The recent pick-up in Sydney house prices is a product of investor speculation, though investors continue to support activity in a number of other states. Investor activity is at an unprecedented level in Sydney. When this inevitably normalises, Sydney house prices will decline.

Housing market activity has picked up significantly since the Reserve Bank began its latest cutting cycle. Owner-occupiers are taking the opportunity to upgrade on their existing purchases, while investors believe there are opportunities to make a quick buck.

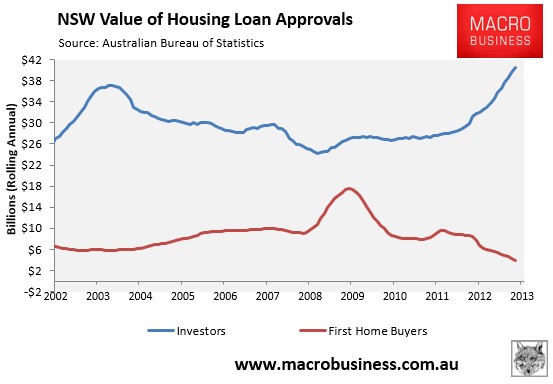

But for first home buyers, it has been an entirely different story: their activity has never been weaker.

We all know this story now, captured by UE’s extraordinary chart:

Pickering then looks forward:

So what will happen now?

We are not often certain about anything in the housing market, but we can all agree that the recent rise in investor activity in New South Wales is not sustainable. Investor activity in Sydney will inevitably slow and, when it does, it will happen quickly.

As a result, Sydney house price growth will slow significantly and more than likely begin to decline once investor activity normalises. It wouldn’t surprise me if Sydney saw something similar to when the first home owner boost was removed in 2009 and house prices gradually declined over the following two years.

For the other states, it is less clear. Investors may begin to move their attention towards other states and that could support house price growth. However, I see a period of soft growth in these states, particularly given the weakness in first home buyer activity. Outside NSW, I expect house price growth to be at around the same pace as income growth over the next couple of years.

The 2003 episode had a soft-landing for two reasons. First and foremost it transpired as the mining boom took off, supporting incomes as asset prices fell. Second, that supported national activity with enough vigor for the housing bubble to go national as Sydney stalled.

This time around, it Sydney does stall and begin to fall then the underlying condition of the economy will be exposed as very weak. Consumers will retrench and the RBA will immediately be forced to slash interest rates again, risking another leg up in the speculative blowoff.

This situation is not dissimilar to the pickle that the Fed finds itself in with its stock market bubble. Tapering and bursting the bubble only leads swiftly to more easing and a bigger bubble. Do nothing and your bubble gets bigger anyway.

The fact is that the more dependent you become on the bubble to support your growth, the more monetary policy loses its incremental power and instead becomes an on/off switch.

The only way I can see a soft-landing in Sydney is via macroprudential policies which restore some of the incremental power of interest rates as tightening in the distribution of credit can be offset by concurrent easing in its price. Even the effects of that are debatable, though New Zealand will give us a test case in Auckland.