Following on from this morning’s post on how Wall St has re-inflated US housing, here is Westpac’s Elliot Clarke on the role of investors in US housing. I see two possible ways this can go. If Wall St is driving the rebound through rental securitisations then it could run despite rising interest rates because it’s a play on reaping the financial packaging fees. But the asset remains in the hands of the bank et al there has to be a high risk of run on the market when rates turn (or taper arrives). A tipping point scenario if I’ve ever seen one.

The US housing sector has been a key focal point in this recovery, not only due to the material price and activity declines that occurred following the GFC, but also because of the sector’s historical ability to have a positive, broad-based impact on activity – directly through new construction, and indirectly through confidence and consumption.

When considering the health of the housing market, house prices have been the financial market’s primary benchmark, the expectation being that as go prices, so goes activity. However, this has not proven to be entirely correct, with the contribution to growth of housing activity lacklustre relative to the scale of the prior decline and past cycles.

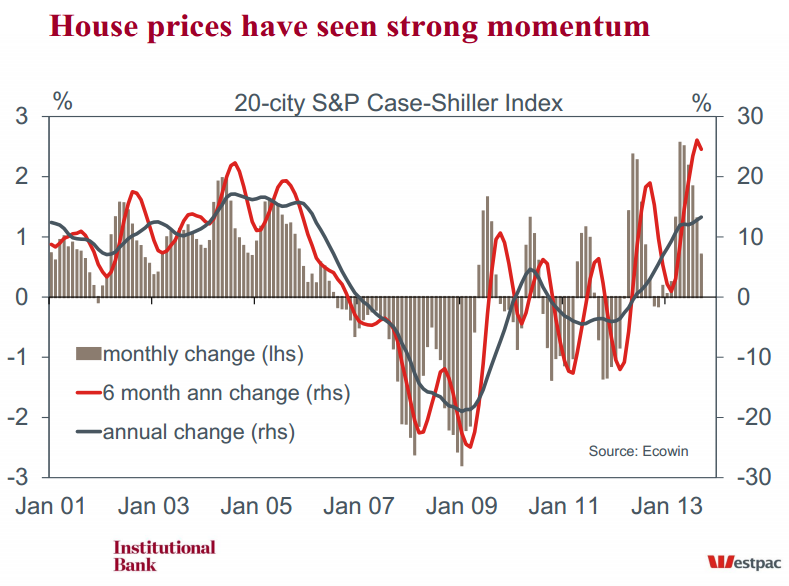

On house prices, the past two years have definitely given reason for optimism and confidence. According to the S&P/ Case-Shiller 20-city measure, house prices have risen by 18.5% between January 2012 and September 2013, with the bulk of those gains seen in the past year (13.3%yr).

While these gains are certainly significant, it is important to remember that, owing to the scale of the GFC price declines, national house prices are still down 21.5% from their April 2006 peak in nominal terms; and, given the PCE deflator has risen by almost 14% over that time, closer to a third in real terms. Arguably this is a key reason as to why the pass-through from price gains to confidence and consumption has been more modest than that seen in past cycles.

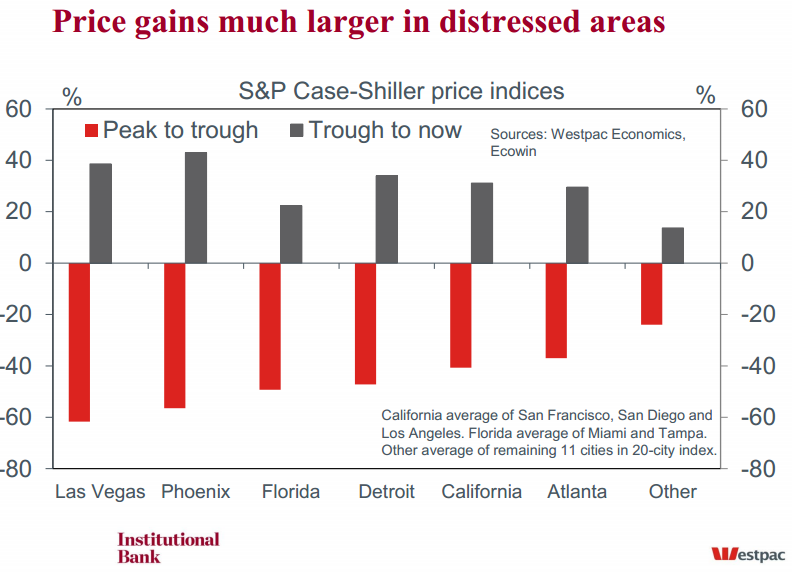

The other critical issue is that these price gains have not been equally shared across the country. One would typically expect those hardest hit to see a stronger recovery, but gains in the current episode seem excessive. From their respective late-2011/early-2012 low points, prices have risen by around: 40% in Las Vegas and Phoenix; 34% in Detroit; and 30% in California and Atlanta. Across the rest of the nation, the average gain has been around 14%.

The change in house prices in the cities named above are at odds with prevailing macroeconomic conditions. A classic example of this is Detroit. This is a city which has recently filed for bankruptcy (July 2013) and has one of the highest levels of unemployment in the country (9.5% in October, albeit down from 10.7% a year ago), yet house prices have risen by almost 12% in 2013 following a 15% gain in 2012. Similarly, Las Vegas has seen a 22% gain in 2013 following a 13% increase in 2012 despite Nevada’s unemployment rate remaining high at 9.3%, from 10.3% a year ago. Albeit to a lesser extent, the gains recorded in Phoenix also look to have followed this trend, with Arizona’s unemployment rate remaining stagnant around 8.2%.

The patterns above suggest investors (institutional and individual) have been the primary driving force behind the US housing market over the past two years, with large-scale investors playing a particularly prominent role in depressed areas. This corresponds with our observations on household income (discretionary income stagnant) and household credit (being driven by auto and student loans not mortgage credit) not to mention the dramatic deterioration in mortgage activity through 2013, primarily on the back of the taper-talk-induced rise in mortgage rates.

In and of itself, investor buying is not a bad thing. It provides a source of demand which helps markets to clear; and, in this instance, it is also helping to provide rental accommodation for households unable/ unwilling to purchase a home. However, where it does become an issue is when investor behaviour is short-term and speculative in nature. Available information is limited, but the pace of the gains and their geographical focus in hard-hit regions alludes to speculation, as do the many anecdotal reports of strong institutional investor interest.

RealtyTrac’s latest foreclosure report is also consistent with this thesis, with distressed and all-cash sales remaining key. Highlighting the risk of a potential abrupt reduction in investor demand, RealtyTrac reported that the share of total national sales to institutional investors fell from 12.1% in September to 6.8% in October; that compares to 9.7% a year ago. The proportion of institutional and all-cash sales are much larger in distressed regions. For example, institutional purchases in Memphis and Atlanta in October totalled 25% and 23% respectively. The proportion of all-cash sales also points to significant investor demand in other distressed areas, most notably Florida (66%), Nevada (55%) and Michegan (50%).

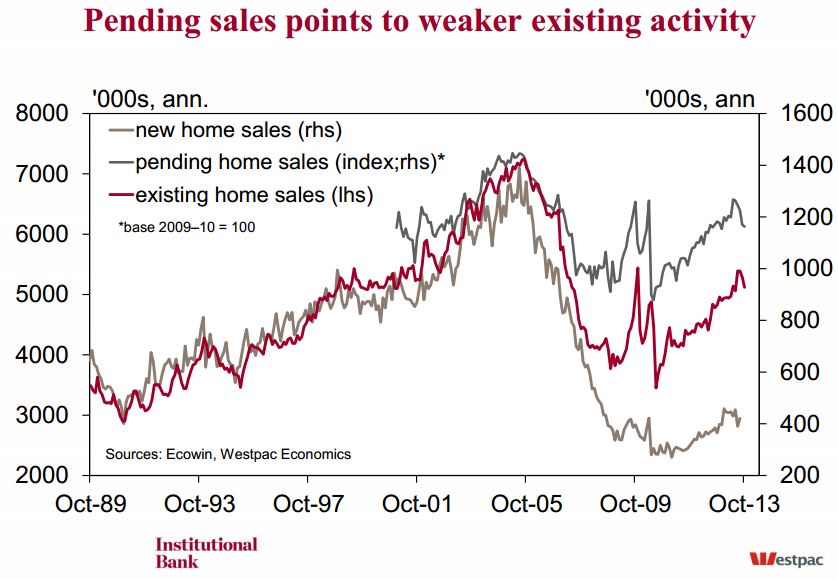

Amidst the activity data, a downtrend is clearly beginning to emerge. From their peak in January 2013, new home sales have fallen around 8% (to August). Existing homes sales held up through the first half of 2013, but higher rates and a potential softening in investor demand has since resulted in a 5% decline over September and October; pending homes sales’ 8% decline over the five months to October points to further weakness.

With mortgage rates remaining elevated and employment and income growth still subdued, the near-term fate of the US housing market looks set to remain heavily dependent on investor appetite. Best highlighted by the RealtyTrac report, there is a real risk that this marginal demand will abate, resulting in a deterioration in conditions and price growth. Already impacted by higher rates and October’s fiscal malaise, such a development would be unquestionably negative for consumer confidence and discretionary spending, both with respect to the housing market and general consumption.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.