Residex has released its house and unit price results for the month of September, which revealed flat growth in national house values over the month, but significant divergence across the various markets (see below table).

Residex’s price results obviously contradict RP Data’s, which recorded 1.6% growth in dwelling values nationally in September. Residex’s quarterly growth rate of 0.48% is also well below the other major data providers – the ABS (+1.9%), APM (+2.2%) and RP Data (+3.8%) – which all recorded much stronger growth over the quarter, albeit at the national capital city level.

Advertisement

Nevertheless, in this month’s commentary, Residex founder, John Edwards, plays down talk of an Australian housing bubble, instead arguing that the recovery is patchy:

Improved consumer confidence and lower interest rates have been good news for Australian housing markets. I find it hard to support the bullish press about a potential housing bubble developing and the market powering ahead. While markets are improving and “red ink” is nowhere near as prevalent as it was this time last year, growth is patchy and there are still markets that have not recovered from the adjustments that occurred over the last three or so years.

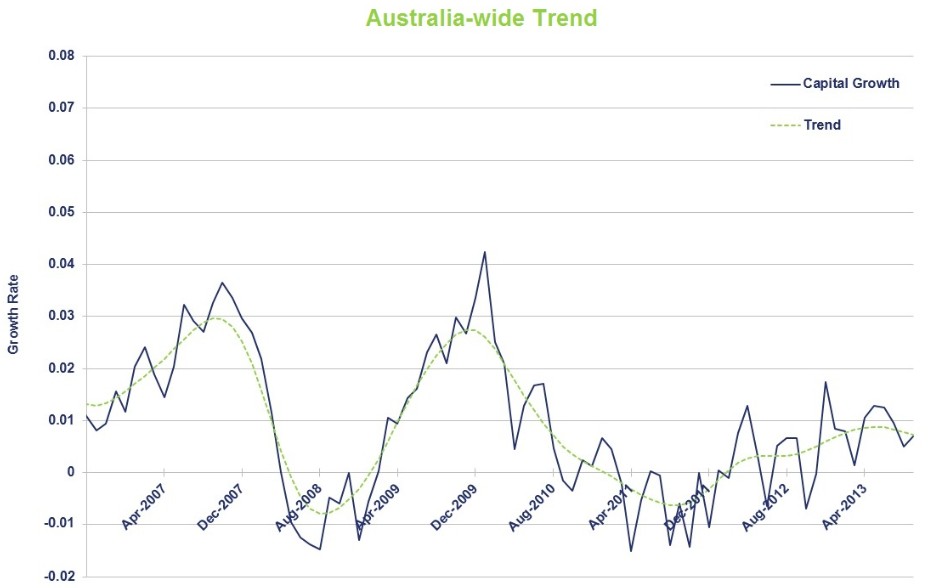

Graph 2 displays the combined house and unit trend for Australia wide. While the trend is encouraging, it does not point to anything other than a market presenting modest recovery.

Sydney is the standout performer with its house and land market performing strongly. On the other hand, Sydney’s unit market is only performing slightly above inflation (1%). The reason for this is a surplus supply of unit stock. The majority of new stock in Sydney can be found in the unit market, while the house and land market cannot keep up with demand.

The position across Australia is similar. Unit developments are the preferred option for developers and as a consequence, supply is sufficient to ensure growth in the unit market is kept to a relatively low level compared to the house and land market.

Sales activity also confirms that the market is not overheating and we are not entering boom times. Graph 3 presents the total sales activity for dwellings across Australia. The data indicates that while things are improving, there is some way to go before we reach a historically ‘normal’ market. Total sales activity is still lower than it was in 1999.

Growth in the markets has basically been driven by a shortage of stock for sale, particularly in Sydney. However, as the “Spring Selling Season” gets underway, there has been a significant increase in property listings which is helping growth rates to moderate. The slight downturn in the market’s growth is evident in Graph 2.

The predicted forecast average capital growth outcomes over the next five years have been provided in Table 1. You will notice that the predictions are modest average growth rates. Residex models are suggesting that growth in 2014 will be similar to what has been seen this year and that growth will moderate once interest rates start to move up to more normal levels.

I believe that while the economy is doing relatively well and sentiment is improving, it still needs a further boost as interest rate reductions have not stimulated business activity sufficiently. I think there will be a further interest rate reduction, which will probably be the last in the cycle, in the order of 0.25%. It is unlikely that the RBA will move on the rate position until February as it will want to assess the impact of the new government, see what flows from the Christmas trading period and if the improved sentiment in the business sector flows into improved investment activity and employment. Inflation does not look as if it is an issue for the RBA as a wage blow-out is unlikely given the potential for a deteriorating employment situation.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.