Today’s hot equities topic is why is Fortecue trading at such a discount to its peers? Credit Suisse had the note that fired everyone up:

How does consensus arrive at an FMG target price of A$5.65, being a lowly FY14 P/E multiple of 5.6x? Our own target price of A$7.50 and DCF SOTP of A$9.40 are top of the market, despite our near-term iron ore prices being bottom of the market.

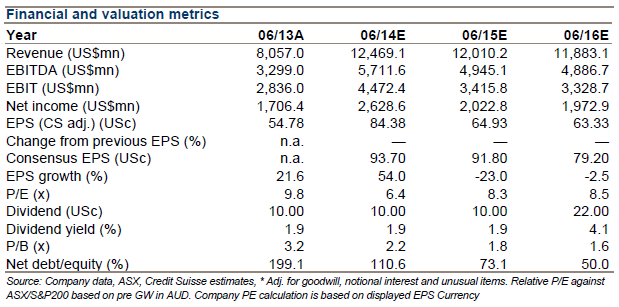

To investigate, we have used IBES consensus estimates to build a P&L and a simple DCF valuation that an investor can reproduce and verify. Using consensus estimates, we reach a DCF SOTP of A$8.30, not the street’s A$5.65. Likewise, a mid-cycle earnings valuation delivers A$8.10. Using a forward P/E at RIO’s 10.6x and adjusting for the difference in net debt implies a valuation of A$8.00/sh, and an EBITDA multiple implies A$10/sh.

The consensus target price can be derived by the DCF (but not other methods) by using a long-term iron ore price of $85/t CFR (real) rather than consensus’ $94/t, or by cutting the mine life to the 17 years of reserves while applying zero for additional resources and exploration potential.

The long-term iron ore price is the key sensitivity for the DCF. The incentive price for expansions delivering 15% IRR is US$100/t CFR (real), for a capital intensity of $150/t and C1 costs of $30/t. This suggests the longterm consensus price of $94/t is perhaps a little low, but not unreasonable.

Catalysts that may close FMG’s valuation gap with its peers are hard to define. Instead we expect a gradual re-rating as FMG’s shipments increase, and debt is reduced. Iron ore price is a key for sentiment.

Our DCF sum-of-the-parts valuation remains A$9.40/sh, and we retain our A$7.50 price target and OUTPERFORM rating.

I will add CS is bearish on iron ore.

I don’t think this is rocket surgery. FMG is being repriced as we speak but it should not trade on the same valuations as either RIO or BHP for one simple reason. Although it has managed to bring its costs of production down to around $80 or so, it remains the marginal high cost producer of volume in Australia by a considerable distance.

There are any number of risks that come with this territory, from an irrational and extended shakeout in more expensive Chinese iron production to local start ups like Gina Rinehart’s Roy Hill, which surely can’t have a higher break even than FMG and still get funding.

Advertisement

Thus it remains risky on two fronts. The debt remains very high and if the worst happens to the ore price, FMG will struggle to survive. But even if it does make it through it’s slimmer margins and greater concentration in one commodity is an earnings risk on competition.

How much it should be discounted is the only question.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.