Last week, Rumplestatkin posted an interesting article attempting to quantify the relationship between mortgage credit growth and house prices. The analysis drew on the credit aggregates data released monthly by the RBA and house price data from the ABS.

My gut feeling after reading the article was that it had probably focused on the wrong data input – namely mortgage credit data from the RBA – instead of using the value of housing finance approvals published by the ABS.

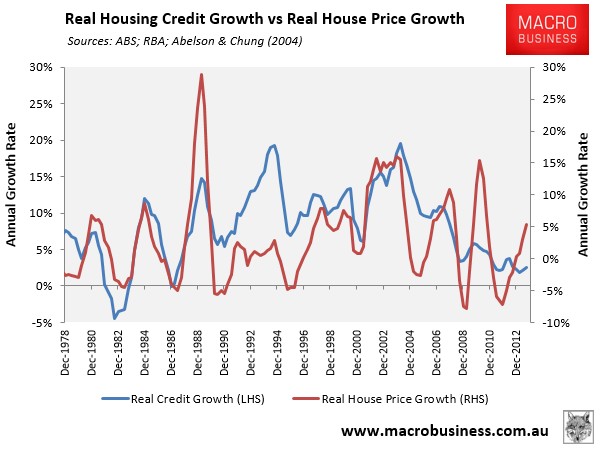

The reason for my skepticism in using the RBA’s mortgage data to predict house price growth is that it captures accelerated repayments from pre-existing mortgage holders, which does not actually affect housing demand but works to offset new mortgage creation. As such, the RBA mortgage data can give the false impression that mortgage demand is weak, when actually the demand from those whom impact price growth – i.e. newly created mortgages (excluding refinancings) – is running strong.

Indeed, as shown by the next chart, the relationship between the RBA’s mortgage credit growth and house prices has broken down over the past five years, presumably due to accelerated repayments from pre-existing mortgage holders offsetting new mortgage creation:

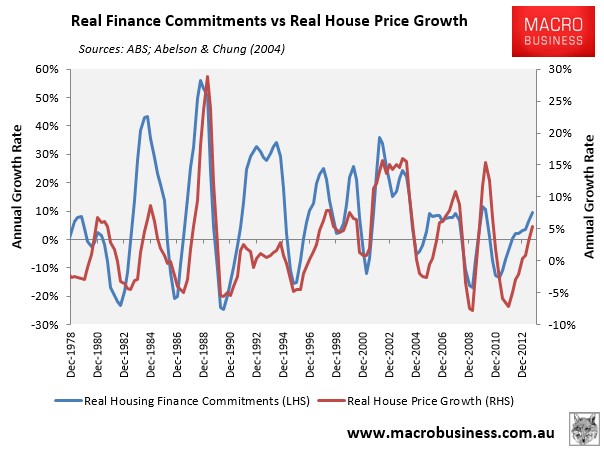

In my view, the ABS’ housing finance data (excluding refinancings) provides a much better predictor of house price growth, since it includes new mortgage creation only, and ignores noise associated with accelerated repayments.

As shown by the next chart, the correlation between the ABS’ housing finance growth and house prices is much stronger, and also tends to be a leading indicator for house prices:

unconventionaleconomist@hotmail.com