My base case for a Fed taper is mid next year. But Friday’s US data continued a good run of upside beats and, given the taper is the only game in town for asset prices, we should remain vigilant.

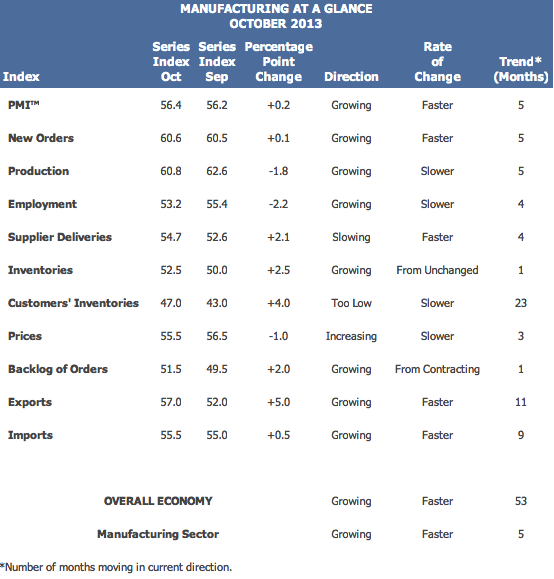

The very important ISM (essentially the US PMI) was again strong:

There is no weakness at all in there and no sign of the shutdown. Just to confuse things, these days there is also a generic Markit PMI which was less favourable, showing a sharp drop in production on the shutdown, but it’s the ISM that matters.

As a consequence, long bonds sold off sharply with yields up 2%:

Stocks rallied too, half a percent, on the hope that the ISM is wrong. So, where is this data going and is it enough to revive an imminent taper? Calculated Risk offers the following guidelines:

1) The unemployment rate probably increased sharply in October (due to the shutdown), but the impact of the shutdown will be reversed in the November report that will be released on Friday December 6th. If the unemployment rate declines back to 7.2% or so in November (the September rate), then the FOMC might taper.

2) As Merrill’s Hanson noted, the FOMC would probably also be looking to see employment growth close to 200,000 in the November report. If the year-over-year change in employment is still around 2.2 million for November, the FOMC might taper.

3) The FOMC is also concerned that inflation is too low. From the October FOMC statement:

The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, but it anticipates that inflation will move back toward its objective over the medium term.

The PCE price index for October will be released on December 5th (the September PCE index will be released this week). If PCE prices are moving back towards 2%, the FOMC might taper. Note: CPI for November will be released on December 17th and might influence the decision.

4) On fiscal policy, the budget conference committee is scheduled to present an agreement on December 13th (just before the FOMC meeting). The committee is expected to play “small ball”, so it is possible an agreement will be reached. If a reasonable agreement is reached (hopefully reduce the impact of the sequester in 2014), then the FOMC might be more inclined to taper. If it appears that the House might shutdown the government again, the FOMC will be inclined to wait.

If the Fed was nervous enough to wait in September then any circumstance without a fiscal resolution is a no-brainer hold. As well, data is beginning to flow through now showing the impact on home construction of the past few months of headwinds and it’s looking like a pretty sharp fall, adding to recent weakness in pending home sales. Also from Calculated Risk:

Builder results so far strongly indicate that the combination of higher mortgage rates and aggressive home price increases resulted in a significant slowdown in new home sales last quarter. While the relationship between large builder results and Census estimates for new home sales is far from perfect (partly reflecting market-share changes but also reflecting methodological and timing differences), these builder results suggest that Census estimates for new SF home sales for September (re-scheduled for release, along with estimates for October, on December 4th), could be down sharply from August.

This data is the equivalent of the HIA in Australia and is reliable enough.

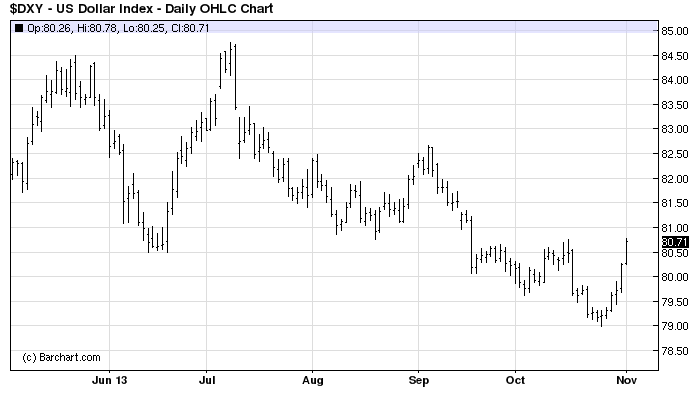

Before we get too complacent going even longer equities, currency markets also reacted to the Friday data flow by aggressively bidding up the US dollar more than half a percent and it is threatening to break out on the chart:

Everything undollar was hit with the Aussie and gold down half a percent and oil down almost 2%. Some of this heat is also coming from a growing expectation that the ECB will cut rates this week.

At this point, then, my view is unchanged that taper is March at the earliest. These shutdown events have a strange impact on the economy. Demand hiccups briefly which sends a little shock through the supply chain, which pauses, then the cash starts to flow again and there’s a little hill of pent up demand to service just as inventories flatline. Production then has to catch for a quarter or two.

In short the data should be decent running into Christmas but underneath that I still US housing slowing too fast for the Fed’s comfort. Unless there’s a fiscal settlement that removes fiscal drag in 2014, which seems very unlikely at this point, equities can still rely on the Fed put, though as the data flows you’d expect some nerves.