Capt’ Glenn crashes dollar with MB agenda

What on earth are we going to write about now? RBA head Glenn Stevens has so comprehensively embraced the MB agenda that we’ve become mainstream!

In an interview with the AFR, which is clearly aimed at ramping up the RBA jawboning campaign, the Capt’ demanded a lower dollar, cautioned of the need for a real depreciation, declared macroprudential policy an option in current circumstances, warned Sydney property speculators to cool it and households to not increase their leverage, unfavourably discussed the settings for housing investment at the micro level, got behind a well-governed public infrastructure spend, prompted debate on Budget sustainability and suggested banks should pay for guarantees.

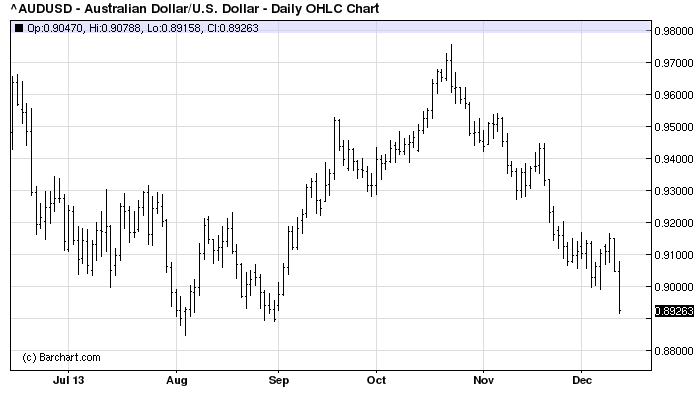

He’s cautious and frustratingly laconic but the messages are all there. As a result, the dollar crashed 1.5% to almost 89 cents:

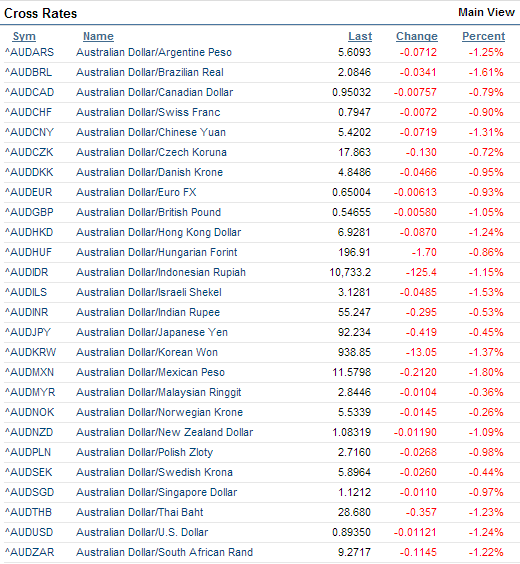

And was monstered on all of the crosses:

As forecast, we are going to see a downside test of this year’s lows, and break them in my view, certainly if Stevens keep saying this:

Mitchell: In the SMP I got the impression that you were looking for another depreciation on the order that we saw earlier in the year. On the exchange rate as it was at the time I inferred from that we were looking for an 80 cent dollar.

Stevens: I am not – you know, I’m not going to sit here and put numbers on these things. I don’t think the extent of our knowledge about what’s correct is that good, but I did think 95 was rather too high. I thought 85 would be closer to the mark than 95 at the time we started to make some comments some months ago, but, really, I don’t think we can be that precise. I just think that if things over the medium term evolve as we’re presently assuming – and I think it’s reasonable to make these assumptions – it’s going to be surprising if a nine at the front is the right number.

And he will. Don’t fight the Fed is the rubric of our age.

Running through things from the top, Stevens was pretty cold on more rate cuts:

Mitchell: Well, the market has increased its priced-in probability of a rate cut in February

Stevens: Well, only by a miniscule amount. You know, it’s about one chance in three or something.

Mitchell: Yes.

Stevens: So we’ll see when we get to February but, really, the curve doesn’t embody all that much more easing now. A partial chance of one.

And on macroprudential he was far more open than previously:

Stevens: Well, we’ve thought about these issues and we have had, as well, preliminary discussions at a working level with APRA and other agencies about if we needed to do something like that, what kind of things would they be, and I don’t – without wanting to go into the fine details of that, I think we’ve got a sense of the kind of things that might be effective if we need to do them. My general attitude to macroprudential tools is I think they’re potentially a useful adjunct to other policy tools that help you manage some of these tensions for a period of time. I think it would be a bit naïve and contrary to the lessons of history to expect that prolonged use of regulatory tools, and that’s what they are, they’re regulatory tools, and we know that regulatory tools over a prolonged period to try to make up for the fact that the price of credit is, in some sense, not in the right place.

We know that ultimately, that’s not very effective. We know that from our own country’s history. That was the history of the days prior to liberalisation where the price of money was too low and we tried all sorts of regulatory devices to stop the banks lending it and non-banks [inaudible] to lend it and so on. So we know that history, but that’s not to say that you can’t use them for shorter periods to kind of get you through a period where you’ve got some of these tensions. I think they’re probably useful in that setting, as long as we’re realistic about what we can expect.

Stutchbury: Should we expect that that will be on the agenda in 2014?

Stevens: I’m not sure. I wouldn’t necessarily want to go that far, but I regard the possibility of using such tools, if they would offer the hope of, you know, some useful outcomes, as on the table. I wouldn’t say that I’ve got an active plan to deploy them right now.

On housing more widely, his views have also shifted. Previously the RBA hasn’t embraced micro-economic explanations for house prices but now it has:

Stutchbury: So even if there isn’t a bubble, isn’t it increasing the risk in the system to have already house prices which haven’t gone through a genuine post-GFC correction to be rising again?

Stevens: Well, it’s a very big question. In some ways some people might answer the question, is it a bubble, by saying unfortunately, perhaps it’s not a bubble and unfortunately we may have done things as a society to make, in some fundamental sense, prices quite high. If that were true, you know, I have a certain sympathy with that. I think there’s a whole bunch of social and economic issues that go from there, which aren’t about really, the risk of a collapse, it’s about whether we have inadvertently given away a natural advantage that a country with this much land ought to have, that we ought to have cheap housing, not expensive and so on. And inter-generational issues about how our kids are ever going to afford to live in the same city as we do, so that’s a separate set of questions.

…Stutchbury: And you have alluded to the investor class in Sydney and it is interesting that a bigger than normal percentage of the construction approvals are coming in apartments, rather than houses. Do you see that as part of an investor class issue which might cause you concern? Is that a supply constraint which the Reserve Bank has talked about and you’ve alluded to again, or is that something to do with the changing nature of Australia’s biggest city?

Stevens: Well, I think it’s certainly to do with the way, as a community, we’ve decided to configure the marginal supply. I think, you know, we – my sense is we’ve taken decisions as a community to do more of that in high density. I think there are also preference changes with the younger generation today being more inclined to want to live quite close to where they work and enjoy the various aspects of inner city life in a way that perhaps my generation didn’t have such a strong preference for when it was the moment where we were starting in housing. I think both those things are probably true. Investors, there may be some dynamic in the prominence of investors as well and don’t forget, of course, it’s true that the investor approvals are rising quite quickly right now, and so are those for repeat buyers. The rest of us who are, you know, up sizing, down sizing or changing life, whatever we’re doing. It isn’t just the pure investors that are driving the trend.

I’ll simply note that all bubbles start with a kernel of truth. That does not mean they are not bubbles. On housing more widely Stevens was agnostic but clearly cautious on Sydney:

Mitchell: Now, just a quick return to the monetary policy issue, how big a constraint on you is the risk of overheating in the property market?

Stevens: I don’t – I haven’t felt particularly constrained thus far by what has been happening in housing…by and large, across the community, leverage – credit growth – has remained quite modest, in fact. The second caveat is, I think we will see a little bit of a pick up over the months ahead. In credit growth we’ve seen a 10 per cent rise over the last two months of data in the value of loan approvals, that’s a pretty healthy clip, and I think we will see some gradual pick up now in aggregate credit growth to households as a result of that. And that’s okay, but that is something that we will obviously be watching over the next six months or so. We – I think if we saw a return to the kind of double digit credit growth to households that we saw for so many years in the past, I would have to wonder whether that would be wise given the level of debt from where we start. That would be a different proposition to what we’ve seen lately so thus far, I think it’s okay but obviously, it’s a thing we have to watch.

Mitchell: So the interest rate that you have now is not different to what you would have if we didn’t have people worrying about bubbles in the

Stevens: I think – well, I would put this different way. I think what we’re seeing in the housing market and credit markets and the equity market, these are the sorts of things that low interest rates normally produce; it’s part of the way it works. If I didn’t see that, then I might have a different view about whether the rate setting we’ve got is the right one because you wouldn’t have this evidence that it’s working, but we do have this evidence, I think, and it’s accumulating as the months go by that the very low level of rates that we’ve reached is doing many of the things you would expect it to do. That’s a piece of evidence the policy is working. Whether it’s working by enough or not quite enough, of course, is always the judgment call but it’s certainly evidence that the transmission process is working in something like the normal way.

Stutchbury: A year ago in our talk you said that housing prices in Australia were high and you know, whatever correction there was has now been overtaken with price rises.

Stevens: That’s right.

To come to your point about risk, I think the key thing to keep your eye on is the leverage…We might see it yet and if we do, that will be something to be quite concerned about and, as I say, we need to think about the investor part in Sydney where there is a fair bit of borrowing starting to take place there now so care needs to be taken. But for the system as a whole, I don’t think, on what we’ve seen to date, that there has been a case for us to get on the soap box about leverage. It might come and that’s why we have to watch it, but thus far, that would be my view.

Stutchbury: But the household sector hasn’t really de-leveraged post-GFC

Stevens: Well, debt to income hasn’t fallen very much, that’s true. Then again, people have been servicing that debt quite comfortably, so it’s I suppose an open question whether there needed to be a large de-leveraging from where they were or whether the main thing is to avoid a big gearing up from here. Certainly, I think, we would be well advised to avoid that.

Here are the video highlights:

And the full transcript is here. Well worth reading the whole thing.