From the Australian Workforce and Productivity Agency today comes the first study I have seen aiming to quantify the effects on the labour market of the mining capex cliff (actually the modelling was done by Deloitte Access Economics):

Many media commentators have speculated the boom is coming to an end, as commodity prices slacken, investment declines and global competition intensifies. Industry experts dispute this view—as does the Australian Workforce and Productivity Agency (AWPA)—and instead describe an industry in transition, as some of the biggest projects ever undertaken in Australia move from the construction phase to the less labour- and capital-intensive operations phase. In April 2013 the Bureau of Resources and Energy Economics valued committed investment in resources and energy major projects at $268 billion and estimated uncommitted investment at $379 billion. Developing and maintaining the capacity and expertise required to drive the operations phase will be vital to Australia’s ongoing prosperity.

In this report, the third annual report prepared by AWPA on Resources Sector employment and skills needs, we consider the implications of these changing circumstances on the demand for, and the supply of, the skills and workforce capacity required to deliver major mining and oil and gas projects. AWPA commissioned a comprehensive employment demand and supply outlook model for the Resources Sector. This model—using Bureau of Resources and Energy Economics data available as at April 2013—details projections for 2014–18 across three subsectors (Resources Project Construction, Mining Operations and Oil and Gas Operations) under three economic growth scenarios (base case, high growth and low growth).

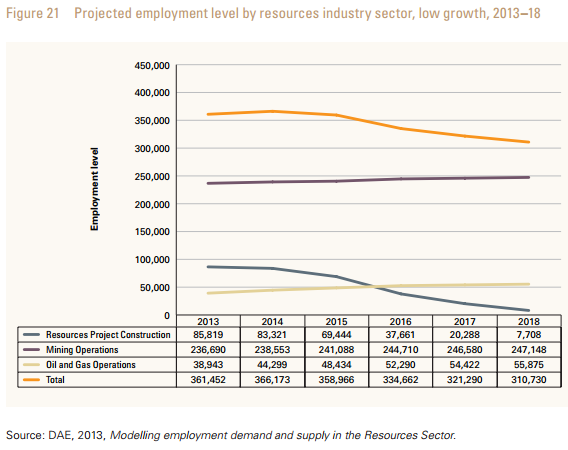

- A highly volatile phase lies ahead for Resources Project Construction, which is expected to see employment plateau at first and then decline rapidly in coming years. Under the low growth scenario (considered the most likely due to the lower probability of projects proceeding to the committed stage), employment is expected to drop slightly from 85,819 workers in 2013 to 83,321 workers in 2014 and then decrease quickly to 7,708 by 2018. This decline is common to all three scenarios, and is likely to force many thousands of trades workers from the domestic workforce to seek employment in other industries, unless their skills can be transferred to mining and oil and gas operational roles.

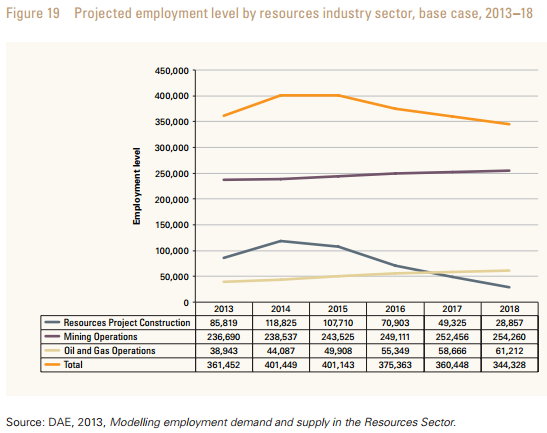

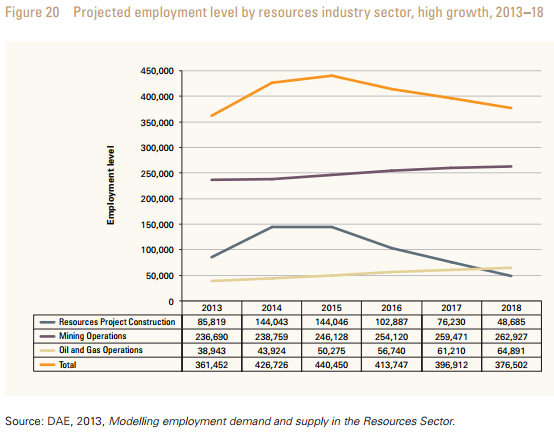

- Commodity prices will play an important role in shaping the demand for labour within Mining Operations. Under all three growth scenarios, Mining Operations employment is projected to increase every year from 2014 to 2018. Under the most likely base case scenario, employment is expected to increase from 236,690 workers in 2013 to 254,260 in 2018, which is a 7.4 per cent increase.

- All three growth scenarios anticipate significant annual employment growth of 9.4 per cent in the Oil and Gas Operations sector from 2014 to 2018. Employment under the most likely base case scenario is expected to experience robust growth from 38,943 workers in 2013 to 61,212 in 2018, which is a 57 per cent increase. This is due to many of the major liquefied natural gas projects currently under construction moving into their production phase.

Righto. So, we’re using BREE’s April forecasts which have already been cut moderately (although the modelling claims to adjust for that).

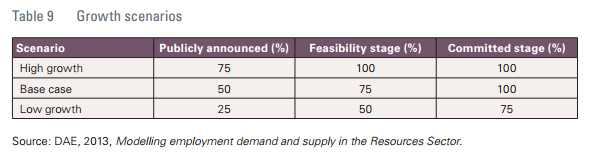

Here are the assumptions behind the three scenarios:

In BREE’s October update, 63 projects were at the committed stage so the low growth scenario of this study assumes a dozen more approvals in the years ahead. Not unreasonable though much depends upon whether we’re assuming LNG projects or salt mining down the beach.

Here is what each scenario does to employment. First the most likely “low growth” scenario:

The base case:

And high growth:

I agree that the low growth modelling is the one to watch. It indicates the peak in employment is passing as we speak and a big downdraft that rally gathers pace in 2015. Total mining losses are 55k jobs out to 2018.

That’s big but is manageable over the period. The issue is what kind of multiplier effect does it have? For instance, GLNG employs approximately 10k people directly but the project argues it supports wider employment for 45k people, most of which are outside of direct mining employment in the supply chains and support services.

It’s impossible to put a multiplier number on it, but it will be big.

Full report here.