Steve Keen has been a rather lonely voice linking debt dynamics to asset prices, particularly home prices. While home values reflect the ‘fundamental’ value of homes in terms of capitalised rents, in addition they reflect a degree of debt-fuelled speculation. Thus, if one wants to generate a useful model for predicting house price movements it should include both the fundamental value benchmark of rents and interest rates and the dynamic speculative drivers of the rate of change and acceleration of mortgage debt.

A Twitter conversation between Noah Smith, Steve Keen, Unlearning Economics and myself on the relevance of debt dynamics in economic forecasting was the catalyst for this post.

Following this conversation Steve promised to post his data so we can all work from the same page and really see whether debt dynamics are useful forecasting inputs.

Steve is probably on to that as I type, but I can be impatient and need to work while I’m on my morning caffeine high. So I went ahead and payed with some numbers to see to what degree debt, the rate of change of debt, and the acceleration of debt explain home price movements.

For those of you familiar with Mathematica you can download my Notebook with all the code and calculations here (the file is called CreditAccelerator2.nb, and my apologies for no open source code).

The data I use comes straight from the RBA and ABS websites which my code will automatically download. For debt balance I use the sum of owner occupier and investor housing from the RBA Table D2, Credit Aggregates. Home price data is the ABS capital city measure. Rental price is the capital city rental price series from the CPI. Mortgage interest rate is from the RBA Table F5, Indicator Lending Rates. The data is quarterly from March 1990 to September 2013. Credit data, home prices and rents are in natural logs. All of this is linked in my code.

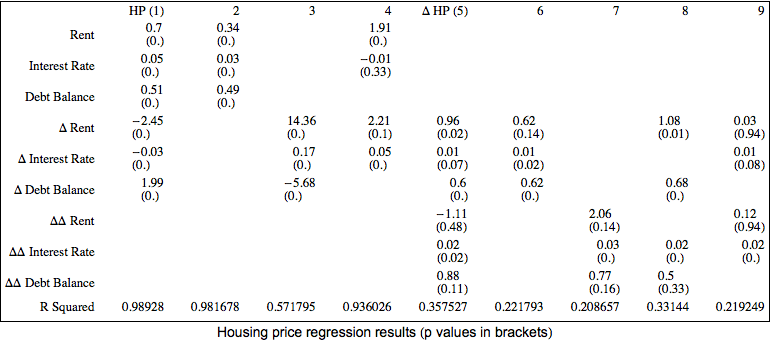

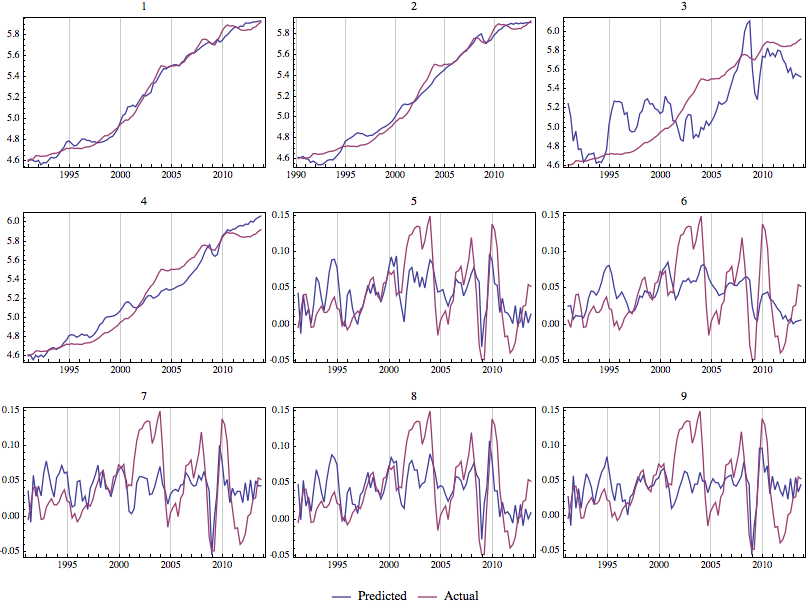

That’s it. Let’s mix it together and see what we get. I’ve posted the regression parameter results in the table below and graphs of each model’s predicted versus actual house price a little later in the post. The dependent variable for the first four models is house price, and for the next 5 is the change in house price.

Model 1 can be compared with model 4 where debt dynamics – the debt balance and change in debt – are removed. We do gain quite a degree of explanatory power by including debt. If you look at the graphs of predicted and actual house prices below you can see the tightness that including debt brings.

By the same token, for predicting the rate of change on home prices model 5 can be compared with model 9, where the change in home prices is estimate with and without debt dynamics (this time the change in debt and the acceleration of housing debt). In this case we get a much better fit of the data, and the graphs below confirm this visually. We also see that rent dynamics don’t have any explanatory power unless debt dynamics are controlled.

Browsing across the other models we see that all the variables are very important, with debt perhaps the least important, and the acceleration of debt seems to be a little chaotic to catch much.

One important consideration is the error in the quarterly measures. This means the second difference of the variables is especially volatile. From Keen’s earlier work it is pretty clear that in the US the lower volatility seems to lead to a greater importance on the acceleration of debt. Perhaps there is some smoothing that can be done here as well. We’ll have to wait and see the data Steve Keen posts.

An important caveat is that using national average measures won’t provide much actually investment guidance, since you can’t buy a national average home. At any point in time some homes will be under or over-performing the market. Moreover, the ongoing compositional change in the housing stock means that any individual home is likely to increase in value over the long run at a faster rate than this average measure.

What can we conclude from this preliminary analysis? For those who have studied the important role of debt in driving activity there will be no surprises. Debt is important, and if we don’t consider it when seeking to explain the changes in housing asset prices we will be missing a large part of the picture not capture by the rent and interest rate ‘fundamentals’.

When I get some time will follow up with some more analysis, including currency and terms-of-trade effects, which I expect to be crucial determinants of price changes in the Australian housing market. Some investigation of lags and other time series model processes will also be interesting, especially for predicting home price movements in advance.

Please share this article. Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin