Ok, so I’m going to roll over a little. The data flow in Australia is improving. It’s not red hot by any means but it’s well off the bottom and there are signals enough to suggest that the cyclical acceleration is gaining momentum over the structural headwinds, for now.

Let look at the rundown. First, iron ore prices are as strong as an oxe. We have managed to jump right over the seasonal price weakness and into the end of year restock without skipping a beat. Much of the supply deluge is ahead of us but some is behind yet prices have traded very atypically in a reliable band around $130 for six months.

Chinese steel production has been strong throughout this period, much higher than anticipated, but I’m also of the view that we are seeing the benefits of industry concentration in the price. The Pilbara iron ore cartel is adept at massaging prices and are doing a damn good job of it. I suspect the great Chinese destock of 2012, which washed out much of its hoarded product, has handed pricing power back to the miners as the Chinese supply cushion is gone.

In addition, the shape of Chinese reform proposals for real estate is appearing reasonably benign. China still plans to rationalise its steel production as a part of its plans to rebalance away from investment but it looks like glacial not radical change is in the offing.

It is also becoming clear that the only imminent threat to Australian iron ore – a resumption of Indian trade – is not going to materialise in volume any time soon.

I still expect a declining iron ore price next year but all things being equal that bottom may be closer to $100 not the $60-80 downside spikes I’ve been envisioning for some time (though further out we may see such).

That means Australia’s terms of trade stay higher for longer. Much of the deflation in coking coal price has transpired. I expect more weakness for thermal coal but it too has deflated a lot. Gold is well off its highs. If iron ore isn’t going to tumble neither is the ToT.

That means Australian income growth next year will be better next than I feared it would be. It also means fiscal instability will be lower.

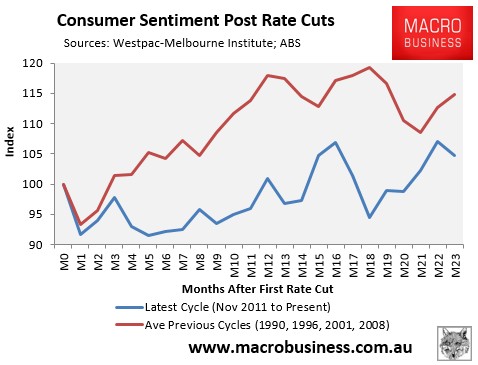

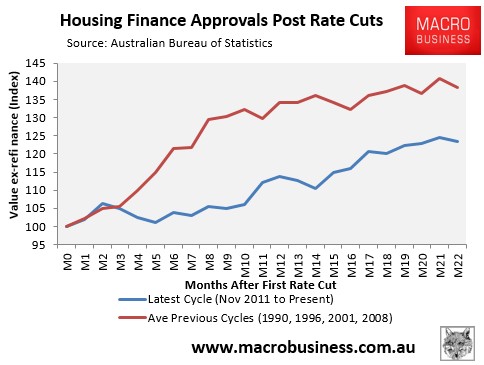

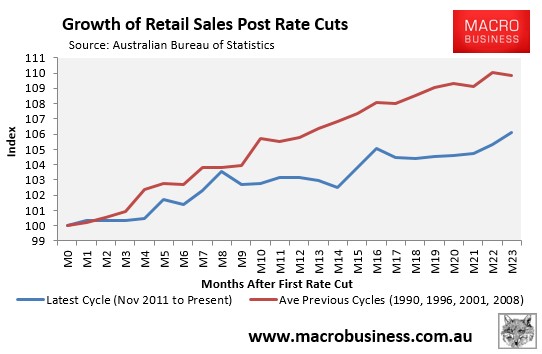

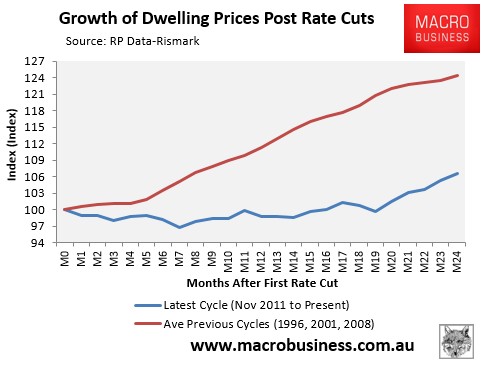

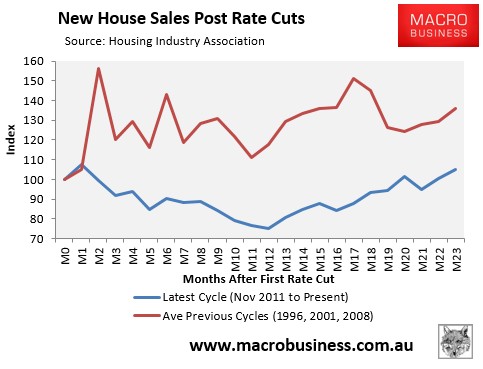

Which brings us to the local cycle. The monetary stimulus we’ve seen so far has been as extreme as the response to it has been lousy. Check out the following charts which show you why I’ve been bearish for two years:

This has been a very weak cycle even accounting for the recent acceleration in activity. A range of indicators are also now signalling that the labour market is at the bottom. Although I don’t expect any sharp turnaround, stability will itself encourage the recent turn in confidence trends for the better.

The cyclical upswing driven by house price rises is slowly spreading. It’s too early to call September’s rebound in retail sales a new trend but mortgage market activity is widening beyond Sydney. Both the leading indexes of AFG and RP Data suggest Melbourne is starting to bubble. I expect massive oversupply to hold prices in check in the second city – versus Sydney at least – but growing at almost 10% per annum is hardly slouch material, even if that would only get Melbourne back to its previous highs. In due course the exuberance may spread to Brisbane.

Don’t get me wrong, absolutely nothing in my structural view has changed. If anything it’s getting worse. The world is still a huge mess. China must rebalance. Europe is paralysed. The US must face its budget issues. I still expect supply to overwhelm commodities prices, Australia to confront a credit cap before long, the capex cliff to be worse than officials think as well as to undermine any genuine economic revival, and for households to keep saving. As we get deeper into next year and the capex cliff falls away, the substance beneath this bubble episode will get more and more thin. Each rise in house prices only drains further the competitiveness of our rentier economy and we remain at a higher risk of recession in the next three years than any time I can remember.

But timing is everything and when animal spirits attack you’d best join the herd lest you’re run down. The trick is seeing the approaching cliff before the herd tosses you off it.

In terms of my three scenarios for the end of the asset cycle – when the RBA is forced to introduce macroprudential tools to bring down the dollar, or when the RBA is forced to jack rates to control house prices, or when a full growth response raises rates – I am now evenly divided between one and two with three still trailing by a very long length.