Morgan Stanley offer five reasons to be bullish on Australian equities today:

Transition East: We remain constructive on the upside potential for Australian equities in 2014e. Our 12-month forward target for the ASX 200 (end 2014) is updated at 5,700 (+17% total return). Our base case forecasts are underpinned by our belief in a successful transition from

Resource Boom to East Coast recovery – a combination of accommodative monetary policy, a sustained housing-related cycle, and improved clarity of fiscal policy.

Five Key Themes for 2014:

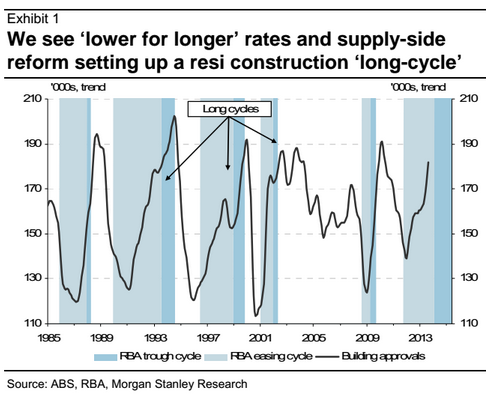

Late-Phase Bubble vs Early-Stage Cycle

The key debate for stock pickers in the last 6-9 months has been whether Australia is in the midst of an early-stage housing and construction cycle – or in the heady phase of a housing bubble. There has been much focus on the increase in prices received at auction as proof of a bubble, but we see such price outcomes as an acceptable cost of transition to an East Coast Recovery. Top picks: LLC, SGP, DLX, REA.

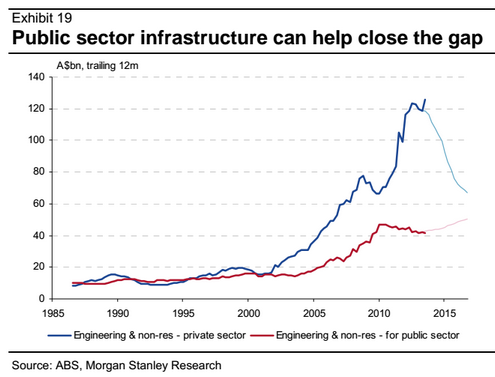

Watch for Infrastructure Signaling:

To build will take time – but we see the signaling and intent around Tier 1, 2 and 3 public infrastructure spending as an important waypoint for medium-term improvements in business and consumer activity.

Monetary policy is now spurring demand-side growth – so the ball is entering the court of government to deliver reforms and policy that can help unlock the supply side. We see this element as crucial to the sustainability of the East Coast

Recovery strategy, helping to turn a cyclical recovery in asset prices into a medium-term build-out of infrastructure-equipped housing supply. We are optimistic that in 2014 the new Federal government will work with the states to advance a major program of public infrastructure spending. Key ideas: MQG, CDD and BSL.

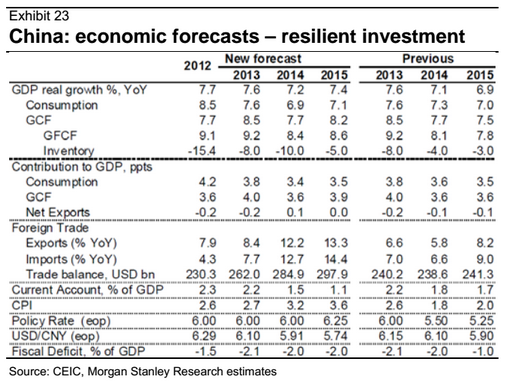

Reform de-risking the Chinese growth model

At the end of a year dominated by focus on the Chinese reform agenda (culminating in the mid-year SHIBOR crisis) or lack thereof (following a mini-stimulus and re-stocking phase from 3Q13), the new Xi-Li leadership looks to have consolidated power and delivered a constructive reform agenda through the Plenary session (see A Full-Bodied Reform Guideline with Strong Political Backing). We see this reform de-risking the growth model, presenting select opportunities in large cap iron ore, copper and energy names. MS Iron Ore supply-demand analysis suggests 2014 resilience in Australia’s bellwether commodity – all supporting select plays in resources, such as FMG, BHP and MIN.

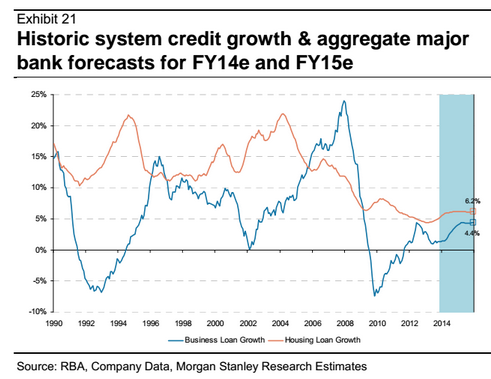

Credit Growth Forecasts Remain Cautious

Recent bank earnings upgrades have been linked to better than expected asset quality. Consensus remains cautious on lending growth (particularly business credit) – this could change should activity cycles on the East Coast start to turn.

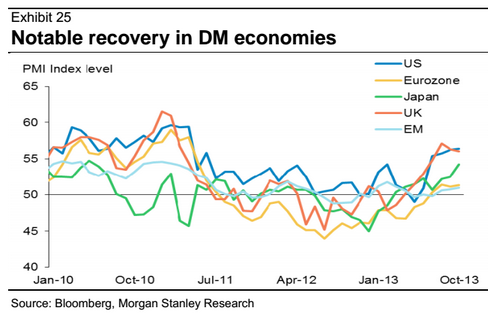

Living in a World of DM over EM:

Our global economics team sees 2014 as marking the transition to a ‘sounder, safer and more sustainable’ second half of the post-GFC expansion. This will require successful transitions in policy stances and growth models across the major regions, but we are optimistic that global growth can pick up from 2.9% in 2013, to 3.4% in 2014 and 3.7% in 2015. Supportive for: BXB, NVT, DMP, RMD, LLC and FOX.

Jesus, a new boom! I suggested this morning in my equities special report that cyclicals and dollar-exposed industrials would be the play for 2014 from the sell side. Sadly, MS’s risk analysis is non-existent.

The Australian housing surge is a late stage bubble surge even if it’s necessary evil. Government infrastructure is not likely to kick in until 2015/16 owing to long lead times. The idea that China has been “de-risked” by the Plenum doesn’t pass the laugh test. Australian credit can grow but not for long if investors keep driving it because the RBA will be forced into macroprudential tools. Developed markets are my favoured play but their growth is driven by renewed bubbles to real recovery.

By failing to address any risk whatsoever, MS is free to claim that:

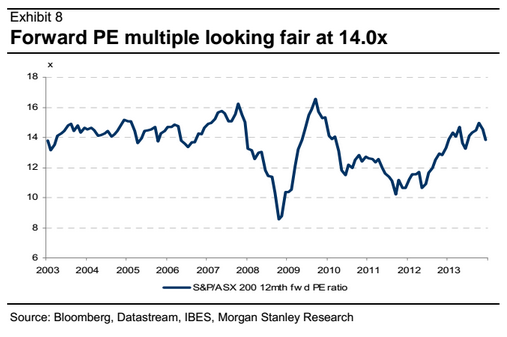

Given the re-rating, the S&P/ASX 200 is now trading on 14.0x 12-month forward, putting it between its 2003-07 mid-cycle average (14.5x) and its full post-2003 average (13.5x).

MS is forecasting a 5700 on the ASX by year end. Quite possible. But it’s not risk free and a market without financial repression would be discounting much higher risk. Which means you aught to be a well.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.