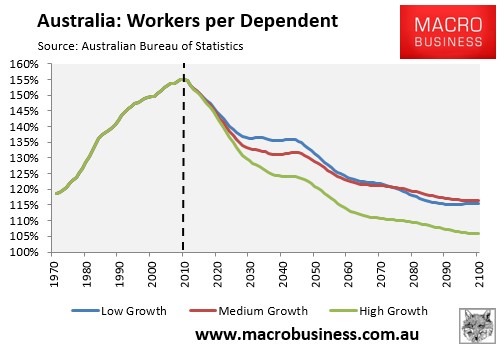

Piggott’s article pushes all the right buttons. The ABS’ recently released population projections showed that Australia’s demographic flip point was hit in 2010, with the ratio of workers per dependent now projected to be in terminal decline under each of the ABS’ population growth scenarios (i.e. low, middle and high):

With a lower share of workers supporting retirees, the Federal Budget is facing a big hit as a declining tax base meets higher outlays for health, aged care, and pensions. This calls for tough policy decisions aimed at placing finances on a more sustainable footing.

Raising the access ages for the aged pension and superannuation are a no-brainer, as are more imaginative retirements products, such as annuity-style superannuation pensions and reverse mortgages. Broadening and raising the rate of GST is also sensible, as it is a relatively efficient tax and would share the tax burden with the growing share of people no longer in the workforce.

However, these reforms on their own do not go far enough.

As argued repeatedly, a major failing of Australia’s retirement system is that it directs the lion’s share of superannuation tax concessions to higher income earners – i.e. precisely those whom are least likely to need the pension – instead of sharing concessions more evenly across the income distribution.

Accordingly, the Government should look to replace the 15% flat tax on super contributions with an flat concession (say 15%), thereby: 1) providing all taxpayers with the same taxation concession; 2) boosting lower income earners’ super savings and thus reducing reliance on the aged pension; and 3) reducing overall costs to the budget.

Further, access to the pension is also distorted by not including the biggest asset most households own – the family home – from the assets test. This results in a large number of wealthier households gaining access to taxpayer assistance when they are well placed to look after themselves.

In any event, the growing debate around retirement policy is welcome. With Australia’s population ageing fast, and the proportion of workers to non-workers set to decline significantly in the decades ahead, the Government will ultimately be forced to scale back entitlements as the tax base shrinks. Therefore, it is better to begin the reform process now rather than waiting until there is a Budget crisis.

unconventionaleconomist@hotmail.com