A terrific report today from PIMCO nails Australian issues, even if our elites cannot.

- In 2013, real growth in business investment in Australia outside the mining sector slowed to almost zero, in part due to the high exchange rate.

- While some sectors of the economy such as housing appear to be improving, we continue to expect sub-trend growth in 2014 due to the subdued outlook for business investment.

- The RBA will most likely have to keep interest rates low for an extended period to ease the transition away from mining-assisted growth and encourage a weaker exchange rate.

Australians will remember 2013 in part for the fall of some of our national corporate icons. The Ford Falcon and Holden Commodore are unlikely to be produced domestically going forward, and Qantas has unsuccessfully sought subsidies from the Federal government. Due to elevated cost structures and a high exchange rate, Australia Inc. is increasingly unable to compete in a fiercely competitive global market.

High on the Reserve Bank of Australia’s (RBA) Christmas wish-list this year will be a lower exchange rate and a business community more willing to loosen its purse strings in 2014. Unfortunately, the first wish will likely need to be granted before the second can be realized. We expect the RBA will need to keep policy accommodative over the cyclical horizon and 2014 will be a critical transition year for the Australian economy.

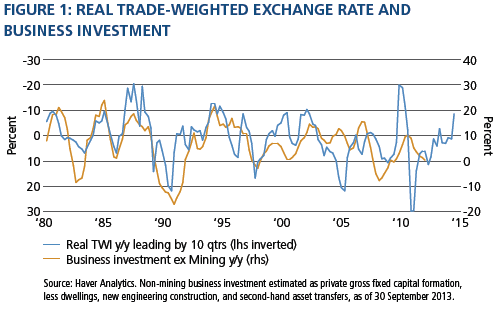

Over the year through September 2013, real growth in business investment outside the mining sector slowed to almost zero (0.5% to be precise, as shown in Figure 1). Why has Australia Inc. invested so little into its businesses this year? As RBA Deputy Governor Philip Lowe commented in a speech in late October, the lack of business investment in recent years is actually a global phenomenon across the developed world.

Although hard to quantify, this “investment drought,” as Lowe described it, has likely been influenced by a lingering risk aversion after the financial crisis as well as the political uncertainty that has been common in many developed countries over the past few years. But in Australia another variable has also been restraining non-mining capital expenditure, and that is the elevated exchange rate.

As Figure 1 shows, changes in the real trade-weighted exchange rate have historically led changes in non-mining business investment. As the real exchange rate appreciates, domestic products and services become less competitive relative to foreign goods and services, both at home and abroad. And of course, the reverse is true when the real exchange rate depreciates.

Another important point that Figure 1 illustrates is that exchange-rate movements impact the real economy with long lags. Historically, it has taken two years or so for the transition mechanism between the exchange rate and the real economy to work, meaning the full impact of this year’s currency depreciation is unlikely to be felt before 2015.

Critically, it is the real exchange rate that matters when determining global competitiveness (that is, the nominal exchange rate adjusted for inflation differentials between countries). The real exchange rate can appreciate (and domestic companies become less competitive) either because the nominal exchange rate rises, or because the price of domestic goods and services rises faster than world prices while the nominal exchange rate remains unchanged. Take Holden as an example. An Australian-made Holden Commodore can become expensive relative to an imported Volkswagen Golf either because Australian input prices (e.g., wages, parts, etc.) are higher than global input prices, or because the nominal exchange rate rises, making imported VWs cheaper.

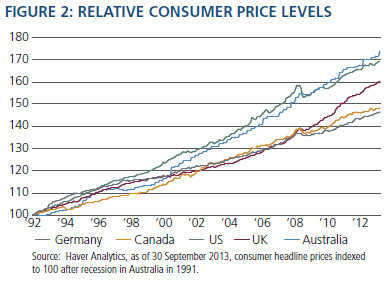

Viewed through this lens, it is unsurprising that Australian businesses have been hesitant to invest: They have felt increasingly uncompetitive. Twenty-two years without a recession has generally meant that prices in Australia have continued to rise, while in other countries economic downturns have resulted in periods of price adjustment. One way of illustrating this is Figure 2, which shows headline consumer prices for five developed countries starting after the last recession in Australia in 1991. Amplifying this growing price disadvantage over recent years has been the very strong nominal exchange rate.

Following the RBA’s policy meeting in December, RBA Governor Glenn Stevens noted, “A lower level of the exchange rate is likely to be needed to achieve balanced growth in the economy.” We agree. The critical variable will be how Australia Inc. responds. Because of the historical lag between changes in the exchange rate and changes in business investment as well as the subdued capital expenditure responses in recent business surveys, we remain cautious heading into 2014. We also expect that structural change will continue to affect the composition of growth in the Australian economy. (Please see the Viewpoint, “Dutch Disease Lite in Australia’s Economy,” April 2012.)

Investment implications

2013 was a challenging year for both policymakers and Australia Inc. While there have certainly been signs that some sectors of the economy such as housing are improving, we continue to expect sub-trend growth over the coming year due to the subdued outlook for business investment. To ease the transition away from mining-assisted growth and encourage a weaker exchange rate, the RBA will most likely have to keep policy accommodative via low interest rates for an extended period. So how do we think investors should be positioned heading into 2014?

- Own Australian duration at the front end of the yield curve.With anchored domestic monetary policy and the US Federal Reserve likely to reduce its purchases of US Treasury bonds (potentially putting upward pressure on global long-term yields), the probability of the domestic yield curve flattening significantly is low. At the same time, due to the shape of the yield curve, the three-to-five-year maturity sector provides the highest expected return per unit of duration.

- Position for a weaker exchange rate.Stopping short of physical intervention, the RBA has clearly stepped up its verbal assault on the Australian dollar in recent months. As the exchange rate is such an important variable in determining the competitiveness of Australia Inc. and therefore how smoothly Australia rebalances its growth engines next year, we expect this RBA rhetoric to continue. Two other factors should also be working in the RBA’s favour to achieve a lower exchange rate over the cyclical horizon:

- The increase in iron ore supply will likely exert downward pressure on iron ore prices and therefore Australia’s terms of trade. Our credit team is expecting the increase in iron ore supply from the four largest producers (Vale, Rio Tinto, BHP and Fortescue) over the next two years to exceed the incremental increase in demand from China over the same period. Given that China represents approximately half of all global iron ore demand, this supply/demand imbalance should exert downward pressure on Australia’s terms of trade.

- Foreign capital inflows that have kept upward pressure on the exchange rate over recent years are likely moderate going forward. Foreign direct investment into the mining sector will likely subside as the resource-project pipeline continues to taper next year. Additionally, despite a spike in the third quarter of 2013, foreign purchases of Australian government bonds have generally been much less aggressive.